Long Skirt With Full Sleeve Tie Top – Elevate Your Style with Trendy-Atelier

Shopping |

2026-06-26 03:32:38

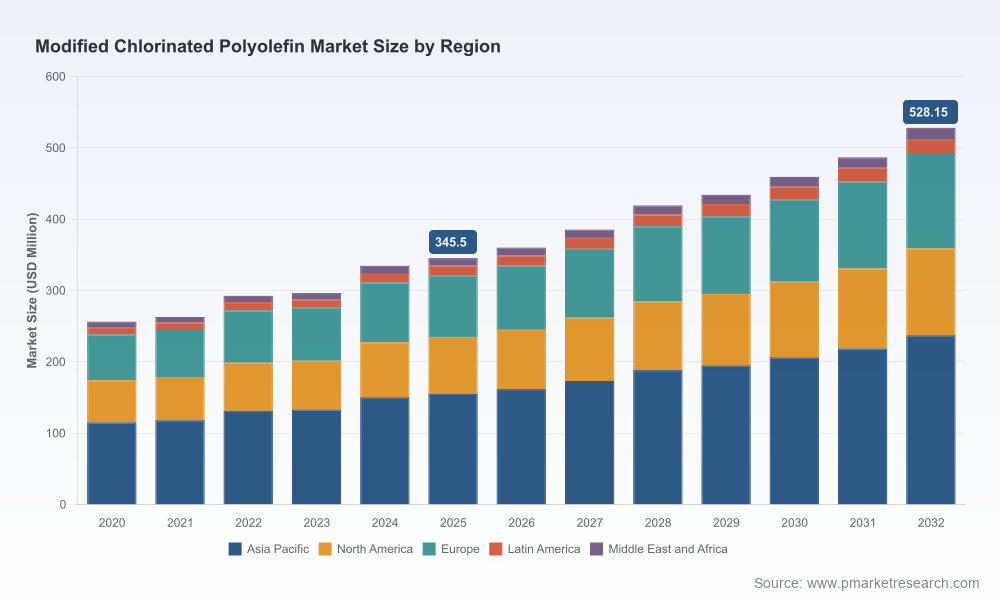

PW Consulting’s latest market study on Modified Chlorinated Polyolefin (MCPO) provides an operationally focused intelligence package designed to inform boardroom and functional decisions in 2026. Our model shows the market reached USD 345.5 Million in 2025 and, under our central case, will grow at a compound annual growth rate (CAGR) of 6.28% through 2032 to approximately USD 528.15 Million. That trajectory combines steady demand from legacy uses (coatings, inks, adhesives) with accelerating adoption of waterborne and low‑VOC formulations driven by regulatory and OEM pressures.

Modified Chlorinated Polyolefin Market

Regulatory inflection: New emissions and materials regulations that crystallize in 2025–2026 will materially change formulation economics and go‑to‑market mechanics for adhesion promoter systems.

Modified Chlorinated Polyolefin Market

Raw material volatility: Feedstock cost swings—polyolefins and chlorine derivatives—are creating margin compression windows that reward procurement sophistication and flexible production footprints.

Modified Chlorinated Polyolefin Market

Technology transition: A measurable shift toward waterborne dispersions and specialty modified grades is opening routes for product premiumization and differentiation—if executed with credible supply assurance and application support.

Proprietary market model and scenario engine: a calibrated supply‑demand model that can be re‑run with custom input assumptions (pricing, raw material shocks, adoption curves) so commercial teams can stress‑test business plans for 2026–2032.

Commercial playbooks: step‑by‑step guides for launching waterborne MCPO products, including formulation positioning, OEM/coat house engagement scripts, and distributor incentive structures.

Procurement & cost sensitivity tools: hedging and contract design templates keyed to polyolefin/chlorine price drivers, plus margin impact matrices by product family.

Supply‑chain mapping and resilience diagnostics: supplier tiering, single‑sourcing risk heatmaps and contingency planning checklists for manufacturers and converters.

Competitive intelligence dossiers: qualitative and comparative profiles of market leaders, challenger plays, and regional specialists, including product portfolios, channel strategies and capability gaps.

Regulatory and sustainability playbook: compliance checklists, substitution risk scoring, and a path to low‑VOC/waterborne certification for automotive and industrial applications.

M&A and partnership framework: a scoring methodology for identifying bolt‑on targets, JV candidates and distribution partnerships that accelerate access to target end‑markets.

Upstream feedstock volatility is now a strategic factor. Production of MCPO depends on polypropylene, polyethylene and chlorine derivatives. Price swings in crude and derivatives translate quickly into manufacturing cost fluctuations. For 2026 planning, companies must shift from ad‑hoc pass‑through to dynamic cost‑sharing and formula‑based contracts with key customers.

Regulatory pressure is accelerating the migration to waterborne and reduced‑VOC systems. This is reshaping product R&D roadmaps and capital allocation: manufacturers that already offer water‑reducible dispersions or low‑VOC grades are positioned to capture premium demand, while legacy solvent‑based portfolios risk market share erosion unless reformulated.

End‑market nuance matters. Automotive and industrial coatings remain high‑value anchors, but growth pockets are appearing in inks and adhesives where improved adhesion on untreated polyolefins reduces downstream process costs. Commercial teams should prioritize application engineering and co‑development pilots that demonstrate system‑level benefits, not just polymer chemistry.

Concentration and competitive dynamics. Our concentration metrics indicate a market exhibiting moderate consolidation: the top three producers account for a meaningful share of supply, and the top five an even larger portion. That structure creates both barriers and windows—regional specialists can exploit service and speed, while larger players can leverage scale to invest in waterborne technology and regulatory compliance.

Eastman Chemical Company: Eastman’s portfolio of solvent and water‑reducible CPO dispersions (e.g., CP series, Advantis™) positions it as a full‑system supplier for OEMs and coat houses seeking low‑VOC adhesion promoters. Strategy implication: Eastman will continue to invest in application support and regulatory compliance capabilities, raising the bar for new entrants on go‑to‑market execution.

Nippon Paper Group (SUPERCHLON®): With an established acid‑modified CPO brand that integrates well with acrylic/urethane chemistries, Nippon Paper is a go‑to partner for formulators targeting automotive primers and industrial coatings. Strategy implication: their depth in specialty grades signals potential for co‑development deals with regional formulators.

NAGASE America (Hardlen CPO distribution): As a distributor/connector, NAGASE provides flexible packaging and delivery formats across solvent and water‑based grades. Strategy implication: distributors like NAGASE are vital partners for scale rollouts, but margins and loyalty will depend on value‑added services (technical support, inventory programmes).

PhibroChem (partnering with Nippon Paper): Longstanding distribution partnerships offer fast market access in North America. Strategy implication: manufacturers seeking accelerated access should evaluate exclusive vs. non‑exclusive distribution frameworks with performance KPIs.

Toyobo (HARDLEN®): Toyobo’s MAH‑modified CPOs address adhesion challenges on polyolefin substrates. Strategy implication: differentiated chemistries like MAH‑modification allow premium positioning in segments where bond strength and durability are decisive.

iSuoChem and regional Chinese suppliers: Competitive on cost and lead time for local markets, these suppliers compete aggressively on commodity grades and fast delivery. Strategy implication: multinational buyers should weigh total landed cost and quality assurance when sourcing from regional manufacturers.

Align R&D investment to regulation: Prioritise waterborne and low‑VOC formulations where OEM adoption timelines and local standards make compliance a source of commercial advantage.

Reconfigure procurement: Implement index‑linked supply contracts and strategic feedstock hedges for polyolefins and chlorine derivatives; build dual‑sourcing where feasible to reduce single‑supplier exposure.

Prioritise go‑to‑market pilots: Fund application labs and co‑development projects with high‑value customers (automotive tier suppliers, large coat houses) to demonstrate switching economics and secure early wins.

Screen M&A opportunistically: Use our M&A framework to identify targets that fill capability gaps—application engineering, waterborne tech, or regional manufacturing footprints—rather than only volume increases.

Operational readiness: Develop a regulatory compliance roadmap and material substitution plan to pre‑empt material bans or VOC ceilings, and integrate these into new product introductions.

Commercial playbook deployment: Equip sales teams with margin impact calculators and objection handling material focused on lifecycle benefits (adhesion reliability, reduced rework), not just product chemistry.

Granular, segment‑level forecasts, including scenario permutations for regulatory tightening, raw material shocks and accelerated waterborne adoption (available in the full report).

Detailed supplier scorecards and negotiation playbooks tailored to each major purchasing archetype.

Templates and models (Excel) that allow finance, procurement and commercial leaders to rerun forecasts against bespoke assumptions.

The Modified Chlorinated Polyolefin market is at a strategic inflection: steady baseline growth is being reshaped by regulatory drivers and feedstock volatility, creating both risk and opportunity. For 2026, executives must act on three fronts—product transformation (to waterborne/low‑VOC), procurement sophistication, and customer‑centric application support—to protect margins and capture premium segments. PW Consulting’s report delivers the granular tools and decision frameworks needed to translate market direction into executable plans; the executive summary you’ve just read previews the analysis, and the full report provides the segment‑level intelligence and tactical playbooks required for immediate implementation.

To access the full dataset, supplier dossiers, and executable templates referenced here, visit our report page or contact PW Consulting for a briefings package tailored to your strategic priorities.

For detailed analysis of this topic, please visit the official page:Modified Chlorinated Polyolefin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com