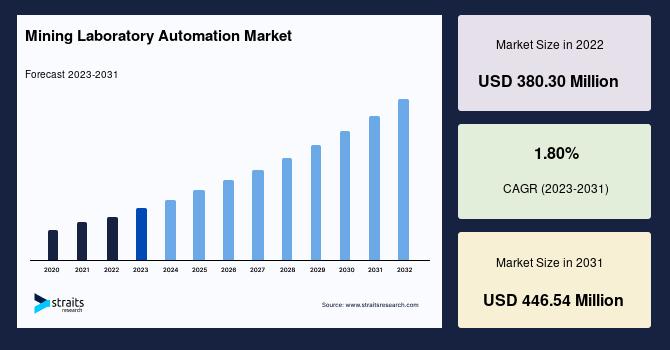

鉱業研究所の自動化市場規模は、鉱物試験の効率と精度によって推進され、446.54によって2031百万米ドルに達する

Home |

2026-04-24 10:29:08

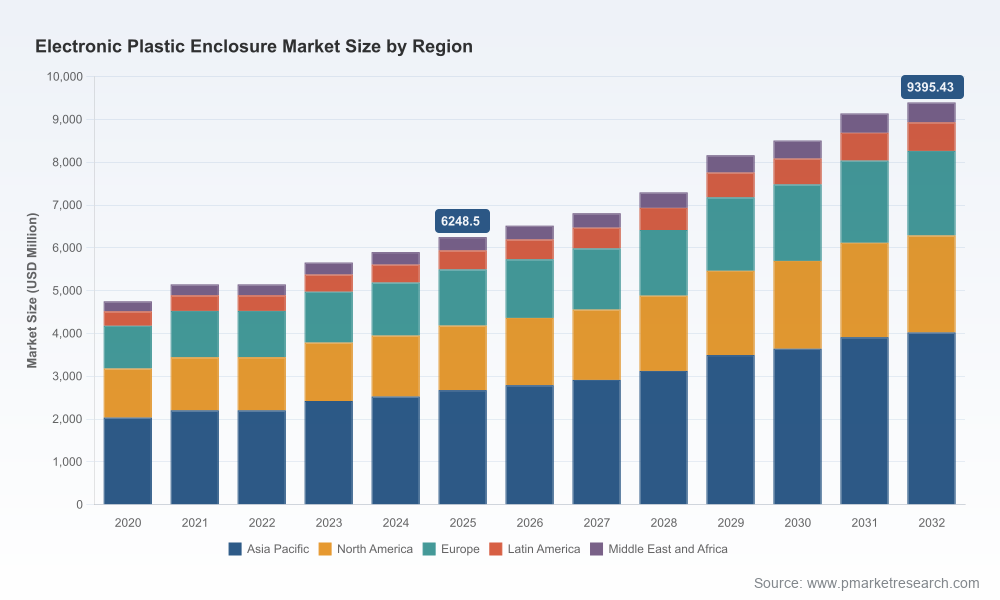

PW Consulting’s latest market study on Electronic Plastic Enclosures positions industry leaders, product strategists, and investors to act decisively in 2026. Built on a rigorous historical dataset (2020–2025) and a detailed forecast horizon (2026–2032), the report quantifies market expansion and maps the practical levers companies must pull to capture value. At the macro level, the global market expanded from a multi-billion-dollar base in 2020 to an estimated USD 6.25 billion (Revenue Unit: Million) in the 2025 base year, and PW Consulting projects growth to roughly USD 9.40 billion by 2032 at a compound annual growth rate (CAGR) of 6.0% over the forecast period. The market concentration is moderate: the top three firms account for less than one-third of industry revenue, while the top five collectively remain below forty percent — a structure that favors nimble incumbents and well-capitalized challengers alike.

Electronic Plastic Enclosure Market

Actionable foresight under uncertainty: We translate macro growth (CAGR and total-market trajectories) into stress-tested scenarios for price, input-cost volatility, and demand shocks that are likely to shape 2026 strategies.

Electronic Plastic Enclosure Market

Prioritization for scarce capital: The study offers a decision matrix to prioritize investments — tooling, automation, product line rationalization, and selective nearshoring — aligned to profit-at-risk analyses across common enclosure use-cases.

Electronic Plastic Enclosure Market

Sustainable compliance and product redesign: With tightening regulatory regimes and eco-criteria in electronics procurement, the report maps compliance pathways (material substitution, reporting, and design constraints) that companies will need to operationalize in 2026.

Competitive and M&A playbooks: Detailed profiles and capability matrices for leading manufacturers enable acquirers and partners to assess inorganic and alliance opportunities informed by capability gaps and regional footprint priorities.

Market architecture and demand drivers: A concise synthesis of end-market pull (consumer/industrial/automotive/telecom/medical trends) and supply-side structures (manufacturing modalities, contract vs. captive production).

Scenario-based financial models: Revenue and margin sensitivity analyses that convert macro forecasts into P&L and cash-flow impacts under multiple material-cost and tariff-loading scenarios.

Supply-chain stress tests and sourcing playbooks: Multi-factor risk maps and recommended sourcing strategies (dual-sourcing, regional supply nodes, inventory hedging) tailored to enclosure producers and OEM buyers.

Product and manufacturing playbooks: Comparative analysis of injection molding, thermoforming, and tool-less custom solutions, with guidance on volume thresholds, capex timing, and lead-time optimization.

Regulatory and sustainability compliance templates: Practical checklists for meeting regional reporting obligations and low-chemical-content criteria, plus lifecycle improvement levers to support procurement targets.

Commercial playbooks: Pricing strategies, channel optimization, and aftermarket services (customization, assembly, and integrated sensor housings) that drive differentiation in a fragmented market.

Competitive benchmarking deck: Profiles and strategic positioning for the most-active vendors — including their product focus, manufacturing strengths, and recent moves — enabling fast comparative diagnostics.

Data appendices: Granular segment-level forecasts, price/volume matrices, and supplier scorecards (note: segment-level figures are purposefully reserved in this public summary — full datasets are available in the complete report).

The industry comprises a mix of long-standing component houses, regional specialists, and vertically integrated contract manufacturers. The market’s moderate fragmentation (CR3 ~28.5%, CR5 ~39.8%) means scale matters but does not wholly determine competitive outcomes. Success increasingly hinges on capability breadth (materials, ratings, customization), supply resilience, and regulatory/quality credentials.

Polycase (Avon, Ohio) — Known for U.S.-manufactured enclosures with NEMA-rated outdoor solutions and strong off-the-shelf and customization capabilities. Recent product activity includes expansion of NEMA-rated series and incremental size additions, signaling continued investment in ruggedized platforms that reduce OEM integration work.

Bud Industries (Willoughby, Ohio) — Broad catalog strength in industrial enclosures; recent introductions emphasize higher ingress-protection designs and modularity for factory and commercial applications.

Hammond Manufacturing (Guelph, Ontario) — Differentiates via EMI/RFI shielding options and a portfolio spanning miniature to general-purpose enclosures, appealing to designers requiring electromagnetic robustness.

OKW Enclosures (Germany/US presence) — Competes on industrial design and ergonomic enclosures for handheld and panel-mounted electronics; recent announcements focus on solutions for extreme factory environments.

New Age Enclosures & Productive Plastics — Represent contrasting specialization: New Age on high-volume injection molded PCB enclosures and short-run customization; Productive Plastics on larger thermoformed enclosures for robotics and sensors, serving OEMs with moderate-volume needs.

Regional specialists (Fibox, Bopla, Rolec, Allied Moulded, Integra, Toolless) — These firms leverage localized distribution, material specialization, and niche product portfolios (e.g., polycarbonate/IP-rated boxes, metal-plastic hybrids, tool-less custom assemblies) to protect margins and retain customer stickiness.

Product refresh and premiumization: Multiple vendors are launching NEMA/IP-rated and ergonomically optimized models — a signal that OEMs are willing to pay for pre-certified solutions that lower their time-to-market and compliance burden.

Material cost and substitution dynamics: Raw-material volatility is a near-term operational reality. For example, ABS resin experienced upward price pressure in early 2026 linked to feedstock and plant turnarounds, while polycarbonate saw notable price softening through late 2025. These divergent price signals create both margin risk and substitution opportunities; our models quantify breakeven points for replacing ABS with lower-cost or higher-performance alternatives across common form factors.

Regulatory pressure is rising: New reporting obligations and chemical-content limits (notably restrictions on specific flame retardants and halogen levels in plastic parts) require manufacturers and OEMs to adapt material specifications, supplier audits, and disclosure practices. Non-compliant portfolios will face both procurement exclusion and potential retrofit costs.

Geopolitical trade constraints: Tariff modifications and trade policy shifts (including recent Section 301 changes affecting strategic goods) continue to influence sourcing decisions, pushing some buyers toward nearshore suppliers or restructured supply chains to mitigate incremental tariff exposure and lead-time uncertainty.

Adopt a materials-first product roadmap: Prioritize qualification of alternative resins and validated suppliers to reduce single-material exposure and secure compliance with tightening chemical-content limits.

Target differentiated “certified” product tiers: Invest selectively in NEMA/IP and EMI/RFI-certified SKUs that command premium pricing and shorten OEM integration timelines.

De-risk supply chains incrementally: Implement dual-sourcing policies for critical resins and tool-critical components, and evaluate nearshoring for high-value or rapid-replenishment SKUs.

Commercialize services around customization: Expand value-add services (assembly, labeling, integrated gaskets and connectors) to increase wallet share and create switching costs for customers.

Use M&A to acquire capabilities, not only scale: Target acquisitions that add unique manufacturing processes (e.g., thermoforming for large housings, tool-less prototyping) or compliance credentials rather than purely revenue accretion.

This study goes beyond headline growth figures to provide executable templates: negotiation playbooks for resin procurement, ROI calculators for tooling vs. outsourcing, and supplier scorecards that map technical capability to commercial terms. The report’s scenario models translate the global CAGR and market trajectory into concrete budgetary impacts for product lines and regional operations.

We intentionally omit full segment-level tables and proprietary regional splits in this summary to preserve the strategic value of the dataset for subscribers and clients. The complete report contains exhaustive segmentations, price/volume matrices, and supplier-level forecasts that are essential for transaction diligence, capex allocation, and product roadmapping.

Purchase the full PW Consulting Electronic Plastic Enclosure Market report to access the granular datasets, segmentation breakouts, and downloadable modeling tools that support board-level decisions in 2026.

Schedule an executive briefing for a customized walk-through of scenarios pertinent to your portfolio, including bespoke sensitivity modeling and M&A target mapping.

For executives planning budgets, sourcing strategies, or M&A activity in 2026, PW Consulting’s report turns aggregate market momentum — a mid-single-digit CAGR and near-term growth to nearly USD 9.4 billion by 2032 — into operationally relevant intelligence. Contact PW Consulting to convert these insights into an actionable 12–24 month plan tailored to your organization’s risk profile and growth ambition.

For detailed analysis of this topic, please visit the official page:Electronic Plastic Enclosure Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com