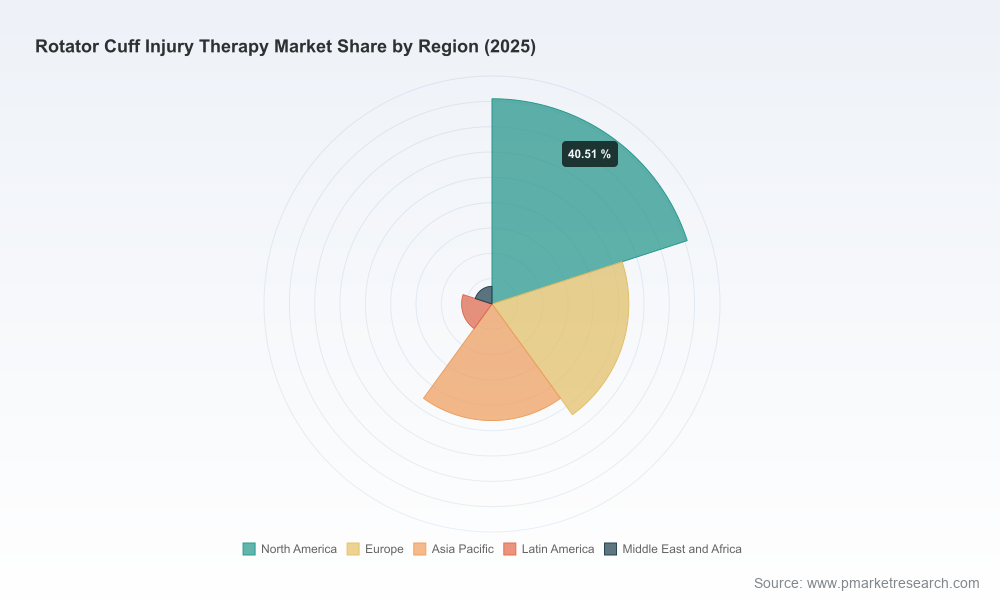

Rotator Cuff Injury Therapy Market: Strategic Imperatives for 2026 — PW Consulting Market Report

PW Consulting today releases its authoritative market study on the Rotator Cuff Injury Therapy market — a tactical intelligence product designed to inform executive decisions across medtech, orthopedics, private equity and health system strategy teams as they plan for 2026 and beyond. Built on a 2025 base year and combining quantitative market modeling (historical 2020–2025) with forward-looking scenario analysis (2026–2032), the report delivers the market context and directional forecasts that senior leaders need to prioritize investment, R&D and commercial initiatives.

Rotator Cuff Injury Therapy Market

Market trajectory: a clear, investable growth story

Our bottom-up model shows a resilient, mid-single-digit expansion through the coming decade. With the market valued in the 2025 base year and a compound annual growth rate of 6.1% across the 2026–2032 forecast window, PW Consulting projects consistent upside driven by aging demographics, expanding indications for biologic augmentation, and steady adoption of minimally invasive surgical technologies. By 2032 the market is projected to be materially larger than the 2025 base, reflecting both procedure growth and higher-mix, higher-value interventions in key treatment pathways.

Rotator Cuff Injury Therapy Market

Importantly for corporate planners, the historical period (2020–2025) demonstrates the market’s ability to absorb macro shocks while continuing structural adoption of implants, augmentation matrices and next-generation anchors. That stability makes the rotator cuff therapy space an attractive arena for targeted innovation and supply-chain optimization in 2026.

Rotator Cuff Injury Therapy Market

Why this report matters for 2026 decision cycles

- Portfolio prioritization: The analysis identifies which therapy modalities and device classes show disproportionate upside under alternative reimbursement and clinical-guideline scenarios — enabling R&D and product managers to reallocate resources away from commodity anchors into differentiated biologics and augmentation solutions.

- Go-to-market timing: Our scenario work maps product launch windows against guideline updates and expected reimbursement shifts so commercial leaders can time clinical trials, surgeon education and contracting efforts to maximize early uptake.

- M&A and partnership screening: The report’s deal-readiness matrix and commercial fit assessment accelerate target screening for acquirers and licensors seeking bolt-on assets with rapid integration potential.

- Reimbursement & policy playbook: Given evolving CPT coding behavior and the documented variable success of complexity modifiers, the study provides operational tactics that compliance, physician liaison and value teams can deploy to secure higher reimbursement capture.

- Clinical evidence ROI: We quantify how incremental reductions in re-tear rates and improvements in function translate into payer value and lifetime societal savings — a critical lever for evidence generation investments in 2026.

Report contents — practical, execution-ready intelligence

- Executive summary with investor-ready talking points and prioritized strategic options for different enterprise archetypes (large OEMs, fast-follower medtechs, biologics startups, PE investors).

- Detailed market-sizing and growth modeling (2020–2032) with sensitivity analyses across adoption, pricing elasticity and policy scenarios.

- Clinical and technology landscape: assessment of key therapy classes (suture anchors, bioinductive implants, augmentation matrices, balloon spacers, arthroscopic systems), clinical evidence heatmaps, and surgeon-adoption curves.

- Regulatory & reimbursement mapping: timeline of recent device clearances, guideline shifts, and practical coding/reimbursement playbooks that affect margin realization.

- Competitive landscaping: vendor scorecards, capability mapping and strategic risk analysis for incumbent and emerging players.

- Commercial playbooks: go-to-market segmentation, KOL engagement frameworks, pricing strategy templates and hospital/ASC contracting approaches.

- M&A and partnership blueprint: valuation drivers, integration checklists and prioritized targets by capability gaps.

- Supply chain and manufacturing assessment: component concentration risks, quality/regulatory bottlenecks and sourcing mitigations for 2026.

- Appendices with primary research summaries, interview extracts from surgeons and procurement leaders, and methodological notes supporting reproducibility of our model.

Competitive landscape: concentrated yet open to disruption

The competitive structure reflects moderate concentration: the top three firms account for a meaningful share of activity while a broader cohort of specialist players captures the balance. This mix creates both stability and room for innovation — incumbents retain distribution and OR relationships, while specialized firms and biologics innovators can carve high-value niches through clinical differentiation and targeted reimbursement strategies.

Key companies profiled in the report include:

- Arthrex, Inc. (Naples, Florida, USA) — renowned for comprehensive knotless and knotted repair systems and augmentation portfolios; their integrated approach to surgeon training and product ecosystems continues to set a high commercial bar.

- Smith & Nephew plc (London, UK; US ops in Fort Worth, TX) — with a growing bioinductive implant presence and newer tendon repair systems, they are leveraging biologics to address re-tear reduction imperatives endorsed by recent clinical guidelines.

- Stryker Corporation (Kalamazoo, Michigan, USA) — offers anchor platforms and adjunct devices like balloon spacer implants which target massive irreparable tears; their strength lies in cross-sell through established shoulder reconstruction franchises.

- Zimmer Biomet (Warsaw, Indiana, USA) — focused on instrumentation, anchors and biologic adjuncts; their channel reach and OR footprint support high-velocity adoption for compatible innovations.

- Johnson & Johnson (DePuy Synthes) (New Brunswick, New Jersey, USA) — brings scale and broad implant portfolios; strategic moves will likely target higher-margin augmentation technologies to offset pricing pressure on commodity anchors.

- CONMED Corporation (Utica, New York, USA) — positioned on augmentation implants and soft-tissue reinforcement; recent regulatory wins increase their commercial optionality.

- Atreon Orthopedics (Dublin, Ohio, USA) — a specialist player focused on bioresorbable wicks and autobiologic matrices; product-clearing events and launches make them a watchlist candidate for partnerships or licensing.

- Integra LifeSciences (Princeton, New Jersey, USA) — supplying soft-tissue repair and augmentation solutions with clinical and distribution synergies that complement adjacencies in reconstructive surgery.

The report’s vendor scorecards evaluate each company across clinical differentiation, go-to-market execution, regulatory positioning, and balance-sheet capacity — enabling buyers and partners to quickly identify strategic fits and potential competitive responses.

Recent developments shaping the 2026 playbook

- AAOS 2025 Clinical Practice Guideline updates strongly favor bioinductive implants in select rotator cuff repairs to reduce retear rates — a guideline shift that materially changes evidence thresholds and commercialization roadmaps.

- Several augmentation devices obtained regulatory clearances in the 2024–2025 window, expanding clinicians’ toolkit for tendon-bone reinforcement and increasing the need for head-to-head evidence to justify premium pricing.

- Notable firm-level events — including new product showcases and cleared biologic matrices — are accelerating competitive activity and creating time-sensitive windows for strategic responses in 2026.

- Operationally, reimbursement dynamics remain a gating factor: complexity modifiers for arthroscopic rotator cuff repair succeed in a minority of claims, underscoring the need for robust documentation and payer engagement to capture full case value.

Actionable recommendations for 2026

- Allocate evidence-investment to payer-relevant endpoints: Prioritize studies that demonstrate re-tear reduction and functional gains that map to lifetime societal savings; these outcomes materially strengthen contracting leverage.

- Design product launches around guideline milestones: Synchronize KOL engagement, post-market registries and payer dossiers to coincide with professional-society updates for faster uptake.

- Prepare modular commercial offers for ASCs and hospitals: Differentiate pricing and service bundles to reflect procedural complexity, OR time savings, and implant mix.

- Scan the M&A landscape with a capability-first lens: Seek targets that fill biologic augmentation or evidence-generation gaps rather than doubling down on commodity anchors.

- Harden reimbursement operations: Invest in coding education, case documentation templates and payer-negotiation playbooks to improve modifier success rates in 2026.

Where to find the full intelligence

This press release highlights the strategic thrusts and executive-grade recommendations contained in PW Consulting’s Rotator Cuff Injury Therapy Market report. The full report contains proprietary segmentation, regional and end-user breakdowns, and granular scenario outputs that are intentionally withheld here to preserve actionability for report subscribers. For access to the comprehensive model, vendor scorecards, and the downloadable executive slide pack designed for board-level discussion, please visit the PW Consulting report page.

PW Consulting’s Rotator Cuff Injury Therapy Market report arms decision-makers with the data, context and prioritization frameworks needed to convert market growth into durable competitive advantage in 2026 — whether that means accelerating a device launch, structuring a partnership, or mounting a targeted acquisition. In a market defined by clinical nuance and reimbursement complexity, timing and evidence strategy will determine winners.

For detailed analysis of this topic, please visit the official page:Rotator Cuff Injury Therapy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com