Europe Nuts Market: Insights and Competitive Analysis

Other |

2026-03-02 06:57:30

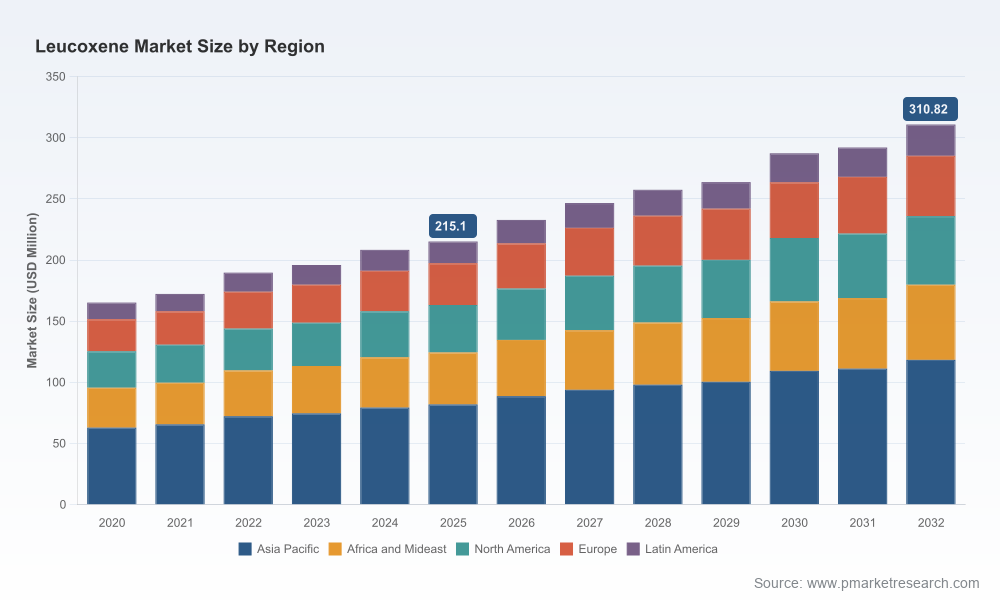

PW Consulting’s latest Leucoxene Market report (base year 2025; historical analysis 2020–2025; forecast 2026–2032) equips executives with the market analytics and transaction-grade tools necessary to convert mineral feedstock dynamics into competitive advantage in 2026. Our model projects a compound annual growth rate (CAGR) of 5.4% across the 2026–2032 forecast window. Measured in USD Million, the global market expands from an estimated 215.1 in 2025 to a projected 232.8 in 2026 and continues to rise toward 310.8 by 2032 — a trajectory that creates discrete opportunities across procurement, processing, and downstream manufacturing value chains.

Leucoxene Market

Time-sensitive sourcing: Leucoxene remains a strategic feedstock for welding flux, pigment production and titanium metal pathways. Secure sourcing and contract structure decisions taken in 2026 will materially affect manufacturing cost curves for the next decade.

Leucoxene Market

Price signaling and hedging: Observable price datapoints (for example, reported ilmenite and leucoxene bulk f.o.b. Australia pricing in 2025) indicate volatility pockets that reward proactive hedging, long-term offtakes and quality-linked pricing clauses.

Leucoxene Market

Regulatory and ESG alignment: Certification and traceability standards—now including industry-recognized frameworks—are reshaping premium access to industrial buyers. Producers with credible IRMA-level performance and documented chain-of-custody capture differentiation in procurement tenders.

Portfolio and capital allocation: Given the market’s steady expansion and concentration dynamics, investors and resource owners must calibrate near-term CAPEX and M&A activity against mid-cycle demand growth and quality differentials.

This report was built as a toolkit for executives and deal teams, not a theoretical literature review. Key deliverables include:

Market sizing and outlook model (2020–2032) in editable format, enabling bespoke scenario runs for price, demand elasticity, and substitution assumptions.

Supply-side inventory and capacity survey — asset cataloguing down to project stage and operational risk classification.

Price and cost sensitivity matrices that map feedstock grades and beneficiation options to downstream margin outcomes for pigment, welding and metal producers.

Commercial playbooks: contracting templates, clause libraries (quality premiums, force majeure language, ESG covenants) and negotiation guides tuned to supplier bargaining power shifts.

Actionable M&A & JV screening frameworks with ranked deal archetypes (bolt-on beneficiation, greenfield near-port, integrated pigment feedstock acquisition).

Sustainability and permitting compendium linking certification status to buyer access and financing conditions.

Our forecast and advisory recommendations rest on three objective signals:

Growth trajectory: The market’s baseline expansion (CAGR 5.4% through 2032) creates persistent demand for higher-quality titanium feedstocks, widening the spread between premium and standard materials in constrained markets.

Concentration dynamics: The top three producers command a majority share of commercially tradable supply, with the top five capturing over seventy percent of market availability. That concentration implies meaningful supplier-side pricing power in supply disruptions and underpins the strategic logic for offtake agreements and vertical integration.

Quality and substitution: Leucoxene’s high TiO2 content profile positions it as a direct competitor to rutile and slag in specific downstream routes. This compositional reality drives differentials in processing economics and capital intensity for downstream users.

Our competitive analysis synthesizes public disclosures, operational footprints and recent company-level moves to produce a short list of firms that matter strategically. Highlights include:

Iwatani Corporation (Japan; https://www.iwatani.co.jp): Through its subsidiary operations, Iwatani is a notable supplier of high-TiO2-grade leucoxene from large primary deposits. Their grade-specific positioning (higher-grade product tiers) creates optionality for premium markets and feedstock-linked value capture.

The Kerala Minerals & Metals Limited (India; https://www.kmml.com): As a state-owned supplier with integrated beach-sand separation capabilities, KMML is a strategic partner for domestic downstream players and a candidate for strategic supply agreements driven by government procurement and local content policies.

Eramet (France; https://www.eramet.com): Grande Côte Operations’ active marketing of high-TiO2 leucoxene (notably positioned for welding flux) and their recent ESG certification achievements indicate a dual commercial-ESG strategy that enhances buyer access in regulated markets.

Iluka Resources (Australia; https://www.iluka.com): As a major mineral sands operator, Iluka’s production variances and quality mix shifts have demonstrable pricing impacts in tradeable feedstock markets — a reminder that mine-level grade curves matter to market participants.

Tronox Holdings Plc (United States; https://www.tronox.com): Integrated pigment producers that also control feedstock can manage margin volatility more nimbly through internal feedstock allocation and process integration.

Astron Limited, Kenmare Resources, Arima Minerals Processing and international traders (e.g., Mineral Global Trading): each plays distinctive roles in project development, regional supply aggregation, processing services and global marketing that buyers should map into sourcing strategies.

Recent observable moves (e.g., active marketing campaigns, quarterly production reviews noting quality impacts, and publicized 2025 price data points) are included in the full report and are used to stress-test near-term scenarios and commercial tactics.

Leaders we advise should treat 2026 as a window for three coordinated initiatives:

Secure feedstock through diversified contracting. Mix long-term offtakes with indexed spot exposure; embed quality-linked premiums and supply-protection language to reduce delivery risk from concentrated suppliers.

Invest selectively in beneficiation and blending capabilities. Where margin math supports, onsite or near-port processing can convert lower-grade inputs into commercially acceptable feedstocks and reduce reliance on constrained premium material markets.

Embed ESG certification into procurement and capital plans. Evidence of certification and documented traceability is increasingly monetizable via access to premium channels and more favorable financing.

Pursue targeted M&A or JVs for upstream optionality. Assets that provide grade diversification or proximity to shipping infrastructure deliver outsized value in scenarios of supply tightness.

Operationalize dynamic pricing and inventory strategies. Use the report’s pricing sensitivity models to calibrate buffer inventories and hedging tactics that minimize margin erosion during price spikes.

Day 0–15: Run the PW Consulting leucoxene model with your internal demand and blend assumptions. Identify top 3 supply-risk scenarios that move your margin most.

Day 16–40: Validate supplier profiles and ESG status in our supplier scorecards. Launch conditional offtake negotiations with prioritized partners and include quality/ESG clauses.

Day 41–60: Execute pilot procurement or blending trials based on model outputs; finalize hedging or inventory policies; brief the board with an M&A/JV shortlist if upstream optionality is warranted.

To preserve the tactical value of our work for subscribers, this public overview intentionally omits granular segment-by-segment volumes, regional share breakdowns and the full pricing curve matrix. These asset-level and subsegment datasets are included in the report’s subscriber deliverables (complete Excel models, interactive dashboards and deal-ready annexes) and are essential for precise contracting, valuation and bid modelling. Our approach follows a “trailer” model: demonstrate methodological rigor and strategic direction while reserving the detailed inputs that catalyze commercial action for report subscribers.

For procurement leaders, finance teams and strategy executives, the 2026 planning cycle is the inflection point to convert macro growth into defensible margin and secure supply. PW Consulting’s Leucoxene Market report provides the calibrated market forecast, competitive intelligence, and operational playbooks required to act decisively. Subscribers gain access to the full dataset, supplier-level scoring, and downloadable scenario models that power negotiations and investment decisions.

Contact PW Consulting or visit our report page to download the executive summary, request a demo of the model, and obtain the subscriber-only annexes necessary for precise 2026 planning.

For detailed analysis of this topic, please visit the official page:Leucoxene Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com