EEG Devices Market Outlook 2031: Technological Advancements & Industry Growth

Health |

2026-05-06 18:31:22

PW Consulting today publishes an executive preview of our forthcoming deep-dive market study, "Cellular Base Station Antenna for Telecommunications Industry Market" (base year 2025). This briefing is crafted to help C-suite and investment teams build 2026 strategies that balance rapid 5G densification with pragmatic capital allocation. Our analysis synthesizes historical performance (2020–2025), a forward-looking forecast to 2032, vendor-level competitive dynamics and regulatory scenario modeling to support high-consequence decisions in the year ahead.

Cellular Base Station Antenna For Telecommunications Industry Market

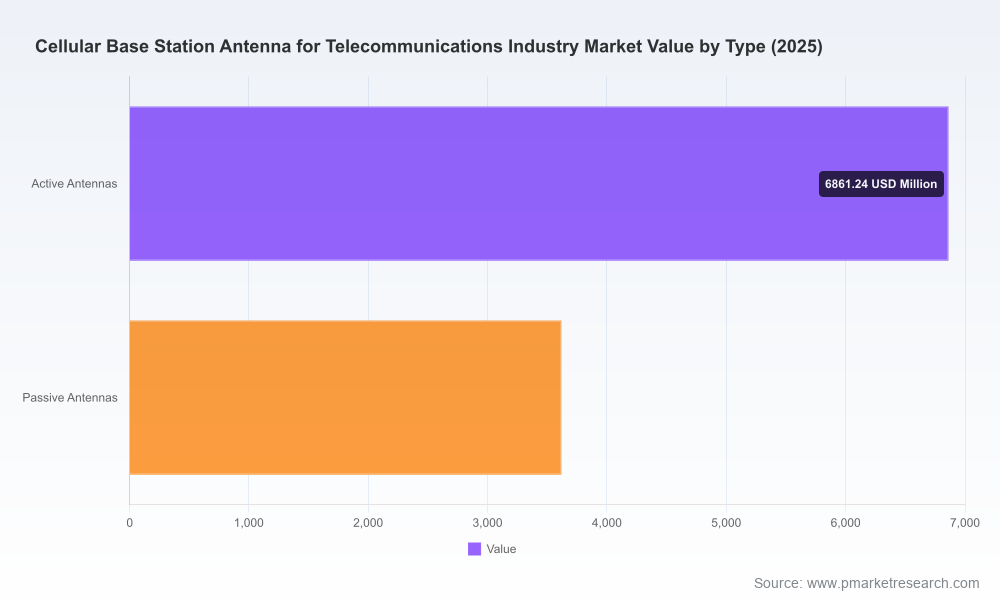

The market for cellular base station antennas has moved from an early 2020 baseline to a materially larger ecosystem by mid-decade. PW Consulting’s model shows growth from the low single-digit billions in 2020 to a 2025 base exceeding USD 10 billion, with a projected expansion to roughly USD 27.9 billion by 2032. The forecast period (2026–2032) implies a robust compound annual growth rate (CAGR) of approximately 15%. This pace reflects simultaneous tailwinds: accelerated 5G macro and small cell rollouts, ongoing technology refresh cycles (including Massive MIMO and multi-band solutions), and regulatory moves that aim to streamline deployment friction.

Cellular Base Station Antenna For Telecommunications Industry Market

Capital planning and vendor selection: With volume demand and unit complexity increasing, 2026 procurement decisions will determine 3–5 year operating and upgrade costs. Our report translates market trajectories into procurement scenarios that quantify trade-offs between capex efficiency and long-term operational expenditure.

Cellular Base Station Antenna For Telecommunications Industry Market

Network architecture and modernization timing: Operators face a hybrid decision matrix — where to densify with small cells versus where to upgrade macrocells with active and hybrid antenna systems. The research offers scenario-based sensitivity analyses that stress-test coverage, throughput, and TCO under divergent spectrum and densification assumptions.

M&A and partnership prioritization: A concentrated vendor landscape means strategic partnerships, acquisitions, or distribution agreements can yield immediate scale and differentiation. We provide an M&A playbook that maps asset types, capabilities, and value-creation levers against a measured market concentration profile.

Regulatory risk management: Recent and proposed regulatory changes materially alter deployment economics — from expedited modification approvals to potential new mid‑band spectrum auctions. The report quantifies the strategic upside and downside of these shifts for different go-to-market pathways.

Comprehensive market sizing and forecasting model: Transparent methodology, baseline assumptions for 2020–2025, and scenario-based projections through 2032 that translate macro demand into component-level and system-level implications.

Supply-chain and manufacturing analysis: Detailed assessments of supplier capacity, critical components (RF chains, connectors, RU/Antenna integration), and logistics sensitivities that influence lead times and pricing volatility.

Vendor evaluation matrix and strategic profiles: Independent scorecards across technology breadth, manufacturing footprint, product roadmap, regulatory compliance posture, and service delivery capabilities. These are coupled with go-to-market playbooks customized for tier-1 operators, regional integrators and neutral-host providers.

Deployment economics and ROI models: Practical tools to calculate break-even points for macro upgrades vs. small-cell densification, factoring in installation, maintenance, and energy costs as well as spectrum scenarios.

Regulatory and standards implications: Forward-looking analyses of regulatory proposals and standards work (including the latest industry recommendations) with clear decision triggers for deferring, accelerating, or altering deployment plans.

Risk register and mitigation plans: For program directors — prioritized operational, technical and regulatory risks with concrete mitigation actions and estimated residual exposure.

The base station antenna market is meaningfully concentrated: the top three vendors account for a material majority of market share, while the top five hold north of 80% — an important backdrop for strategic sourcing. Against that concentrated core, a set of specialized and regional players provide complementary capabilities, local manufacturing advantages, or cost-competitive alternatives tailored to specific operator needs.

Huawei Technologies Co. Ltd. — Global breadth in passive and active antenna portfolios, with strong Massive MIMO and multi-band capabilities aimed at high‑port density macro deployments and energy efficiency.

Ericsson AB — Integrates antenna systems tightly with radio access infrastructure (EAS), offering passive, active and hybrid solutions that optimize multi-band and Massive MIMO performance for large operator bases.

Nokia Corporation — Focused on multi-band and Massive MIMO antennas optimized for both dense urban and rural 5G scenarios, with integration into AirScale and broader system-level solutions.

CommScope Holding Company, Inc. — Emphasizes scalable RF platforms and distributed antenna systems for hybrid LTE/5G deployments, addressing both macro and small-cell needs.

Regional and specialized vendors — Companies such as Amphenol Procom, Comba Telecom, Rosenberger, RFS, ACE Technologies, Tongyu, PROSE, JMA Wireless, Alpha Wireless and HUBER+SUHNER represent a mix of high-performance niche products, supply-chain resilience, and regulatory-compliant manufacturing propositions.

For procurement and technology teams, the competitive takeaway is simple: expect a two‑tier dynamic where global system integrators drive platform-level decisions and specialized vendors provide tactical alternatives for cost, lead-time, or compliance-sensitive deployments.

Regulatory streamlining in the U.S.: Recent and proposed measures seek to reduce barriers to network modernization and ease certain local permitting constraints. These moves shorten deployment cycles and alter the equation for retrofit versus greenfield investments.

Spectrum dynamics: Policy actions to repurpose mid-band spectrum for terrestrial 5G will create windows of accelerated commercial opportunity — but also timing uncertainty. Operators and vendors must adopt flexible roadmaps that accommodate auction calendars and guard-band constraints.

Standards and common frameworks: Industry recommendations released in 2025 introduced updated nomenclature and rules for describing passive, active and hybrid systems. Standardization reduces integration risk but increases the pace at which product portfolios must evolve.

Product-level innovation: New radio units and compact Massive MIMO RUs announced in 2026 underscore a trend toward higher throughput-per-rack and improved energy efficiency — a decisive factor in operators’ TCO calculations.

Operational constraints: High installation and maintenance costs, coupled with spectrum scarcity in certain bands, remain key obstacles to densification. Conversely, passive antenna design improvements can deliver measurable energy and cell-edge throughput gains — studies show that modest beam-efficiency improvements can translate into double-digit throughput increases at the cell edge while lowering radio energy consumption.

For network operators — adopt a staged modernization plan that preserves optionality: prioritize upgrades where spectrum and traffic economics align, and defer high-cost densification until regulatory and spectrum clarity is achieved. Use the report’s ROI models to make site-by-site go/no-go decisions.

For equipment vendors — invest in modular product architectures and certification-ready designs that reduce integration friction. Pursue channel partnerships with regional suppliers to hedge supply-chain risk and address local compliance needs.

For private equity and strategic investors — target bolt-on acquisitions that add either specialized antenna design capabilities or domestic manufacturing footprints in markets with regulatory-driven sourcing preferences.

For systems integrators and tower companies — re-price service contracts to reflect higher complexity and energy management services; offer integrated deployment bundles that combine passive and active equipment with life‑cycle services.

For public sector stakeholders — monitor auction calendars and permitting reforms closely. Even incremental reductions in deployment friction can significantly shorten payback periods for new infrastructure investments.

This preview highlights the strategic framing of our full-length market study, which contains the granular deliverables, proprietary scenario models and vendor scorecards that are purpose-built to inform 2026 decisions. In keeping with our “trailer” approach, detailed segmentation tables, regional and application splits, and certain granular revenue-by-segment figures are intentionally withheld from this public summary to preserve the value of the full subscription report.

Clients who require immediate support can engage PW Consulting for tailored workshops, custom scenario modeling, and vendor due-diligence support that leverages the full dataset and our specialist analyst network. For access to the complete report and interactive modeling workbooks, please visit our report page or contact your account representative.

For detailed analysis of this topic, please visit the official page:Cellular Base Station Antenna For Telecommunications Industry Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com