Где можно купить колесные диски

Other |

2026-06-19 17:51:30

As EW, medical device, materials, and food-processing firms plan their 2026 investment cycles, a nuanced understanding of the Electron Beam (E Beam) Accelerators market has moved from "nice-to-have" to mission-critical. PW Consulting’s latest market research—anchored to a 2025 base year and a detailed historical review spanning 2020–2025—presents a forward-looking assessment across the 2026–2032 forecast horizon. Our analysis shows the market expanding at a compound annual growth rate (CAGR) of 4.15%, with market revenues progressing steadily from the early-2020 baseline through a projected 2032 value that signals persistent, structural demand for electron-beam enabled processing and irradiation solutions.

E Beam Accelerators Market

Transition from Proof-of-Concept to Scale: Between 2020 and 2025, we observed technology maturation and increased industrial adoption. 2026 is the first year in our forecast where purchasers face decisive scaling choices—invest in modular low-voltage installations for distributed processing, or commit to high-throughput, capital-intensive platforms that consolidate volumes into centralized irradiation centers.

E Beam Accelerators Market

Regulatory and Contract Momentum: Recent contracts and regulatory approvals have accelerated procurement timelines. These developments are creating short windows for purchasing and partnership negotiation that can materially affect 3–5 year supply chain dynamics.

E Beam Accelerators Market

Service & Outcome-Based Models: Suppliers are shifting from equipment-only sales toward integrated service contracts (performance guarantees, monitoring, and managed irradiation services). Companies that miss this pivot risk locking into higher lifecycle costs and inferior uptime performance.

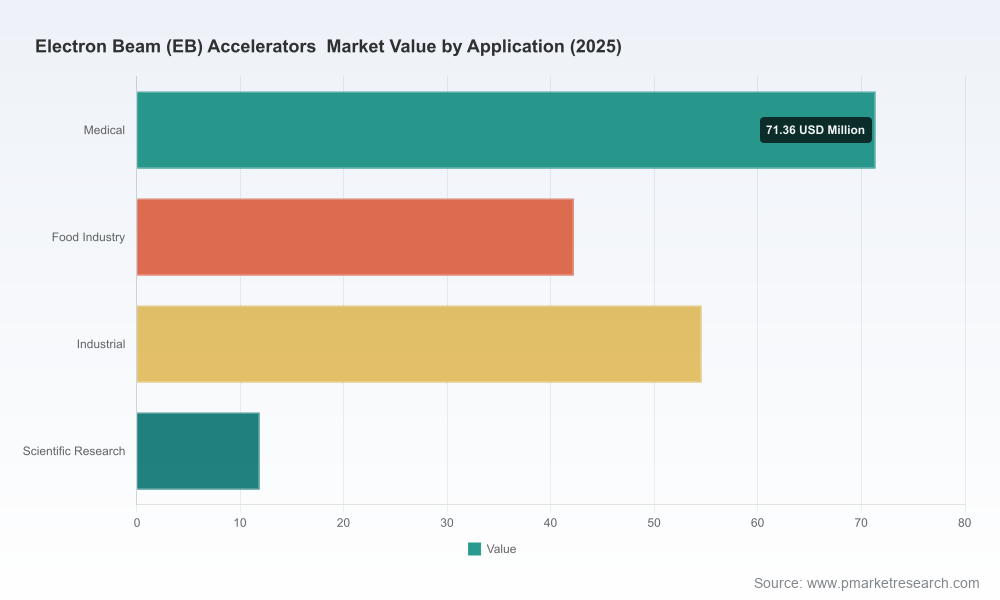

Our market sizing synthesizes primary interviews, equipment shipment data, and end-market consumption patterns. Total market revenues increased consistently through the historical period and continue to grow in our baseline forecast: the market expands from the 2025 base year to a materially higher level by 2032 at the modeled 4.15% CAGR. This trajectory reflects multiple, overlapping demand drivers—medical sterilization renewals, material-property enhancement for polymers and wires, food irradiation scale-ups, and research-sector investments in irradiation and non-destructive testing. For buyers and investors, the headline implication is clear: this is a growth market, but one characterized by varying return profiles across system types and applications.

Actionable Market Sizing & Scenarios — Bottom-line revenue forecasts, upside/downside scenarios, and sensitivity analyses tied to capex cycles, regulatory shifts, and adoption curves for low-, mid-, and high-energy accelerators.

Decision-Ready Use Cases — Three industry playbooks (medical sterilization, polymer cross-linking for wires/cables, and food irradiation) that map investment size to expected throughput, payback windows, and lifecycle OPEX considerations.

Technology & Product Roadmaps — Comparative assessment of low-voltage vs. high-energy systems, including typical integration footprints, maintenance intensity, and uptime risk drivers. We examine trade-offs between distributed low-voltage deployments and centralized high-energy facilities.

Regulatory Impact Matrix — Country- and region-agnostic scenarios that outline licensing timelines, typical compliance bottlenecks, and mitigation steps to keep deployment timelines on schedule.

Supply Chain & Service Archetypes — Supplier capability maps, typical lead-times, after-sales service models, and third-party irradiation center economics to inform make vs. buy and partnership strategies.

Commercial & M&A Playbook — Target screening criteria, valuation bench-marks for strategic acquisitions, and integration checklists for buyers seeking to secure capacity or IP in the electron-beam ecosystem.

The market sits at a moderate concentration level: our analysis of supplier shares indicates a clear leader group followed by a competitive mid-field. This structure has tangible consequences for pricing, service availability, and innovation velocity. Key players included in our competitive deep-dive are industry stalwarts and regionally dominant OEMs, each bringing distinct strengths:

NHV Corporation (Japan): A vertically integrated manufacturer of Electron Beam Processing Systems (EPS) with offerings spanning low to high energy zones. Recent activity includes commercializing an EPS monitoring system and signing a first-use contract with a tire manufacturer—an early example of product-plus-service monetization that shortens customer time-to-value and improves production stability.

CGN Dasheng (China): A full-scope designer and installer notable for deployments in tyre curing and polymer cross-linking. Its delivery of an accelerator into the EU signals both export capability and the increasing internationalization of non-Western suppliers.

Vivarad (France): Known for a wide energy range of systems and a large install base worldwide. Their track record provides a reference point for reliability and field-service expectations.

Wasik Associates (US) and Mevex (Canada): Specialists in custom, turn-key systems that cater to film/foam/wire manufacturers and high-power applications, respectively. Their engineering-heavy approach is an enabler for bespoke process integrations.

IBA Industrial (Belgium): A supplier of high-power Rhodotron® accelerators, with recent contracts highlighting demand for centralized, large-capacity sterilization and irradiation solutions.

Energy Sciences Inc. (US): A leader in low-voltage EB systems focused on packaging, coatings, and cross-linking applications—illustrative of the market’s split between low-voltage distributed units and high-energy centralized platforms.

Strategic Contracts and Installations: High-profile contracts—such as a multi-accelerator installation in Europe and early-use monitoring system agreements—are compressing supplier lead times and reshaping procurement calendars.

Trade Shows & Technology Transfer: Continued presence of OEMs at major industry exhibitions is accelerating cross-border technology adoption and partnership formation. These forums are also acting as deal accelerators for OEMs offering integrated service models.

Regulatory Alignment: Select installations have set precedents for sign-off pathways in major markets, reducing execution risk for buyers who align early with recognized suppliers and certified integrators.

Service Differentiation: Vendors bundling monitoring, predictive maintenance, and managed irradiation services are capturing larger lifetime values, influencing procurement committees to favor total-cost-of-ownership over headline price.

Frame Decisions Around Throughput and Flexibility, Not Unit Price — Map expected volumes across 3–5 year horizons and stress-test options for both distributed and centralized processing. The wrong architectural choice can double lifecycle costs or shorten asset lifespan.

Prioritize Supplier Service Ecosystems — In a market where uptime and regulatory compliance are critical, the quality of after-sales service and monitoring can outweigh a marginal equipment cost advantage.

Consider Partnership Models to De-Risk Capital Intensity — For companies unclear on long-term volumes, managed service agreements or capacity-sharing at third-party irradiation centers reduce entry risk while preserving optionality.

Use M&A and Minority Investments to Secure Capacity — Buyers seeking quick expansion or vertical control should prioritize targets that add either unique process IP or guaranteed throughput in high-demand geographies.

Build a Regulatory & Operational Playbook Early — Anticipate licensing timelines, align with suppliers that have proven approvals, and secure technical consultancy during procurement to avoid execution delays.

Our full E Beam Accelerators Market report is designed as a working tool for procurement teams, CTOs, strategic development leads, and private equity sponsors. It includes downloadable models, supplier scorecards, and a playbook for structuring commercial agreements that capture the value drivers summarized above. For teams preparing 2026 budgets and capital allocations, the report’s scenario analyses and ROI matrices provide the granular inputs necessary to validate investment cases.

To unlock the complete dataset, segmentation breakdowns by region, energy type, and application, and PW Consulting’s proprietary supplier benchmarking, please access the full report and interactive dashboards on our website. The "trailer" you’ve read here is intended to surface strategic opportunity and risk; the full publication contains the decision-ready detail that procurement, operations, and corporate development teams will need to act with confidence in 2026.

For detailed analysis of this topic, please visit the official page:E Beam Accelerators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com