Photosensitive Polyimide for Semiconductor Market — Strategic Preview for 2026 Decision-Makers

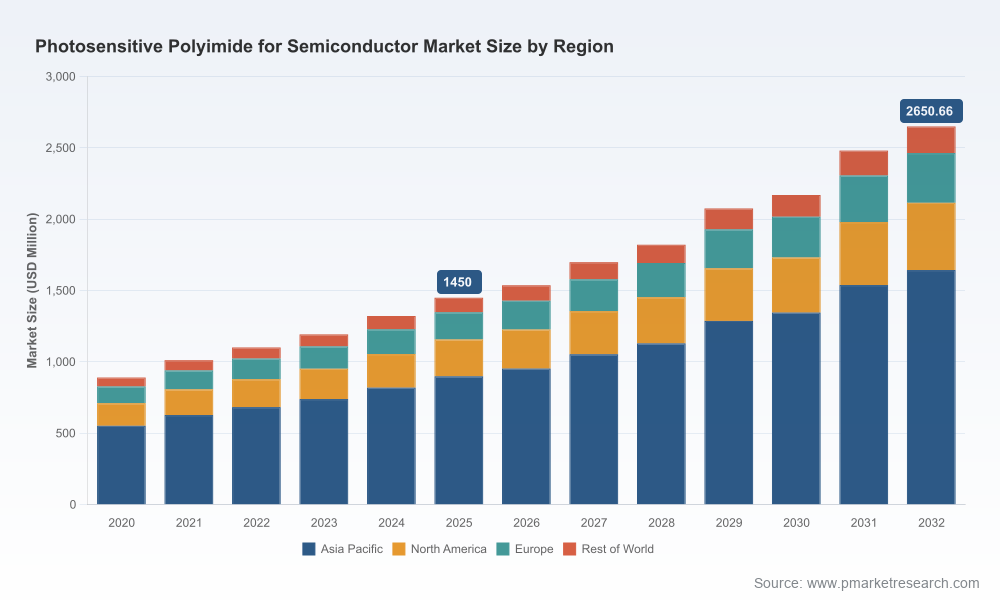

PW Consulting’s latest market study on Photosensitive Polyimide (PSPI) for the semiconductor industry arrives at a pivotal moment. The global PSPI market reached approximately USD 1.45 billion in our base year (2025) and is forecast to expand at a compound annual growth rate (CAGR) of 9.0% through the 2026–2032 forecast period, reaching roughly USD 2.65 billion by 2032. These macro dynamics — faster-than-average growth, a high degree of supplier concentration, and accelerating regulatory and materials-driven shifts — make PSPI a strategic lever for semiconductor packaging, MEMS, and AI-driven device roadmaps in 2026.

Photosensitive Polyimide For Semiconductor Market

Why this report matters to executives in 2026

For procurement, product, and corporate strategy teams, the PSPI report is not an academic exercise: it is a practical decision support tool built to inform near-term capex, sourcing, and qualification choices. The market’s steady growth and the scale concentration among a few suppliers create both opportunity and risk — and they require tailored responses depending on your exposure to advanced packaging, wafer-level redistribution, or high-reliability passivation needs.

Photosensitive Polyimide For Semiconductor Market

- Capex prioritization: Our forecast and scenario workbench helps firms decide whether to fast-track substrate or packaging investments now or adopt a “wait-and-assess” posture until supply-side upgrades filter through in 2027–2028.

- Supplier sourcing and qualification: Given a concentrated supplier base, the report outlines supplier risk matrices and suggested multi-sourcing strategies to protect continuity while accelerating qualification cycles for PFAS- and NMP-free chemistries.

- Product roadmap alignment: Materials choices (e.g., negative- vs positive-tone PSPI, film vs liquid forms) have downstream cost, yield, and reliability impacts. The study offers a decision framework to match chemistry and form factor to packaging architecture and test strategy.

- Regulatory and sustainability compliance: The market is shifting toward low-VOC, PFAS-free, and NMP-free solutions. The report’s compliance checklist helps procurement teams de-risk product portfolios for EU REACH/RoHS and evolving regional chemical regulations.

What the report delivers — practical, executable content

We designed the research for immediate operational use. The report synthesizes quantitative market modeling with tactical playbooks and supplier-level intelligence so that users can move from insight to execution within a 90–120 day horizon.

Photosensitive Polyimide For Semiconductor Market

- Market model & interactive forecasts: A transparent demand-supply model covering 2020–2025 historicals and a 2026–2032 baseline plus alternative scenarios. The model is delivered with guidance on sensitivity levers (end-market growth, packaging technology adoption rates, and raw material price volatility).

- Executive playbook: 12 tactical recommendations for procurement, R&D, and product line managers — including supplier engagement templates, pilot qualification roadmaps, and accelerated approval checklists for PFAS/NMP-free materials.

- Supplier scorecards and capability maps: Operational and technology assessments for the leading PSPI vendors. Each scorecard covers manufacturing footprint, product breadth (liquid vs. film; positive vs. negative tone), regulatory posture, and near-term capacity initiatives.

- Risk heat maps & scenario planning: Supply disruption scenarios, pricing shock simulations, and their quantified P&L or time-to-market impacts under three plausible 2026–2028 pathways.

- IP and partnership landscape: Identification of strategic R&D partners and substrate manufacturers for co-development initiatives, and negotiation points for shared sample programs.

- Implementation tools: A calibration checklist for qualification labs, recommended test matrices for thermal/chemical/UV resilience, and a sample project timeline to compress vendor qualification into an expedited cadence.

Competitive dynamics — synthesis and strategic implications

The PSPI supplier base exhibits significant concentration. Our analysis shows the top three companies account for over 70% of the market with the top five approaching near-total market share. That structure creates powerful incumbency advantages but also makes capacity additions and product innovations meaningful inflection points for the market.

- Toray Industries, Inc. (Tokyo). Toray’s recent moves — including mass production starts and high-aspect-ratio material introductions — position it as a technology leader in high-thickness, high-aspect-ratio patterning. Their STF series (notably formulations engineered to avoid NMP and PFAS in latest variants) is strategically relevant to MEMS, advanced packaging RDL, and applications requiring thick, void-free resin fills. For customers targeting aggressive RDL geometries or simultaneous TGV/RDL process flows, Toray is a primary engagement target.

- Asahi Kasei Corporation (Tokyo). Asahi Kasei’s investments to expand production capacity underscore strong demand dynamics in advanced packaging. Their PIMEL™ line is positioned across buffer, passivation, and RDL applications, and the announced plant expansions indicate they intend to be a supply anchor for high-volume manufacturers.

- FUJIFILM Corporation (Tokyo). FUJIFILM’s ZEMATES™ brand and global supply footprint reflect a strategic bet on diversified form factors (liquid and film) and PFAS-free chemistry. Their ambition to scale sales significantly implies aggressive go-to-market activity and potential channel effects for panel- and panel-level packaging developments.

- HD MicroSystems / DuPont (US-Japan JV and DuPont’s channels). HD MicroSystems’ product range — including NMP-free formulations and low-temp curable options — offers attractive compliance and process-integration benefits. DuPont’s broader footprint and historical capacity expansions make them a pivotal partner for flexible electronics and certain microelectronics segments.

- Kolon, Kaneka, Nissan Chemical. Regional and specialty players retain important roles: Kolon for thermal stability and patterning in advanced packaging; Kaneka and Nissan Chemical for high-reliability and application-specific formulations. For specialized needs or dual-sourcing strategies, these firms are credible second-source partners.

Regulatory and raw-material headwinds — how they change supplier selection

Three industry forces are simultaneously reshaping the PSPI landscape:

- Regulatory convergence: REACH/ROHS and national chemical controls are accelerating migration to PFAS-free and NMP-free formulations. Vendors already offering compliant chemistries reduce adoption friction for global OEMs and substrate suppliers.

- Material-price volatility: Polyimide pricing experienced notable swings in 2025, with APAC pricing softening in parts of the year and periodic restocking-driven pressure in North America. These dynamics make locked-price and volume-flex contracts a core risk-management tool in 2026 procurement negotiations.

- Concentrated capacity risk: New plant starts and announced investments will shift supply balances, but the timing mismatch between investment announcements and actual production ramp-ups means strategic buyers must plan for phased qualification and buffer inventory during 2026–2028.

How to act in 2026 — a 90-day tactical roadmap

PW Consulting recommends a focused set of actions for organizations that cannot afford supply interruptions or that need to capture yield improvements tied to PSPI selection:

- 0–30 days: Run an exposure and dependency audit: map products and packaging flows that use photosensitive polyimide and catalog current vendor qualifications and lead times. Prioritize items by revenue and technical sensitivity.

- 30–60 days: Initiate multi-supplier sample programs with at least one incumbent and one emerging alternative offering PFAS/NMP-free chemistries. Use the report’s qualification checklist to shorten iteration cycles.

- 60–90 days: Negotiate conditional capacity agreements and price-protection clauses with strategic suppliers; lock pilot volumes with clear acceptance criteria and milestone-based expansion options tied to our scenario triggers.

Why PW Consulting’s report is uniquely actionable

We combine a transparent top-down market model (2020–2025 historicals; 2026–2032 forecasts), supplier-level operational analysis, and implementation-level playbooks validated by industry practitioners. The work is intentionally practical: not just “what is happening” but “what you need to do next,” with ready-to-use templates for qualification, contracting, and pilot execution.

Because this release follows the “trailer” principle, we have purposely withheld granular segment-by-segment tables and the supplier scorecard spreadsheets that underpin our recommendations. The full report contains those assets — including downloadable data tables, regional supply-demand curves, and detailed vendor benchmarking — which are essential for precise capex and sourcing decisions.

Next steps

For procurement leaders, process engineers, and strategy teams planning 2026 capex or sourcing moves, PW Consulting’s full report provides the calibrated inputs and templates needed to convert market insight into defensible decisions. Access to the complete dataset and supplier scorecards will enable tailoring of the report’s playbook to your product mix and geographic exposure.

Contact PW Consulting to obtain the full report and the downloadable model so your 2026 strategy is driven by a defensible forecast, supplier intelligence, and executable risk-mitigation plans.

For detailed analysis of this topic, please visit the official page:Photosensitive Polyimide For Semiconductor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com