Ytterbium‑176 Market Outlook 2026: Strategic Imperatives for Life‑Sciences Buyers, Producers and Investors

PW Consulting’s new Ytterbium‑176 Market report (base year 2025, forecast 2026–2032) equips corporate leaders with the intelligence needed to make high‑stakes procurement, investment and partnership decisions in 2026. The market is moving from niche research commodity to strategic component in the radiopharmaceutical and precision‑tech value chains. Our top‑line estimate shows the market expanding from approximately USD 12.45 Million in 2020 to USD 37.20 Million in 2025, with a projected uptick to roughly USD 46.92 Million in 2026 and long‑term growth to an estimated USD 175.95 Million by 2032. That trajectory implies a compound annual growth rate of c. 24.85% over the forecast horizon — a pace that demands proactive strategy rather than reactive buying.

Ytterbium-176 Market

Executive summary: why 2026 is a strategic inflection

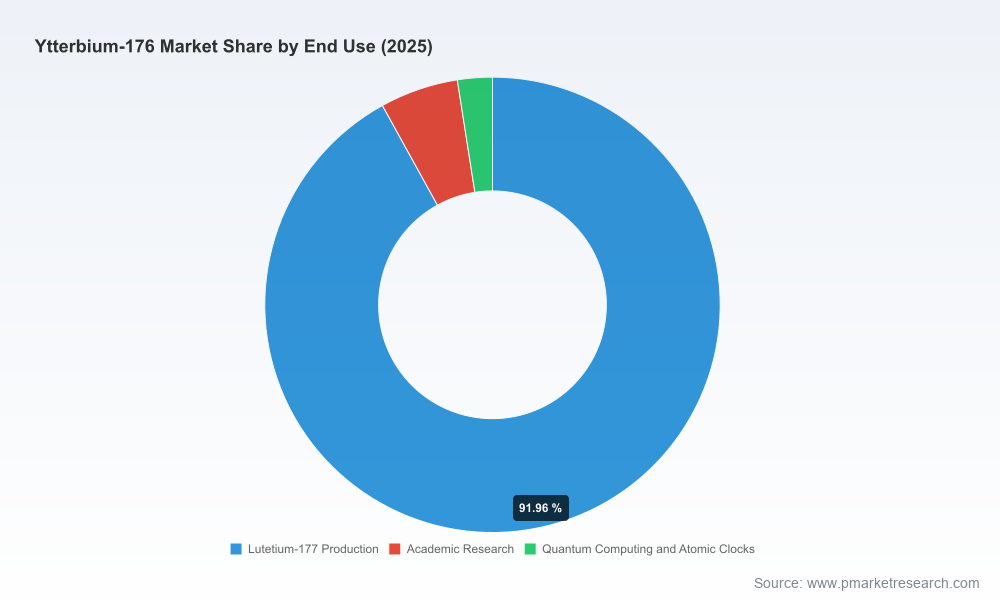

- Supply security has moved to the top of boardroom agendas. Yb‑176 is a critical precursor in no‑carrier‑added Lu‑177 production; historically concentrated sourcing has created geopolitical and logistical vulnerabilities that many organizations can no longer accept.

- Market structure amplifies price and availability sensitivity. Measured concentration indicators point to an oligopolistic supply base; a small number of advanced producers account for the bulk of commercial supply, elevating the value of supplier relationships and the leverage of new entrants who can scale rapidly.

- Technological bifurcation is creating durable differentiation. Producers using electromagnetic isotope separation and those deploying laser‑based quantum enrichment are establishing divergent cost structures, scale‑up paths and intellectual property moats — implications that affect long‑term contracting and M&A calculus.

- Regulatory and handling requirements remain non‑trivial. Export controls, nuclear safety standards and documented chain‑of‑custody for medical‑grade material create entry barriers for new suppliers and friction for buyers seeking rapid qualification of alternate sources.

Data‑driven signals you cannot ignore

Our modelling blends historical shipments, confirmed commercial launches and supplier disclosures to create a high‑confidence top‑line view. The rapid acceleration from 2020 to 2025 — more than tripling in five years — is driven by the maturation of Lu‑177 demand, increased clinical adoption of targeted radionuclide therapies, and deliberate supplier investment to broaden non‑Russian sources. The forecast for 2026 captures the immediate impact of new Western production capacity coming online and the early commercialisation of alternative enrichment technologies.

Ytterbium-176 Market

Two structural observations stand out for decision‑makers: first, volatility in supply will remain a staple risk until multiple producers mature their scale economics; second, buyers who secure multi‑year commitments now will reduce cost volatility and ensure predictable access to medical‑grade targets.

Ytterbium-176 Market

Competitive landscape: capabilities, risks and what they mean for buyers

The supply ecosystem is heterogeneous, combining government programs, legacy international suppliers, and several fast‑moving private producers. Our qualitative assessment of leading participants highlights strategic positioning rather than confidential commercial metrics:

- Technology disruptors (laser‑based entrants) — New‑generation enrichment approaches promise lower marginal costs at scale and the potential to generate differentiated product forms. Early commercial sample shipments in 2025 validate technical viability, but ramp risk and regulatory validation remain execution items for buyers evaluating offtake agreements.

- Established electromagnetic separation producers — Firms that commercialised via electromagnetic isotope separation have transitioned from pilot to steady shipments and are prioritising capacity expansion and supply reliability. These organisations offer a lower execution risk profile for immediate procurement, making them attractive for supply contracts that need short lead times.

- Government and national lab programs — National isotope programs provide important research‑scale volumes and strategic backstops, but their mandates and distribution rules often preclude commercial resale. They are critical for foundational R&D and emergency substitution scenarios, yet not a replacement for commercial supply chains.

- Legacy international suppliers — Long‑standing suppliers continue to serve reactor‑based irradiation markets and maintain important customer relationships. Geopolitical dynamics make their role more complex; buyers must balance historical reliability with elevated sovereign‑risk analysis.

For procurement leaders, the implication is clear: supplier selection must be driven by a matrix that weighs technology maturity, scale‑up roadmap, export and transport logistics, quality documentation and the supplier’s willingness to accommodate clinical‑grade audits and chain‑of‑custody requirements.

Operational and commercial playbook for 2026

- Dual‑sourcing with staged qualification: Contract a primary supplier for volume and a secondary for validation/contingency. Design qualification timelines and quality acceptance plans into contracts rather than treating them as post‑award activities.

- Structured offtakes and inventory strategies: Where product shelf‑life and regulatory constraints allow, negotiate multi‑year offtakes that include flexible delivery schedules and options to convert volume into processable targets. Maintain a calibrated safety stock while testing alternate formats.

- Supply‑chain as a competitive asset: Build upstream relationships with enrichment providers, irradiation facilities and radiochemistry partners. Consider strategic equity or JV stakes where securing priority access materially affects clinical timelines or product launches.

- Regulatory engagement and export planning: Ensure early engagement with regulators and customs authorities; build standardized documentation templates so that cross‑border shipments do not become clinical bottlenecks.

- Technology vigilance and IP assessment: Maintain a clear view of the technology roadmaps of key suppliers. Laser enrichment methods and next‑generation electromagnetic platforms have different licensing and capex profiles that affect mid‑term pricing and supply durability.

Report deliverables: what you’ll find inside (high level)

PW Consulting’s full report provides both strategic narrative and execution‑ready tools tailored for 2026 decision cycles. Highlights include:

- A validated top‑line market model covering 2020–2032 with scenario variants and sensitivity to clinical adoption and geopolitical stress events;

- A competitive vendor assessment that maps technology approach, commercial readiness, QC documentation practices and partner dependency profiles;

- Regulatory and logistics playbooks outlining documentation templates, common qualification hurdles and export control considerations for medical‑grade supply;

- Procurement templates — term‑sheet language, quality acceptance criteria, SLAs and contingency clauses designed for isotopes used in radiopharmaceutical manufacturing;

- Investment and M&A frameworks for assessing target valuation, technology risk, and time‑to‑commercialisation; and

- Stress‑test scenarios and an interactive dashboard for running supply‑shock and demand‑surge analyses to quantify inventory and cash‑flow impacts.

To maintain the utility of this release as a strategic “trailer,” the public summary intentionally omits granular regional splits, per‑application revenue shares and certain proprietary pricing curves. These items are available in the subscriber version and are often the difference between a tactical procurement decision and a transformative strategic position.

How corporate leaders should use this intelligence in 2026

- Boards and BD teams: Use the market trajectory and supplier readiness signals to prioritise capex, partnerships and potential equity stakes in upstream supply.

- Procurement and supply chain: Rework sourcing strategies to incorporate technology risk, regulatory timelines and multi‑leg supply agreements rather than single‑year spot buys.

- R&D and manufacturing: Align clinical development timelines with expected supply ramp milestones; anticipate qualification audits and integrate supplier variability into clinical supply strategies.

- Investors and M&A teams: Focus diligence on proven scale‑up capability, regulatory track records and IP ownership — those are the levers that convert early supply announcements into sustainable commercial positions.

Closing: the strategic window is now

2026 represents a decision horizon where exhibitors of capability become consolidators of market share. The Ytterbium‑176 market is transitioning fast: validated commercial samples, capacity expansions and national programme investments have shifted the conversation from “can it be produced reliably?” to “who can guarantee supply and at what contractual terms?”. Companies that move now — aligning procurement, regulatory and technical functions around an integrated sourcing and mitigation plan — will lock in competitive advantages that are difficult to replicate later.

For executives and investors preparing budgets, negotiating offtakes or conducting diligence, PW Consulting’s full Ytterbium‑176 Market report is a practical resource that translates market growth, supplier dynamics and regulatory complexity into actionable decisions. Visit our report page to access the complete dataset, regional breakdowns, price forecasts and supplier scorecards that underpin the strategic recommendations summarized here.

For detailed analysis of this topic, please visit the official page:Ytterbium-176 Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com