Bio-Based Superabsorbent Polymers for Hygiene Products: Strategic Imperatives for 2026

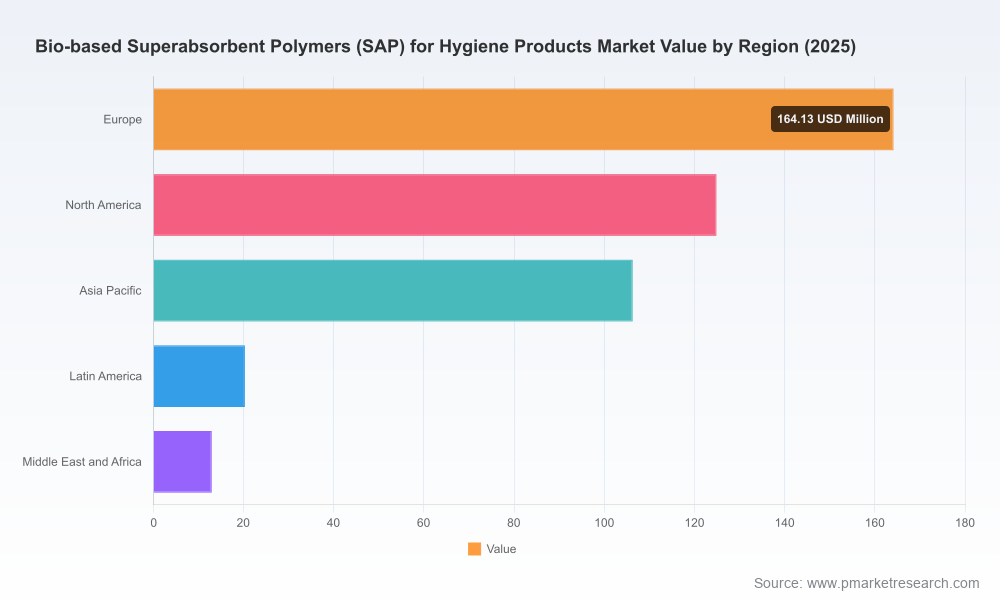

PW Consulting’s new market study on Bio-Based Superabsorbent Polymers (bio-SAP) for hygiene products synthesizes techno-commercial evidence and commercial intelligence to equip C-suite teams, product and supply chain leaders, and investors for decisive action in 2026. The bio-SAP opportunity is no longer hypothetical. From an overall market of approximately USD 428.5 Million in our 2025 base year, PW projects expansion to roughly USD 493.1 Million in 2026, and onward at a compound annual growth rate (CAGR) of about 13.98% through our 2026–2032 forecast horizon, reaching roughly USD 1.07 Billion by 2032. This trajectory creates a narrow window in which commercial-first players can convert sustainability advantage into durable market share.

Bio-Based Superabsorbent Polymers (SAP) for Hygiene Products Market

Why 2026 is a Pivot Year

- Technology readiness is crossing the chasm: multiple suppliers have moved from lab or pilot to validated industrial-line performance. Recent field validations and product launches demonstrate that bio-based formulations can match or outperform conventional acrylic SAP on existing diaper and pad production lines.

- Customer and regulatory pressure is crystallizing into procurement requirements. Leading brand owners are piloting and selectively integrating bio-SAP to lower product carbon footprints while preserving performance.

- Market economics are in flux. Higher unit costs and feedstock volatility remain structural realities, but scale and process innovation are driving down the total landed cost curve for several bio-SAP chemistries.

For executive teams, the practical implication is straightforward: 2026 will separate fast followers (who secure supply and validate integration) from laggards (who react defensively later at greater cost).

Bio-Based Superabsorbent Polymers (SAP) for Hygiene Products Market

Market Dynamics and Practical Risks

- Demand drivers: consumer sustainability preferences, retailer net-zero procurement commitments, and brand-level carbon accounting are underpinning demand beyond regulatory diktats. Hygiene product OEMs seeking end-to-end footprint reductions are increasingly focused on core materials like SAP.

- Supply-side constraints: bio-SAP production is currently costlier than established petroleum-derived acrylic SAP due to feedstock processing complexity and limited integrated supply. Feedstock availability and seasonality can introduce meaningful price volatility and require more sophisticated raw material contracting and inventory strategies.

- Manufacturing integration: the best-performing bio-SAP variants report compatibility with standard diaper and pad production lines, but manufacturers must validate across multiple core constructions to avoid operational surprises. Performance validation at scale—across sizes and core types—remains a gating factor for broad commercial adoption.

- Certification and traceability: mass-balance schemes and recognized sustainability certifications are becoming table stakes for customers to claim bio-based content and associated emissions reductions. Firms that can combine technical performance with auditable supply chain claims gain preferential access to premium procurement channels.

Competitive Landscape — What Leaders Are Doing

The competitive field is a mix of specialist start-ups, chemical multinationals, agricultural processors, and materials SMEs. Leading initiatives illustrate three pragmatic go-to-market models:

Bio-Based Superabsorbent Polymers (SAP) for Hygiene Products Market

- Start-up commercialisation and validation: companies focused exclusively on bio-SAP have accelerated industrialization, achieving line-level validation and commercial-scale launches that prove product parity with incumbent materials.

- Established chemical players leveraging existing routes: major polymer and specialty chemical manufacturers are introducing biomass-balanced or bio-sourced variants via mass-balance certification, combining supply chain scale with customer reach.

- Integrated agri-processing and co-development: agricultural processors and starch/cellulose specialists are partnering with polymer developers to control upstream feedstock and lower feedstock risk while enabling differentiated formulations.

Representative examples in the market illustrate these archetypes and the strategic choices they imply:

- ZymoChem (San Leandro, CA) — commercialized a scalable 100% bio-based and biodegradable SAP with independent validations on diaper production lines, signalling that a direct replacement for petroleum-derived SAP is commercially viable when the supplier invests in scale and process robustness.

- Planet Smart Products (London, UK) — launched a bioSAP positioned as biodegradable and microplastics-free and emphasizes drop-in compatibility, appealing to brand owners seeking immediate substitution without retooling.

- NAGASE & Co. / Nagase ChemteX — developing high-biomass-content bio-SAP with mass-production ramp plans, representing a supplier model that combines chemical expertise with commercial distribution networks.

- BASF, Nippon Shokubai and other large chemicals players — pursuing bio-sourced or biomass-balanced variants, leveraging certification schemes and existing industrial footprint to serve customers at scale.

- Agricultural and starch specialists (e.g., ADM, AquaSol) — pursuing starch- and cellulose-based approaches that can be advantaged by vertically integrated feedstock positions.

These different player models create a fertile environment for partnerships, licensing, and M&A as incumbents and challengers position around performance, cost-to-serve, and sustainability claims.

What Our Report Delivers — Operational, Decision-Grade Intelligence

PW Consulting’s report is designed as a practical playbook for 2026 decision-making. It combines rigorous forecasting with hands-on due diligence tools and commercial templates to accelerate deployment while managing risk. Key deliverables include:

- Scenario-driven market model: three strategic pathways that map adoption rates, price trajectories, and margin outcomes under alternative feedstock and certification assumptions. This model is parametrized so users can stress-test assumptions specific to their supply contracts.

- Supplier assessment framework: a standardized scorecard for technical readiness, industrial compatibility, certification status, feedstock sourcing, capex requirements, and commercial footprint — designed to support sourcing committees and investment memos.

- Techno-economic templates: modular calculators for total landed cost comparisons across chemistries and sourcing routes, incorporating logistics, certification premiums, waste handling, and rework risk.

- Pilot & scale-up playbook: step-by-step test plans for industrial validation across diaper sizes and pad constructions, acceptance criteria, and control plans to minimize line downtime during trials.

- Contractual & procurement toolkit: model offtake terms, option structures, volume-flex clauses, and incentive mechanisms to share scale-up capex and reduce supplier cash-flow constraints.

- Regulatory and claims roadmap: practical guidance on using mass-balance certification, carbon accounting approaches, and allowed marketing claims to avoid greenwash exposure while maximizing consumer value.

- Investment and M&A decision trees: valuation sensitivities and integration checklists for investors evaluating technology owners, feedstock players, or manufacturing partners.

Importantly, the report purposefully reserves certain granular subsegment matrices and live price curves for subscribers and commissioned clients. This "trailer" approach gives readers a clear line of sight into strategic implications while protecting the proprietary, transaction-grade data that deliver competitive advantage.

Strategic Priorities for Different Players in 2026

- Hygiene brand owners: move from lab pilots to industrial validation in prioritized SKUs, secure tiered supply agreements with technical acceptance gates, and develop differentiated value propositions (e.g., carbon reduction, biodegradability) tied to verified claims.

- OEMs / converters: invest in cross-functional trials to prove line compatibility, develop contingency plans for multiple bio-SAP chemistries, and require supplier warranties tied to production-line performance.

- SAP producers and chem companies: prioritize scale-up pathways that reduce unit cost; invest in feedstock partnerships or vertical integration to manage volatility; pursue recognized certifications to de-risk customer procurement cycles.

- Feedstock suppliers and agri-processors: model the incremental value chain capture from upstream integration and offer offtake+processing bundles to de-risk customer supply.

- Private equity and strategic investors: focus diligence on suppliers with validated industrial performance and defensible feedstock access; prioritize assets that shorten time-to-market for global brand owners.

How to Use This Intelligence in 2026

Short-term actions to convert insight into results:

- Initiate a prioritized pilot calendar with guaranteed evaluation metrics and cross-functional stakeholders to compress validation timelines.

- Negotiate staged supply agreements with option-based volumes to balance price premiums and security of supply as scale is proven.

- Adopt modular cost-modeling frameworks to estimate the true landed cost of bio-SAP variants under multiple feedstock and certification scenarios.

- Map certification and claims pathways early to align marketing, legal, and procurement teams and avoid rework that delays launches.

Conclusion — The Strategic Payoff

Bio-based SAP for hygiene products is transitioning from niche sustainability experiments to a mainstream materials play. The 2026 inflection point is characterized by validated industrial performance, nascent commercial rollouts, and evolving economics that reward early, disciplined scaling strategies. Our report translates these macro dynamics — supported by a clear market trajectory and practical supplier intelligence — into actionable roadmaps that help leaders decide where to invest, partner, or consolidate.

For executives preparing their 2026 strategic plan, the choice is pragmatic: invest in de-risked pilots and supply arrangements now, or accept higher execution risk and potential margin drag later. PW Consulting’s full report provides the transaction-grade data, supplier scorecards, and contractual templates that enable decisive action. Access to the full dataset and the live scenario models is available through our subscription and advisory services.

For detailed analysis of this topic, please visit the official page:Bio-Based Superabsorbent Polymers (SAP) for Hygiene Products Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com