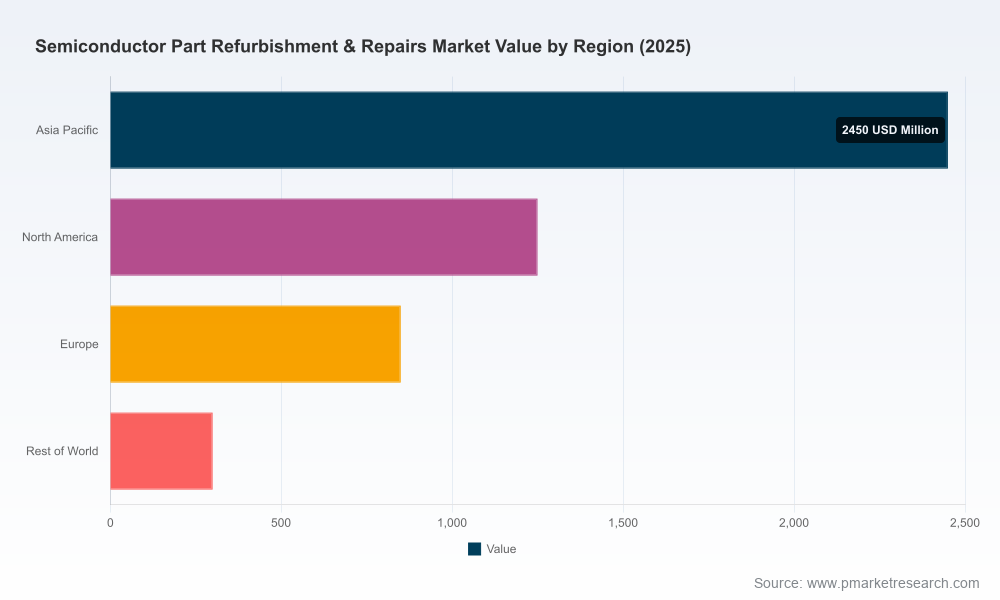

Semiconductor Part Refurbishment & Repairs Market — Strategic Preview for 2026 Decision-Makers

PW Consulting’s new market study on Semiconductor Part Refurbishment & Repairs provides a concise, decision-grade intelligence package tailored for executives crystallizing their 2026 strategies. The market we modelled has recorded consistent expansion through the mid-2020s and—on our base-year 2025 view—stands at a materially larger aftermarket opportunity than in prior years. Our forecast shows continuing growth to 2032 at a compound annual growth rate of 7.85%, reflecting a combination of sustained fab investment, elevated chip pricing dynamics, and supply-chain stress that amplify demand for repair, refurbishment and parts-replacement pathways.

Semiconductor Part Refurbishment Repairs Market

Why this report matters for 2026

- Rapidly shifting economics: With recovery and expansion waves in global semiconductor manufacturing, executives are facing a near-term choice between heavy new-capex commitments and optimized aftermarket strategies. This report quantifies how refurbishment and repair can be used to defer capex, protect yield, and extract lifetime margin from installed assets.

- Material policy and trade inflection points: New trade measures and tariff regimes effective in early 2026 alter the calculus for cross-border maintenance and parts sourcing. Critically, several exemptions explicitly preserve repair, replacement and R&D activities—an operational window many firms can exploit. Our analysis maps practical implications for supply chain design.

- Operational urgency driven by lead times and pricing: Persistent lead-time extensions and supplier price moves in 2026 elevate the strategic value of refurbishment solutions. We show how repair and remanufacturing mitigate production disruptions caused by multi-quarter procurement cycles and intermittent component price shocks.

- Commercial upside in aftermarket services: OEMs, independents and distributors can monetize warranties, extended-service agreements and exchange programs. The report provides frameworks to convert technical capabilities into recurring revenue streams while managing warranty and performance risk.

What we analysed — scope and macro takeaways

The study synthesizes a quantitative market model (historical 2020–2025, base year 2025) and a bottom-up forecast window for 2026–2032. On the market-size front, the aftermarket reached notable scale by 2025, with continued upward trajectory into 2026 and beyond under the 7.85% CAGR scenario. Our forecast horizon captures substitution patterns between new-equipment spend and refurbishment-driven life-extension, and stress-tests outcomes under different geopolitical, pricing and fab-spending scenarios.

Semiconductor Part Refurbishment Repairs Market

Primary research included structured interviews with operators, repair specialists, OEM service heads and procurement managers, supplemented by secondary data and transaction screening. We cross-validated repair-cycle assumptions with empirical field-service logs and warranty claims to produce actionable estimates of market depth and service throughput.

Semiconductor Part Refurbishment Repairs Market

Practical contents you can use immediately

- Executive playbooks: Procurement and service playbooks tailored to OEMs, fabs, and independent service providers—detailing decision trees for when to repair vs replace, and contract clauses that secure cross-border service continuity given evolving export controls.

- Operational toolkits: Templates for refurb ROI calculation, TCO (total cost of ownership) comparators, and repair-benchmark KPIs (mean time to restore, first-time-fix rate, refurbishment lifecycle multipliers).

- Regulatory & compliance guide: A short checklist and flowchart covering tariff implications and U.S. licensing considerations—particularly relevant where repair exemptions interact with Section 232-style measures and BIS licensing regimes.

- Supplier evaluation matrix: A scoring model to evaluate partners on technical capability, vintage-equipment expertise, throughput capacity, warranty posture, and traceability—designed to accelerate vendor selection without bespoke audits.

- M&A and partnership playbook: Due-diligence checklists and value-creation levers for consolidators evaluating tuck-ins or technology acquisitions in the repair and refurbishment ecosystem.

Competitive landscape — who matters and why

The aftermarket remains a mix of specialized independents, regional service houses, and refurbished-equipment resellers. Market concentration is moderate—our CR3/CR5 metrics indicate meaningful scale among top providers, but ample room for regional specialists and niche capability providers to capture profitable pockets.

- IES Semiconductor Parts (Bristol, UK): Focused on repair & testing of a broad set of manufacturing parts—power systems, motors and high-voltage assemblies—with an emphasis on extending legacy and obsolete equipment lifecycles under warranty programs. IES is well-positioned where legacy-line continuity is a priority.

- PSI Semicon Services (Livonia, MI, USA): Offers comprehensive repair, refurbishment and remanufacturing across robotics, PCBs, controllers and vacuum systems—notable for deep legacy-technology support and integration services that appeal to mature fabs.

- SemiGroup (Dallas, TX, USA): Operates a scale refurbishment & resale model that refurbishes to original-equipment specifications and provides installation and maintenance support—optimizing supply for cost-sensitive fabs and non-critical toollines.

- Capitol Area Technology (Austin, TX, USA): Distributor and repair provider for new, used and refurbished spare parts; strong channel reach and parts distribution capability.

- Ichor Systems (Fremont, CA, USA): Known for specialized single-chamber plasma etch refurbishments and design engineering that enable field retrofits—valuable for customers seeking performance upgrades during refurbishment.

- Semiconductor Support Services Co. (Austin, TX, USA): Delivers repairs, upgrades and parts for major OEM tool families—useful for fabs wanting one-stop support across AMAT, Lam and TEL assets.

- Conation Technologies (USA): Niche focus on KLA-Tencor equipment aftermarket parts and services—an example of high-margin specialization where domain knowledge is a barrier to entry.

For investors and strategic buyers, the competitive map highlights two recurring value routes: breadth-led scale (parts distribution plus refurbishment throughput) and depth-led specialization (vintage equipment expertise, proprietary test capability). Our report provides a capability-mapping tool that identifies which route best fits different strategic objectives.

Recent developments and market dynamics shaping 2026

- Capital investment waves: Industry associations reported a surge in announced manufacturing projects and related investments since major national incentives—an input that feeds sustained demand for aftermarket services as fabs scale and diversify geographies.

- Price and lead-time volatility: Multiple suppliers signalled material price increases in early 2026, and lead times for some semiconductor categories have extended into multiple-quarter durations. These dynamics make refurb and exchange programs a practical hedge.

- Regulatory texture: New tariff proclamations and export controls introduce both constraints and carve-outs—repair and R&D activities are often preserved, creating a strategic operational corridor that service providers can exploit if compliance is managed proactively.

- Circularity and sustainability: Recent facility launches focused on eco-friendly refurbishment and material recovery underscore a rising regulatory and end-customer preference for lower-footprint supply options—an important differentiator in supplier selection.

Practical recommendations for 2026 planning

- Adopt a scenario-weighted approach: Build planning scenarios that stress-test your maintenance strategy against high-price/high-lead-time and low-price/normalized-lead-time outcomes. Use the TCO templates in our study to quantify break-evens for repair vs replacement.

- Localize critical maintenance pathways: Where tariffs or licensing create friction, prioritize localized repair hubs or certified local partners to preserve uptime while staying compliant.

- Monetize aftermarket services: Operators with service capability should consider standardized exchange programs and warranty bundles—these convert one-off repairs into recurring revenue while smoothing capacity utilization.

- Vet partners for vintage expertise: Assess suppliers not just on throughput, but on traceable repair methods, parts provenance and warranty frameworks—these attributes materially affect long-term reliability and cost of ownership.

- Pursue capability M&A selectively: Target assets that fill technical gaps (metrology, high-voltage stacks, single-chamber refurb engineering) or that accelerate geographic market access under restrictive trade regimes.

Conclusion — next steps for executives

For leaders deciding capital allocation, procurement strategy, or M&A activity in 2026, the Semiconductor Part Refurbishment & Repairs report functions as a tactical playbook and a strategic market map. It translates macro drivers—continuing fab investment waves, pricing and lead-time pressures, and shifting trade/regulatory regimes—into concrete operational choices across sourcing, servicing and monetization.

This preview outlines the strategic contours; the full report contains the operational metrics, supplier scorecards, and financial models that enable transaction-level decision-making. To access comprehensive segmentation, supplier-level benchmarking, and interactive decision tools—designed to be deployed in procurement negotiations and board-level planning—please visit our report page or contact PW Consulting’s semiconductor practice to obtain the complete dataset and advisory options.

For detailed analysis of this topic, please visit the official page:Semiconductor Part Refurbishment Repairs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com