Plastic Industry Market Analysis Focusing on Applications and End Users

Other |

2026-02-24 09:52:14

As demand for mitochondria-targeted nutraceuticals accelerates, food grade Urolithin A has shifted from niche scientific curiosity to a commercially material ingredient. Our new market study — covering historical performance (2020–2025) and a forward-looking forecast window (2026–2032) — quantifies that transition and translates it into decision-grade guidance for C-suite leaders, product strategists, R&D heads, and supply-chain executives preparing for 2026 and beyond.

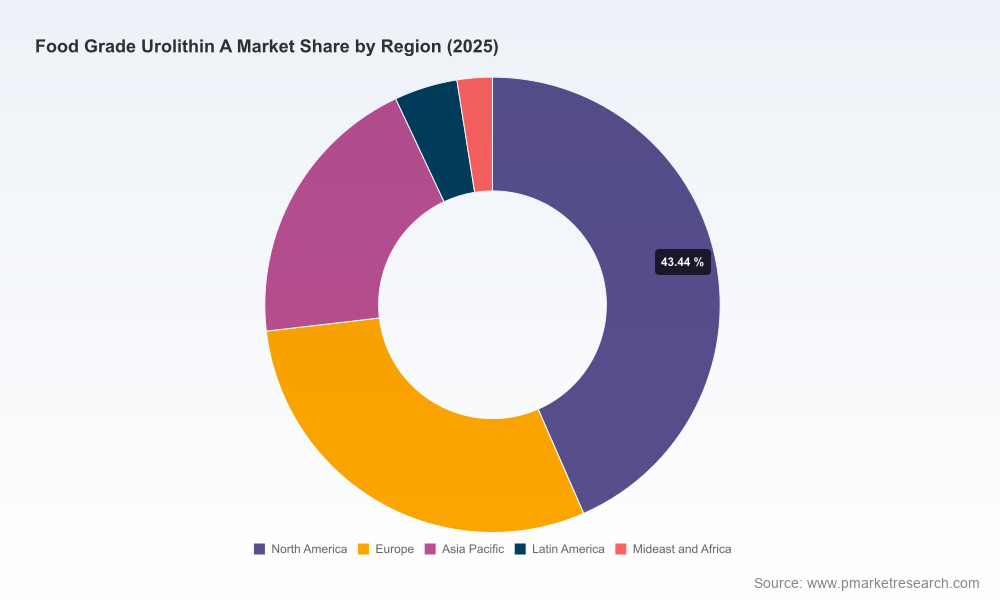

Food Grade Urolithin A Market

PW Consulting’s analysis shows a trajectory that validates strategic prioritization: the global food grade Urolithin A market grew from approximately USD 105 million in 2020 to roughly USD 245 million in 2025, and our forecast projects continued expansion — reaching well into the high hundreds of millions by 2032. The forecast period is underpinned by a compound annual growth rate (CAGR) of 17.5% (2026–2032). This growth is not linear; it is driven by a cluster of converging enablers — improved clinical evidence, regulatory clarity in major markets, and diversified manufacturing routes — and moderated by supply-chain complexity and standardization gaps.

Food Grade Urolithin A Market

The market shows a concentrated supplier base at the top, with the largest incumbents holding a substantial share of commercialized, food-grade Urolithin A. This concentration creates both friction and clarity: partnerships with established suppliers can accelerate time-to-shelf, but they limit negotiating leverage as demand surges.

Food Grade Urolithin A Market

Regulatory precedent plays a catalytic role in 2026 planning. The U.S. FDA’s GRAS notice for Urolithin A — originally notified for certain food formats and usage levels — has been a formative reference point for product developers and regulators worldwide. On the science side, the body of human clinical research has moved beyond single-trial demonstrations to a multi-trial program for certain proprietary ingredients; this shifts commercial value toward those able to substantiate clear, differentiated claims.

At the raw-material level, the ingredient’s origin story matters: Urolithin A is a gut microbiota-derived metabolite of ellagitannins and ellagic acid found in select fruits and nuts. Commercial production today uses a mix of synthetic chemistry and microbial fermentation from natural precursors — choices that influence cost, purity, sustainability narratives, and regulatory positioning.

Our report is designed for rapid application by commercial and technical teams. Highlights include:

A concentrated top tier means that preferred-supplier relationships will determine who can execute premium launches in 2026. PW Consulting’s analysis finds that a small group of clinically-invested and certified suppliers captures a large portion of active market demand, while a larger base of manufacturers competes on volume and price. For commercial teams, the decision framework is simple but consequential:

Our report walks through pragmatic use-case scenarios — from direct-to-consumer supplement launches to large-scale co-manufactured beverages and functional-food integrations — mapping the commercial levers most likely to move P&L in 2026. We quantify the sensitivity of margin to key inputs (supplier premium, dosage strategy, channel mix, and clinical investment) so leaders can prioritize capital allocation with confidence.

Decisions taken in 2026 will determine who captures the most valuable customer segments as the Urolithin A market scales. Our study is intentionally designed as a decision tool — not just a descriptive market narrative. By merging a forward-looking, data-driven forecast (17.5% CAGR over the forecast window) with supplier intelligence, regulatory pathway mapping, and commercial playbooks, the report reduces execution risk and accelerates time-to-value for teams that need to move from strategy to launch within the next 12–24 months.

This preview intentionally highlights the strategic contours and practical implications of the food grade Urolithin A market without disclosing proprietary segment-level figures or supplier-by-segment share data, which are central to the full analysis. For executives and investment teams preparing 2026 budgets, the full PW Consulting report provides the granular models, supplier dossiers, and scenario simulations required to operationalize the plans outlined here.

Contact PW Consulting or visit our full report page to access the complete dataset, supplier matrix, and tailored advisory packages that translate these insights into executable plans for 2026.

For detailed analysis of this topic, please visit the official page:Food Grade Urolithin A Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com