Global Veal Market Size, Share & Forecast Report 2034

Food |

2026-05-07 11:55:22

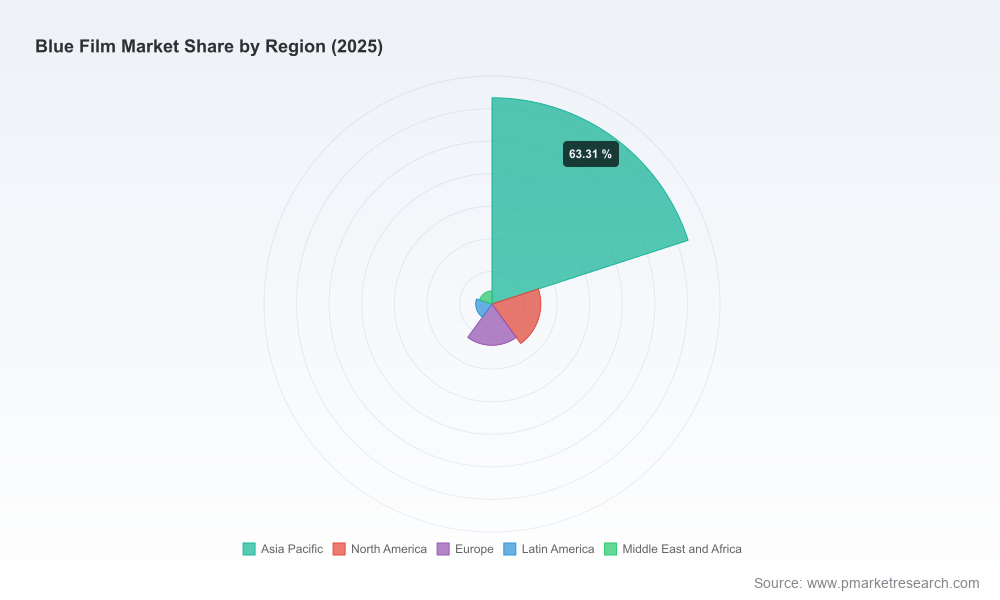

PW Consulting’s new Blue Film Market report is a practical, decision-focused intelligence product designed to shape corporate strategies in 2026 and beyond. The global market for blue films — including protective films, semiconductor dicing/backgrinding tapes, and related polymeric protection products — has marched from under USD 700 million in 2020 to roughly USD 970 million in our 2025 base year, and is projected to expand at a compound annual growth rate (CAGR) of 7.82% over our 2026–2032 forecast window. By 2032 the market is forecast to approach USD 1.64 billion (Million USD), reflecting both sustained end-market demand and material- and process-driven substitution dynamics.

Blue Film Market

Two converging dynamics make 2026 pivotal. First, semiconductor packaging and advanced wafer handling processes continue to press demand for higher‑performance, contamination‑free protective films. Second, upstream polymer markets are undergoing a supply shift: new polyethylene capacity comes online in the second half of 2026, altering global feedstock availability and buyer leverage. Our scenario work shows that when polyethylene availability expands, buyers can negotiate better terms; conversely, any petroleum‑price spike or supply disruption rapidly compresses margins for film manufacturers who are not equipped with hedging or long‑term procurement frameworks.

Blue Film Market

For decision makers, the implication is clear: 2026 is the year to translate strategic intent into tangible supply‑chain changes. Firms that pre‑position through contracts, qualification pipelines, and targeted product investments will capture outsized share and margin upside during the next expansion phase.

Blue Film Market

The blue film market is dominated by a handful of established materials and specialty film companies whose combined influence shapes standards, qualification pathways, and pricing. Major incumbents included in our analysis are long‑standing Japanese and global polymer players that have invested in tape adhesives, non‑UV polyester and polyolefin substrate technologies, and wafer‑level process qualifications.

Strategically, these vendors differentiate on adhesive technology, substrate formulation (polyolefin vs. PVC vs. PET approaches), contamination control, and the ability to support long qualification cycles with fabs. The competitive landscape favors companies that can combine material science depth with integrated supply‑chain resilience and regional manufacturing footprints.

Raw material movements are the most visible lever shaping near‑term margins. Polyethylene remains a primary feedstock for many polyolefin‑based blue films; global polyethylene production and pricing trends therefore cascade into film pricing. Our analysis incorporates recent industry intelligence showing significant new polyethylene capacity slated to come online in the second half of 2026 — a factor that is expected to ease buyer pressure in certain scenarios. At the same time, historical correlations between petroleum‑product price swings and polyethylene costs mean firms must model volatility in multi‑year planning.

On the regulatory side, many semiconductor‑grade films are evaluated against RoHS2 and related electronic materials restrictions; compliance is non‑negotiable for tier‑1 component suppliers and OEMs. This regulatory overlay increases certification timelines and can raise barriers for new entrants without established compliance systems.

Our downside scenarios emphasize three principal risks: persistent raw material inflation, prolonged qualification cycles driven by shifting fab requirements, and substitution risk from alternative protective approaches. Each risk carries distinct operational responses. For raw material inflation, hedging and long‑term supply agreements preserve gross margins; for qualification delays, co‑development with lead customers and early‑stage trials mitigate time to revenue; for substitution, continuous investment in differentiated material properties sustains barriers to replacement.

This report is crafted as an execution toolkit for 2026 planning. Recommended uses include:

With the blue film market growing from our 2025 base into a materially larger market by 2032, 2026 is a strategic window in which supply dynamics, raw material shifts, and qualification regimes intersect. Firms that convert insights into concrete procurement, product, and M&A actions will secure durable advantages. PW Consulting’s Blue Film Market report is structured to move teams from analysis to execution within the 2026 planning cycle.

For detailed segment-level forecasts, granular regional and application splits, the complete set of company profiles, and downloadable models that power our recommendations, please consult the full report on our website. The materials in that package contain the detailed datasets and appendices required to operationalize the strategic pathways outlined here.

For detailed analysis of this topic, please visit the official page:Blue Film Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com