Anticorrosion Tape Market — Strategic Briefing for 2026 Corporate Planning

PW Consulting’s latest industry briefing on the Anticorrosion Tape Market synthesizes a multi-year market model, competitive intelligence, and field-proven strategic options to support executive decision-making in 2026. Our baseline analysis (base year: 2025) finds the market at approximately USD 215.0 Million, having expanded steadily from the start of the decade. Under the central-case forecast the market grows at a compound annual rate of 5.37% through 2032, reaching roughly USD 345 Million by the end of the forecast window. That trajectory masks important inflection points—driven by raw material volatility, regulatory pressure, and targeted product innovation—that will determine which companies capture disproportionate value in the coming 18–36 months.

Anticorrosion Tape Market

Why this briefing matters for 2026

- Decision makers must move from tactical reactions (price, delivery) to strategic positioning (product architecture, regional footprint, service-bundling). The market scale is large enough to justify selective CAPEX but remains sufficiently fragmented to reward focused commercial plays.

- Unexpected shocks in feedstock costs and shifting compliance requirements are compressing margins for firms that rely on spot procurement or commodity formulations. Leading firms are already prioritizing low-VOC and RoHS-compliant formulations — a trend that will accelerate procurement and R&D trade-offs during 2026 planning cycles.

- Commercial opportunities are not evenly distributed: manufacturers that couple technical differentiation (adhesive chemistry, substrate compatibility) with field-proven installation support will outperform peers that compete on price alone.

Market dynamics and near-term drivers

The 2020–2025 historical period shows consistent growth underpinned by infrastructure maintenance needs across energy, water, and maritime sectors, plus an uptick in industrial retrofit projects. Over the 2026–2032 forecast horizon, the market’s 5.37% CAGR reflects a mix of steady replacement demand and selective growth where new formulations address sustainability and installation-efficiency concerns.

Anticorrosion Tape Market

Three dynamics will shape company outcomes in 2026:

Anticorrosion Tape Market

- Raw material volatility: Specialty polymers and aluminum foils—core inputs for many product constructions—show heightened price and availability swings. Firms with flexible sourcing strategies or partial vertical integration will preserve margins more effectively.

- Regulatory and sustainability pressures: Procurement teams increasingly demand reduced-VOC formulations and documentation for RoHS and other regional mandates. This is forcing product reformulation and certification investments that should be budgeted into 2026 plans.

- Customer buying behavior: Asset owners and EPCs place higher value on total lifecycle cost and installation assurance. Solutions that reduce on-site labor time, rework, and risk during commissioning are winning procurement evaluations.

What the full PW Consulting report delivers (operationally focused)

- Proprietary market sizing and scenario models (global and regional views; historical 2020–2025 and forecast 2026–2032) that allow you to run top-down and bottom-up planning scenarios for 2026 capital allocation and sales targets.

- Supply-chain deep dive including composition of primary feedstocks, price-sensitivity analysis, and five practical supplier-risk mitigation strategies you can implement in procurement cycles beginning Q1 2026.

- Competitor playbooks: validated commercial and technical profiles for major players, recent go-to-market moves, and tactical counters for mid-market challengers.

- Go-to-market frameworks tailored for manufacturers, distributors, and engineering contractors: channel segmentation, commercial incentives, and service-bundling templates proven in field pilots.

- Product and regulatory roadmaps: step-by-step guidance for reformulation to lower-VOC chemistries and checklist-based readiness for RoHS compliance.

- M&A and partnership screening matrix: criteria to evaluate tuck-in candidates and technology partners that accelerate entry into specialty segments (e.g., automotive-grade adhesive systems, offshore field-joint coatings).

Competitive landscape — what we observed and the implications

The competitive field is a mix of diversified industrial adhesives leaders, regional specialists, and niche technical suppliers. Large, global manufacturers continue to push product innovation and broaden distribution reach, while focused players defend technical niches or regional accounts by emphasizing local service and long-standing project relationships.

- Product innovation leaders are moving quickly on sustainability and performance. For example, major firms have launched reduced-VOC butyl and polymer formulations with improved adhesive profiles — an explicit response to procurement requirements and field performance feedback.

- Regional manufacturing and capacity investments by established adhesive groups are lowering lead times in key end markets and creating tactical advantages for customers that favor local supply continuity.

- Project-level wins (offshore field-joint systems, encapsulation of complex fittings) demonstrate that project execution capability is as important as product technology; companies that pair product with installation systems capture higher value.

For 2026 planning, these dynamics imply two practical moves for executives:

- If you are a global manufacturer: prioritize modular product lines that can be localized quickly, protect margins via a mixed strategy of long-term raw material contracts and selective hedges, and invest in field-installation training to raise switching costs for customers.

- If you are a regional specialist or distributor: double down on technical support and certification services, use targeted alliances with chemistry innovators to access differentiated formulations, and deploy “coating-as-a-service” pilots to demonstrate lifecycle cost advantages.

Recent industry activity that informs 2026 choices

- New eco-friendly product launches have validated market readiness for reduced-VOC formulations — a commercial lever that can unlock access to sustainability-mandated procurement pools.

- Capacity expansions in Southeast Asia and other supply hubs are creating shorter lead-time options — a factor that buyers will include in 2026 sourcing decisions.

- Continued project deployments by systems providers in offshore and land-based energy projects highlight the value of proven field systems and accredited installation partners.

Supply chain resilience and cost management: an actionable checklist

- Map critical-feedstock exposure by product family and run a 12–24 month price-sensitivity stress test for planning.

- Negotiate phased multi-year supply agreements with indexation clauses that cap downside while allowing upside capture for suppliers.

- Evaluate forward-integration options selectively (blending or tape lamination capacity) where payback can be demonstrated within 36 months under conservative demand scenarios.

- Implement a certification program for recyclate or recycled-content inputs to hedge against both cost spikes and incoming sustainability mandates.

How executives should use this briefing in 2026 planning cycles

Use the market and commercial insights in this briefing to inform three concrete planning deliverables for 2026:

- Year-one investment portfolio: allocate funds across product development, targeted capacity expansion, and service pilot programs with explicit ROI triggers tied to the scenario model.

- Go-to-market sprint: design a 6–9 month commercialization sprint for one differentiated product or service offering to validate pricing and installation economics before broader rollout.

- Procurement playbook: deploy supplier-risk mitigations and a scorecard for raw material partners that captures quality, sustainability credentials, capacity, and financial resilience.

Competitive positioning — tactical advice by player type

- Incumbent global manufacturers: convert R&D into modular manufacturing runs so new formulations can be tested regionally without large upfront tooling costs. Use brand and distribution strength to codify installation standards and certification programs.

- Mid-sized technical specialists: leverage nimbleness to pilot advanced adhesive chemistries with strategic end-users, and monetize technical know-how through installation consulting and warranty products.

- Distributors and EPCs: integrate supply agreements with performance-backed service commitments; offering installation assurance materially improves capture rates in competitive tenders.

What we are deliberately withholding here — and why you should consult the full report

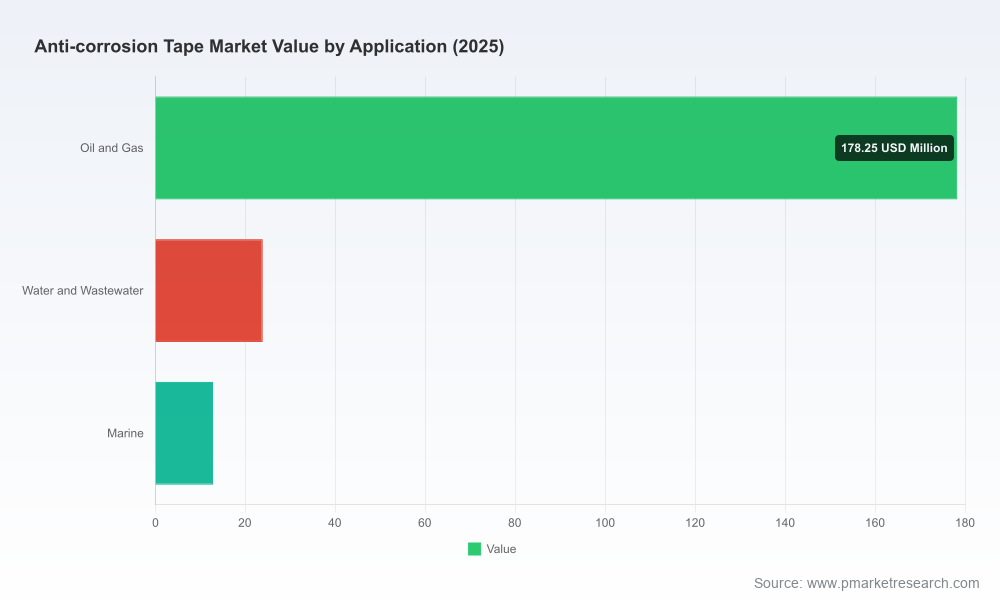

To preserve actionable differentiation for clients and maintain the “trailer” integrity of this briefing, we have intentionally omitted granular regional and application-level market splits and specific numeric shares across product types. The full report contains those detailed segmentations, disaggregated demand curves, and downloadable scenario models that are necessary for precise target-setting, territory planning, and acquisition screening. If you are preparing 2026 budgets, tariff models, or M&A pipelines, access to the detailed tables and sensitivity runs in the complete dataset is essential.

Next steps

Executives preparing 2026 plans should request the full PW Consulting Anticorrosion Tape Market report to obtain the complete market model, supplier scorecards, and customizable scenario templates. With that data you can set defensible sales targets, prioritize R&D spend, and establish procurement tactics that balance cost, compliance, and continuity.

PW Consulting is available to run a tailored strategy workshop that maps your product portfolio against the forecast scenarios and produces a prioritized 90-day action plan aligned to your 2026 budget cycle.

For detailed analysis of this topic, please visit the official page:Anticorrosion Tape Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com