Laser Skin Resurfacing in Dubai | Skin Rejuvenation & Renewal Guide

Health |

2026-05-18 05:15:17

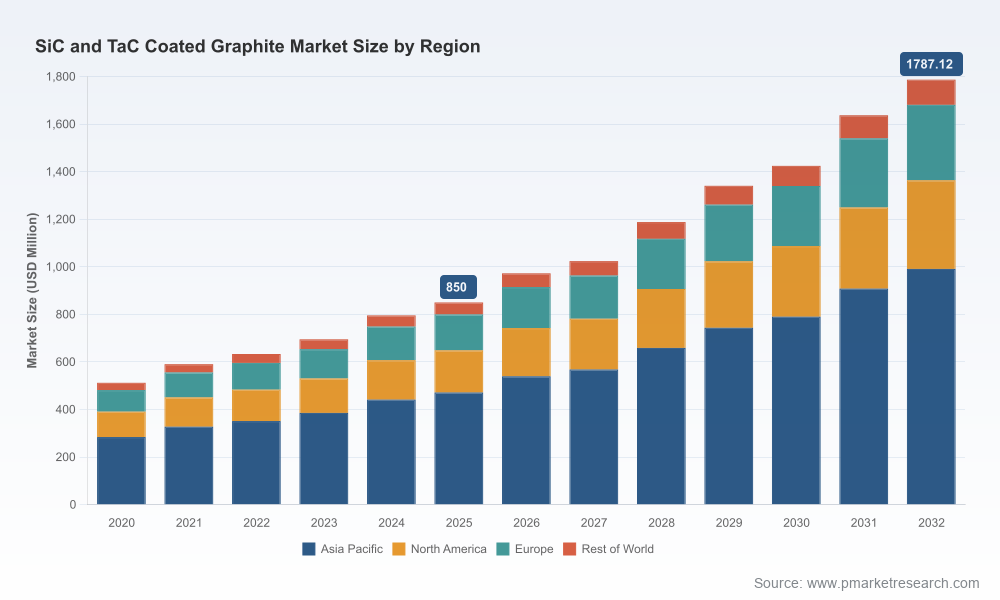

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concise, strategy‑focused briefing drawn from our new market research on silicon carbide (SiC) and tantalum carbide (TaC) coated graphite for semiconductor and advanced wafer processing. The market is at an inflection point: after expanding from roughly USD 512 million in 2020 to about USD 850 million in our 2025 base year, our model points to another step‑change in 2026 with the market moving toward approximately USD 973 million and sustaining an 11.2% CAGR through 2032 to reach a projected USD 1.79 billion. This trajectory carries direct implications for capital allocation, supplier strategy, and risk management plans that must be set in motion in 2026.

SiC and TaC Coated Graphite Market

Timing and scale of capital projects: The expected acceleration in 2026 shifts procurement lead times and qualification cycles from “nice to have” to “mission‑critical” for fabs and equipment OEMs planning EPI, MOCVD, and high‑temperature processing expansions.

SiC and TaC Coated Graphite Market

Supplier and capacity risk: Market concentration is meaningful — the top three and top five suppliers capture a large majority of the market — which raises the stakes for contingency planning, dual sourcing, and long‑term purchase agreements.

SiC and TaC Coated Graphite Market

Cost and margin sensitivity to upstream policy: Tariff dynamics and raw material constraints introduce step changes to landed cost assumptions and unit economics; procurement strategies must be redesigned for scenarios where raw material duties and trade measures persist or expand.

M&A and partnership windows: Consolidation and strategic asset transactions are likely to accelerate; being prepared with a prioritized target list and integration playbook will unlock competitive advantage.

Strong secular demand drivers. Growth is driven by increasing adoption of SiC devices, expansion of advanced logic and power fabs, and rising throughput in epitaxial and MOCVD production. These structural drivers underpin the double‑digit CAGR we forecast across 2026–2032.

Concentrated supply base. The market exhibits a high degree of concentration among a small set of specialized suppliers. This creates pricing power and potential supply bottlenecks during rapid end‑market ramps; CR3 and CR5 metrics in our study highlight this concentrated structure and the attendant strategic implications for buyers and investors.

Tariff and raw‑material policy noise. Two trade measures warrant immediate attention: a 25% tariff on Chinese synthetic graphite has been in place since mid‑2024, and a 25% tariff on natural flake graphite is scheduled to take effect on January 1, 2026. These measures materially alter landed costs and supplier economics and should be incorporated into 2026 budgeting and sourcing scenarios.

Ongoing capacity investments and M&A. Recent industrial moves — from capacity expansions by select coated graphite manufacturers to strategic asset acquisitions in adjacent metal and specialty materials businesses — are reshaping competitive positioning. These transactions are not isolated; they indicate a broader consolidation and capability‑build trend that will affect access, lead times, and pricing dynamics.

Technology and product differentiation. Suppliers compete on coating quality (CVD vs. pyrolytic), coating uniformity, thermal stability (notably TaC’s superior high‑temperature resistance in certain use cases), and contamination control. These technical differentials are often the decisive factors during component qualification and will shape long‑term supplier selection.

Toyo Tanso (Japan): A long‑standing player with proprietary CVD processes and branded offerings for SiC and TaC coatings. Their recent capacity moves and product positioning around high temperature performance make them a go‑to for customers prioritizing thermal endurance and established quality assurance practices.

SGL Carbon (Germany): A European incumbent focused on high‑volume industrial quality and integrated carbon‑material solutions. Their product breadth and established relationships in wafer processing and crystal growth underpin a resilience advantage in key markets.

Schunk Xycarb Technology (Schunk Group): Strong in susceptors and consumables for a wide array of semiconductor processes. Schunk’s system‑level orientation and global service network make them attractive partners for OEMs needing co‑development and rapid deployment support.

Mersen (France): Emphasizes purity and durability across SiC and TaC coated components; effective in serving customers that require certified supply chains and compliance with stringent contamination and materials standards.

China‑based suppliers (several firms): A growing cohort of manufacturers offer competitive cost positions and increasing technical capability in coated graphite parts. Buyers must weigh qualification speed and cost advantage against potential tariff exposure and geopolitical risk.

US and specialist suppliers (e.g., Stanford Advanced Materials, MWI, Bay Carbon): Often serve niche, high‑spec needs with rapid development cycles; strategic for customers needing small‑batch innovation or alternative sourcing lanes.

Market movements to watch: recent asset acquisitions by specialty materials firms and selective capacity expansions are changing supplier economics. Executives should treat these moves as leading indicators of consolidation and rising entry barriers for new entrants.

Robust market sizing and forecast framework (base year 2025; historical 2020–2025; 2026–2032 forecast with scenario testing around an 11.2% CAGR).

Segmentation by region, type (SiC vs TaC), and application with qualitative narratives that explain demand drivers and qualification timelines (note: detailed subsegment tables and modelled dollar splits are available in the full report).

Supply‑chain maps and supplier capability matrices that combine technical attributes, scale, geographic footprint, and trade‑policy exposure to support sourcing decisions.

Cost and TCO modeling templates that incorporate raw material tariffs, logistics, duty scenarios, yield impacts, and lifecycle replacement profiles for capital equipment components.

Commercial playbooks: supplier qualification checklists, contract clauses for tariff pass‑through, inventory and JIT strategies tuned to brittle supply windows.

M&A and partnership screening tools: prioritized target list, scorecards, and value‑capture roadmaps for bolt‑on acquisitions or JV structures.

Primary‑research appendices: executive interviews, plant visits, and validated vendor questionnaires underpinning our qualitative judgments and risk assessments.

Recalibrate procurement assumptions immediately to factor in the January 2026 tariff scenarios and model multiple duty outcomes through 2027; lock in dual sourcing pilots for critical components by Q2 2026.

Prioritize qualification cycles for alternate suppliers that have clean room processes and documented contamination control; accelerate test and validation budgets to compress multi‑quarter timelines.

Deploy capex phasing that aligns equipment orders with supplier capacity ramp signals rather than purely with internal demand forecasts; consider staged purchases to manage inventory risk.

Design contractual protections — price collars, inventory buybacks, and supply continuity clauses — and negotiate longer lead times where economically justified to stabilize production runs.

Prepare M&A playbooks for opportunistic consolidation: build valuation models that stress tariff‑adjusted margins and supplier concentration premiums to prioritize targets.

Invest in a modest in‑house coating and testing capability if strategic volume warrants vertical integration; run a 24‑month business case exercise now to determine break‑even timing.

Procurement leaders: use the TCO templates to reprice supplier panels and adjust inventory strategies under tariff contingencies.

Strategy and corporate development teams: apply the M&A scorecards to identify high‑value targets or partnership candidates and to prepare informed bids amid consolidating markets.

R&D and process engineering: prioritize qualification of TaC vs SiC materials based on process temperature windows, contamination tolerance, and projected throughput growth.

Investors and PE sponsors: leverage concentration metrics and deal‑level scenario analyses to size arbitrage opportunities and to structure earn‑outs that reflect tariff and capacity risk.

Our report is deliberately structured as an operational toolkit for 2026: it synthesizes industry economics, supplier positioning, tariff‑impact scenarios, and actionable playbooks. This briefing has been curated to show the depth of our analysis while preserving the detailed subsegment numbers, regional and application splits, and vendor‑level financial models that are included exclusively in the full report. For complete access to the granular datasets, vendor share tables, downloadable TCO models, and our prioritized action plan, please visit the official report page.

PW Consulting stands ready to support tailored workshops, supplier due diligence, and scenario modeling tailored to your organization’s exposure and strategic priorities for 2026. Contact our practice to schedule a briefing and to obtain the full dataset and tools that underpin these recommendations.

For detailed analysis of this topic, please visit the official page:SiC and TaC Coated Graphite Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com