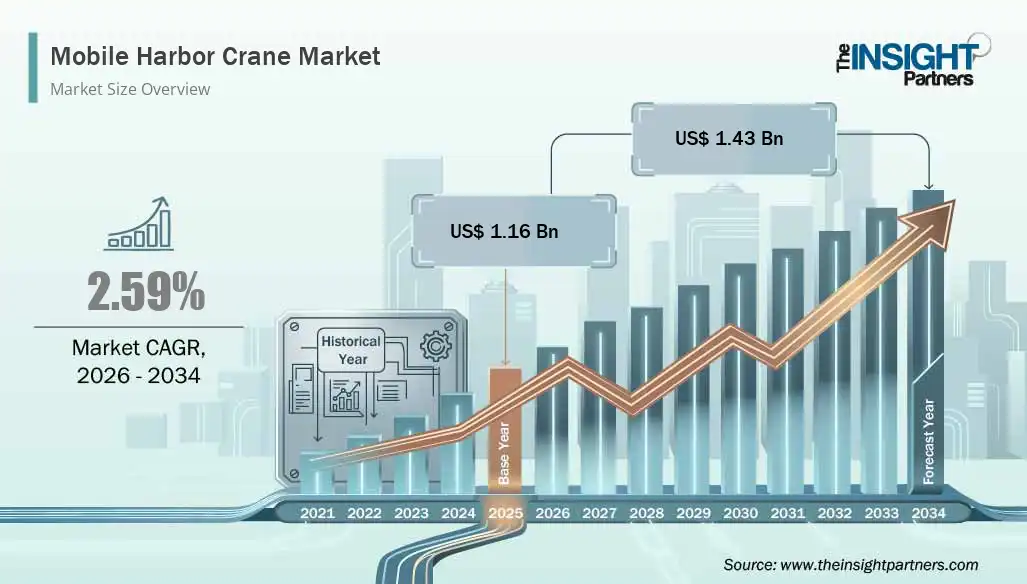

North America Mobile Harbor Crane Market Driven by Port Infrastructure Investments

Literature |

2026-06-25 13:14:10

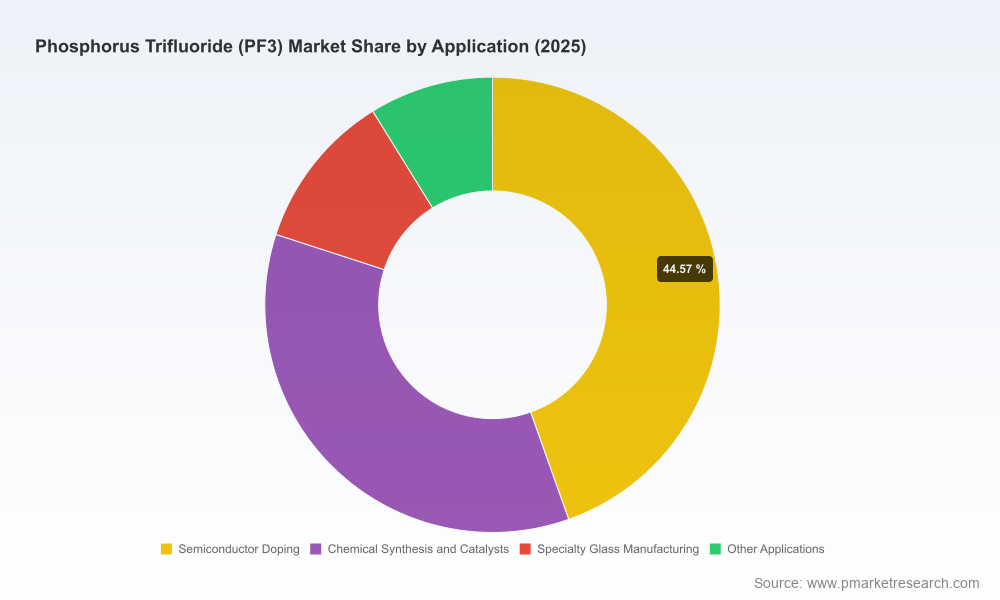

Phosphorus trifluoride (PF3) occupies an outsized strategic position across semiconductor fabrication, chemical synthesis, and several specialty manufacturing flows. PW Consulting’s latest market analysis shows a clear upward trajectory: the global PF3 market expanded from the low‑50s (USD Million) in 2020 to just over USD 72 Million by the 2025 base year, and is forecast to continue growing at a mid‑single digit compound annual growth rate through 2032 — reaching roughly USD 120 Million by the end of the forecast window. For corporate decision‑makers planning capital allocation, procurement strategy, and supply‑chain resilience in 2026, PF3 is no longer a niche tail spend; it is a strategically material input whose availability, purity and logistics profile materially affect product yields, time‑to‑market and margin capture.

Phosphorus Trifluoride (PF3) Market

Two planning horizons collide in 2026. Near‑term operational questions — cylinder qualification, purity grade conversion, logistics bottlenecks — sit alongside medium‑term portfolio choices such as capacity investment, supplier consolidation and M&A. Our PF3 research bridges these horizons by quantifying market scale, projecting plausible demand curves and, critically, translating those projections into actionable procurement and risk‑management playbooks. The result is a report designed to be used directly at the board‑room level and by category managers drafting next year’s supplier scorecards.

Phosphorus Trifluoride (PF3) Market

End‑market momentum. Semiconductor device scaling, advanced etch and ion‑implant processes, and growth in specialty chemical applications anchor PF3 demand. The base‑year market size and forecast trajectory reflect both cyclical and structural demand elements: cyclical capacity ramps in semiconductor fabs and structural migration of specialty synthesis workflows that require phosphorus fluoride chemistries.

Phosphorus Trifluoride (PF3) Market

Grade differentiation. Electronic‑grade PF3 with ultra‑low impurities remains the primary growth vector due to escalating purity demands from next‑generation logic and memory nodes. Industrial and research grades continue to serve legacy chemical synthesis and lab markets, but the revenue mix is shifting toward higher value, higher‑specification offerings.

Consolidation of use cases. As manufacturers converge on fewer, more standardized chemistries for critical etch and deposition recipes, procurement teams can anticipate concentrated demand windows and supplier qualification bottlenecks during fab ramp cycles.

The supplier map combines global specialty gas leaders, regional chemical producers and boutique vendors focused on small‑volume high‑purity packaging. Key strategic positions to note:

Large specialty gas suppliers have advantages in global logistics, multi‑site qualification and long‑term contracts. Their product portfolios emphasize ultra‑pure grades and cylinder packaging solutions that support stable supply for high‑demand fabrication customers.

Independent manufacturers and regional producers compete on price flexibility and rapid batch turn‑around, offering multiple packaging forms from ampules and bubblers to bulk cylinders. These players are important tactical partners for non‑production or laboratory needs and for customers seeking alternative supply during ramp phases.

China‑based producers serve both domestic and export demand with competitive pricing and scaling potential. For multinational buyers, their presence creates both opportunity (additional capacity options) and complexity (qualification, regulatory scrutiny, trade friction).

Our report profiles the leading vendors, detailing purity grades offered, packaging innovations, qualification timelines and the strategic tradeoffs between global majors and regional specialists. (Full vendor scorecards, comparative performance matrices and supplier playbooks are reserved for the full report.)

Raw‑material volatility. Recent disruptions in upstream feedstocks have proven how sensitive PF3 economics and margin structures are to commodity swings. Dramatic price movements in key precursors within the past two years should prompt procurement teams to run stress scenarios and to incorporate raw‑material escalation clauses into supplier contracts.

Tariff and trade friction. 2025 policy actions — including elevated tariffs on specialty chemical intermediates and further tariff escalation affecting semiconductor equipment and inputs — have already altered sourcing strategies. Buyers must now factor potential tariff headwinds into landed cost models, qualification lead times and near‑sourcing decisions.

Regulatory and safety considerations. PF3 handling, storage and transportation require disciplined compliance. Recent tightening in hazardous materials routing and cylinder packaging standards increases the importance of supplier competence in logistics and documentation.

Below are priority actions we recommend for procurement, operations and corporate development teams preparing plans for 2026:

Segregate by criticality. Classify PF3 usage into strategic (fab critical), tactical (pilot lines and labs), and discretionary (R&D, small‑batch synthesis). This enables differentiated sourcing rules: long‑term supply agreements and capacity options for strategic use; flexible, shorter contracts for tactical needs.

Adopt multi‑axis supplier selection. Evaluate suppliers not only on price and purity, but also on packaging innovation, cylinder exchange programs, qualification lead times, and export compliance capabilities. Neglecting logistics competency is a false economy for high‑sensitivity applications.

Invest in qualification pipelines now. Supplier qualification timelines for electronic‑grade PF3 can be lengthy. Start parallel qualifications with at least two vetted suppliers to reduce single‑source risk and preserve production continuity during fab ramps or tariff‑induced re‑routing.

Hedge raw‑material exposure. Work with suppliers to develop cost‑pass and cost‑share mechanisms, or consider financial hedges for key precursors where feasible. Hedging strategies should be scenario‑driven and periodically reassessed as market structure evolves.

Localize critical inventories selectively. For companies exposed to high tariff jurisdictions or concentrated manufacturing footprints, localized buffer inventories or near‑sourcing can be a prudent insurance policy against border delays and tariff shocks.

Embed PF3 into product roadmaps. Technical teams should model PF3 availability and purity limits as design constraints. Early alignment between materials, process engineering and procurement reduces costly late‑stage reformulations.

Our modelling considers three plausible scenarios that should inform board‑level capital allocation decisions:

Baseline growth aligned with current fab roadmaps and chemical demand expansion.

Upside with accelerated semiconductor capacity additions and faster adoption of PF3‑dependent chemistries in specialty manufacturing.

Stress case driven by extended tariff regimes, a sustained spike in precursor costs, or a concentrated supply disruption from one major geographic cluster.

Each scenario is paired with action triggers and financial stress signals so that decision‑makers can translate market movements into pre‑defined responses rather than ad‑hoc reactions.

The full report is designed as an operational toolkit for 2026 planners, including:

A granular supply‑demand model covering historical trends and multi‑scenario forecasts through 2032, with sensitivity analyses and demand‑by‑use‑case drivers.

Supplier scorecards and qualification timelines for global majors and regional producers, including detailed evaluation criteria for purity specification, packaging, logistics and compliance.

Commercial playbooks: sample RFP templates, contract clauses for raw‑material pass‑through, inventory trigger policies, and negotiation levers tuned to PF3 market dynamics.

Risk matrices and recommended mitigations for trade policy shocks, raw‑material price spikes and logistics failures, plus playbooks for rapid supplier substitution.

Packaging and logistics optimization guidance — how to reduce total landed cost through cylinder sizing, exchange programs and route optimization without compromising safety or purity.

Scenario‑based capital planning tools for CAPEX and M&A, identifying where vertical integration or strategic partnerships create defensible supply positions.

Note: the public summary is intentionally surfaced to provide strategic context. The report’s appendices contain the full datasets, supplier rankings, and the modeled tables that underlie our forecasts — available to subscribers and clients.

PF3 will reappear on more board agendas in 2026, not because it suddenly became a headline commodity, but because its purity, availability and transportability now intersect with higher‑value, higher‑volume manufacturing. For procurement, the mandate is clear: move beyond unit price optimization to capability procurement — securing suppliers that can guarantee traceable purity, timely qualification and resilient logistics. For corporate development, PF3 presents both a target for bolt‑on acquisitions that shore up supply and a barometer for strategic localization decisions.

The PF3 market’s steady expansion and evolving structure make it a strategic input rather than a routine commodity for many industrial and semiconductor firms. PW Consulting’s study provides the decision‑grade intelligence required to convert market visibility into concrete actions: hedge and localize where necessary, qualify in parallel, and prioritize supplier capability over narrow cost gains. For teams setting strategy in 2026, the question is not whether to engage with PF3 market intelligence — it is how quickly you will operationalize the insights.

To access the full datasets, supplier scorecards and tactical playbooks referenced here, please consult the PW Consulting report landing page. The detailed appendices will enable you to model, negotiate and execute with confidence in a market that is simultaneously growing, consolidating and exposed to policy and commodity risks.

For detailed analysis of this topic, please visit the official page:Phosphorus Trifluoride (PF3) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com