Normal Dodecyl Mercaptan Market: Strategic Imperatives for 2026 — PW Consulting Insight

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concentrated briefing on the Normal Dodecyl Mercaptan (NDM / n-Dodecyl Mercaptan) market to inform corporate decision-making in 2026. This piece synthesizes the analytical thrust of our newly released market study while preserving the high-value, proprietary segment detail that makes the full report an essential subscription asset. Consider this a tactical trailer: it reveals methodology, strategic conclusions, and recommended actions — and points directly to the full intelligence suite that boards, procurement teams, and R&D leaders will need to execute confidently in 2026.

Normal Dodecyl Mercaptan Market

Executive snapshot: Where the market stands and where it’s headed

NDM is a narrowly focused but strategically important specialty chemical used primarily as a chain transfer agent in polymerization, an intermediate in antioxidant and additive synthesis, and historically as a flotation reagent in some mining contexts. Our analysis uses 2025 as the base year. The global NDM market grew from a mid-three-digit million USD level in 2020 to an estimated USD 205.9 Million in 2025 and, under our central scenario, is projected to reach roughly USD 280.1 Million by 2032. That outlook implies a steady compound annual growth rate of approximately 4.5% across the forecast window (2026–2032).

Normal Dodecyl Mercaptan Market

These headline numbers belie important structural dynamics: demand is being shaped by polymer industry cycles, regional capacity shifts, and an intensified regulatory and EHS agenda — each of which materially affects sourcing, cost pass-through, and substitution risk.

Normal Dodecyl Mercaptan Market

Why this matters for 2026 planning

- Procurement and supply security: The NDM value chain remains concentrated: the top three suppliers control the majority share of global supply, with the top five firms holding an even larger portion. This concentration amplifies counterparty risk and negotiating leverage for large-volume buyers.

- Cost and margin pressure: Upstream feedstock sensitivity — specifically hydrocarbons and sulfur streams tied to dodecene and hydrogen sulfide availability — creates episodic cost swings. Firms that lock tiered supply or implement feedstock-linked hedging will be advantaged in 2026.

- Regulatory & EHS compliance: Persistent odor issues and stricter EHS standards are increasing operational constraints on manufacturing, storage, transportation, and on-site use. In some industrial cases, this has catalyzed product substitution or process optimization.

- Application risk and opportunity: Polymer producers remain the primary end users for NDM, but changes in polymerization technologies, evolving additive chemistries, and targeted R&D investments can shift demand intensity across applications.

Market dynamics: drivers, constraints and tactical inflection points

- Application-led momentum: Polymerization uses continue to underpin volume growth, but the pace is uneven across polymer types and geographies. Selective gains in specialty polymers and ABS/PMMA value chains sustain demand for controlled chain-transfer agents.

- Raw material and process economics: NDM production routes — typically via organosulfur synthesis from alcohol precursors and halide intermediates, or through olefin-based thiolation — tie producer margins to crude derivatives and sulfur commodity cycles. Our marginal-cost modelling shows that small moves in feedstock costs can disproportionately affect low-cost producers.

- Regulatory pressure & substitution risk: New EHS controls and the reputational costs associated with odorous thiols are prompting some end-users to reassess reagent selections. The September 2025 operational case where a mining project removed NDM from a flotation process illustrates how cost and EH&S optimization can rapidly eliminate specific industrial uses.

- Concentration & capacity choreography: High concentration among leading suppliers creates both risks and levers. Buyers face potential supply tightness during maintenance or force majeure events, yet can also negotiate integrated service-level agreements with large producers who offer bundled logistics and stewardship programs.

Competitive landscape: players to watch

The market is a mix of global petrochemical majors, specialty chemical houses, and regional manufacturers. Globally recognized producers bring scale, compliance frameworks, and multi-modal distribution; regional players offer cost-competitive supply and local logistical advantages in key demand centers.

- Major integrated producers with global reach deliver reliability and stewardship services that matter to multinational polymer manufacturers and formulators.

- Regional manufacturers and specialty chemical firms—notably several established suppliers in Asia and India—remain important for spot supply and price-sensitive segments.

- Market concentration metrics underscore a dual reality: dominant suppliers can dictate commercial terms, while a competitive fringescape creates opportunities for localized arbitrage and niche service offerings.

PW Consulting’s named-company intelligence in the full report includes supplier profiles, capability maps, and a commercial strength matrix that ranks firms on service breadth, regulatory compliance, unit-cost positioning, and product stewardship. This is where procurement teams should focus supplier development and qualification work in 2026.

What the PW Consulting report delivers (practical tools)

The full study is built as a pragmatic playbook for executives and practitioners. Key deliverables include:

- Proprietary demand model with scenario-driven forecasts (base, downside, upside) mapped to end-use polymer and additive trends.

- Supply-side cost curve and marginal-cost sensitivity analysis linked to hydrocarbon and sulfur feedstock price scenarios.

- Supplier scorecards and an RFP template optimized for NDM procurement, including ESG and odor-mitigation contractual clauses.

- Regulatory & EHS heatmap by jurisdiction with mitigation playbooks for storage, transport, and plant-level odor control.

- Switching and substitution playbooks for end-users — technical feasibility checklists and impact assessments for reformulation or process changes.

- M&A and partnership diagnostic: target archetypes, integration risk factors, and estimated synergies for midstream consolidation.

These tools are designed to be operationally actionable — not just descriptive. They enable procurement, operations, and R&D leaders to convert market intelligence into supplier contracts, plant investments, and formulation decisions in 2026.

Strategic recommendations for 2026

Based on our analysis, we recommend that companies align around six pragmatic priorities:

- Hedge and tier purchases: Establish a two-tier supplier roster: secure firm contracts with high-integrity global suppliers for critical volumes, and maintain secondary regional sources for spot flexibility and price arbitrage.

- Lock in feedstock linkages: Negotiate feedstock-passthrough or floor/ceiling mechanisms with NDM suppliers to stabilize input cost exposure tied to hydrocarbon and sulfur swings.

- Invest in EHS and odor mitigation: For producers and large users, near-term capital spend on containment, closed-loop transfer, and odour abatement delivers clear risk reduction and insurance-premium benefits.

- Validate substitution pathways: Commission short-run trials for processes where NDM can be replaced or minimized; quantify TCO implications including regulatory and waste-management differentials.

- Use supplier scorecards aggressively: Insist on third-party certification, compliance roadmaps, and incident-response SLAs as part of procurement criteria — not as afterthoughts.

- Scan for M&A arbitrage: Consider bolt-on acquisitions in regions where logistics or feedstock access can materially compress unit costs, and seek partnerships that offer integrated supply+stewardship solutions.

Decision support for 2026: how our report helps

Leaders who treat the NDM market as a commoditized purchase risk under-allocating strategic attention. In contrast, the integrated view we provide translates market forecasts and supplier anatomy into executable steps: contract renegotiation templates, risk-adjusted inventory rules, capex gating criteria for odor-control investments, and prioritized R&D paths for substitution or concentration reduction.

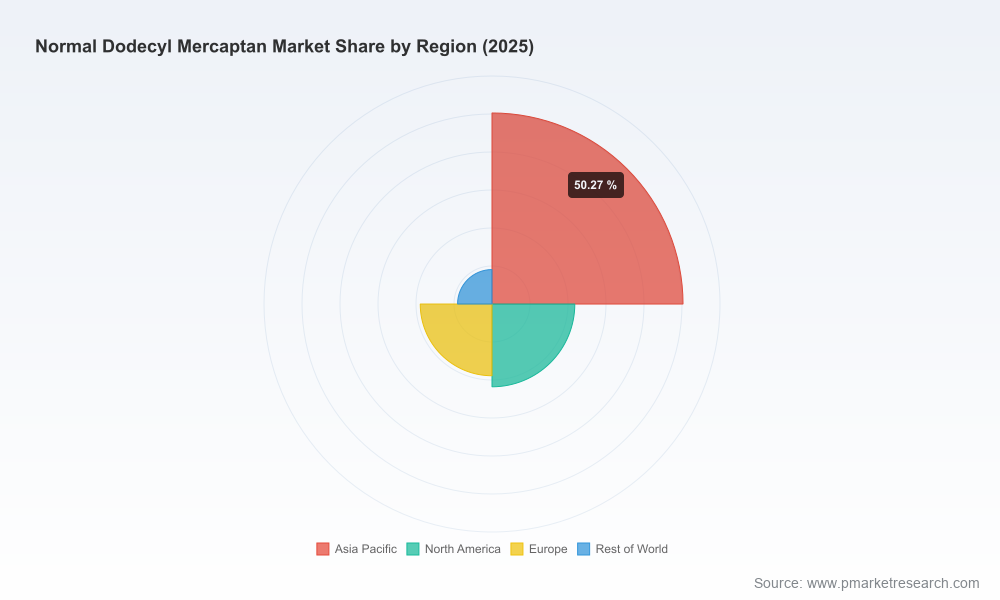

We intentionally withhold the granular regional and application split tables from this briefing — those calibrated segment-level figures, price projections, and supplier-specific capacity maps appear in the full report and the accompanying digital dashboard. That level of granularity is what materially changes supplier negotiation outcomes and capex prioritization.

Closing — next steps

For procurement directors, R&D heads, and corporate strategy teams preparing 2026 plans, the question is not whether to act — it is which of the recommended levers to deploy first. Our central scenario signals steady market expansion with manageable but asymmetric risks: concentration-driven supply risk, feedstock price volatility, and regulatory-driven substitution events.

Accessing the full PW Consulting NDM Market Report and interactive tools will equip your team to: quantify exposure, design contractual protections, prioritize capex, and identify acquisition targets with defensible synergies. Visit the PW Consulting research portal to view the full table of contents, sample report sections, and subscription options — the segment-level intelligence and supplier-specific modules are available only through the full report.

For bespoke briefings, scenario workshops, or to commission a customized supplier due-diligence, contact our Strategy Services team. PW Consulting’s methodology and on-the-ground supplier checks are designed to convert market intelligence into measurable commercial advantage in 2026.

For detailed analysis of this topic, please visit the official page:Normal Dodecyl Mercaptan Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com