Middle East and Africa Induced Pluripotent Stem Cells (iPSCs) Market Industry Size and Strategic Market Assessment Report

Health |

2026-05-29 12:25:51

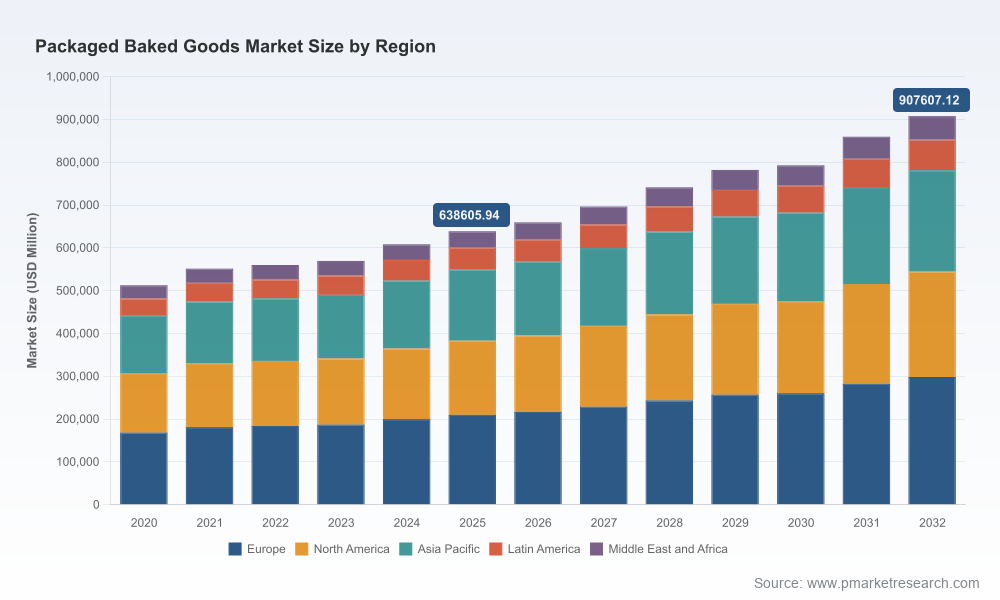

PW Consulting today publishes an executive briefing drawn from our full Packaged Baked Goods Market report (base year 2025), designed to arm C-suite teams, private equity sponsors, and functional leaders with the decision-grade insight required to navigate 2026. The market has moved from an estimated USD 512.5 billion in 2020 to roughly USD 638.6 billion in 2025, and under our baseline forecast it is set to expand at a 5.15% CAGR through the 2026–2032 planning window, reaching approximately USD 907.6 billion by 2032. This trajectory masks important asymmetries—structural drivers, regulatory shocks, raw-material volatility and concentration dynamics—that will determine winners and laggards in the next 18–36 months.

Packaged Baked Goods Market

Timing: The intersection of new labeling proposals, packaging EPR schemes, trade/tariff adjustments and incremental commodity cost pressure creates a compact window for re-pricing, reformulation and contract restructuring. The decisions you take in 2026 will lock in margin structures through the latter half of the decade.

Packaged Baked Goods Market

Scale of the prize: With the global packaged baked goods market measured in the high hundreds of billions (USD) and growing at a steady mid-single-digit CAGR, incremental share gains translate to significant revenue and EBIT upside—or downside if execution fails.

Packaged Baked Goods Market

Fragmentation and competitive posture: The category remains relatively fragmented; leading firms hold a modest slice of global revenue, leaving room for agile players to consolidate niche positions or leapfrog incumbents via channel innovation and cost leadership.

Executive playbooks: Go-to-market blueprints for Retail, Foodservice and E-commerce channels, including SKU rationalization thresholds, private-label engagement strategies, and retailer negotiation levers optimized for 2026 trade calendars.

Product and portfolio decision toolkit: A prioritized NPD matrix that balances margin recovery, clean-label reformulation, and premiumization—backed by demand elasticity scenarios and SKU-level pruning guidance to free up working capital.

Cost-to-serve and procurement levers: Detailed supplier segmentation and sourcing tactics, hedging/contract templates, and a stress-tested cost pass-through model that quantifies impact under differing tariff and commodity scenarios.

Supply chain resilience playbook: End-to-end mitigation options—dual sourcing, regional production hubs, frozen-to-fresh production swaps and logistics-batching tactics—designed to preserve fill rates while containing landed-cost increases.

Regulatory and packaging roadmap: Implementation timelines and compliance checklists to align products and packaging ecosystems with emergent requirements (nutrition front-of-pack signaling, EPR schemes, and material bans), with costed options for recyclability upgrades and supplier certification.

M&A and partnership screening: Deal archetypes and valuation sensitivities for bolt-on versus platform acquisition approaches, plus a shortlist of capability gaps that are most accretive in 2026 (cold chain, direct-to-consumer capabilities, clean-label factories).

Operational risk and recall readiness: Crisis response templates, traceability quick-wins and insurance/indemnity structuring options that reduce reputational and balance-sheet exposure after safety incidents.

The industry roster includes global champions with broad distribution networks, regional powerhouses with deep retail relationships, and specialist players with strong brand equity in sweet and convenience segments. The competitive responses we expect in 2026 fall into distinct playbooks.

Scale incumbents (e.g., Grupo Bimbo, Mondelēz International, Nestlé): Expect accelerated supply-chain optimization and targeted premiumization—squeezing factory productivity and redirecting marketing spend toward higher-margin snack and on-the-go baked formats. These firms will also leverage global procurement to blunt commodity-driven margin erosion and invest selectively in packaging recyclability.

North American branded bakers (e.g., Flowers Foods, General Mills, Hostess Brands, McKee Foods): Anticipate focussed SKU modernization (keto, organic and multi-grain launches are already visible), closer integration with major retailer loyalty programs, and more aggressive private-label defense in key categories.

Regional specialists and emerging-market champions (e.g., Yamazaki Baking, Britannia, Warburtons, Aryzta): Will double down on localization—productizing formats that meet local taste and price points—while selectively exporting differentiated SKUs to diaspora channels and cross-border e-commerce.

Ingredient and supply partners (e.g., Rich Products): Will expand frozen-to-retail options and co-manufacturing agreements as manufacturers seek capital-light capacity solutions.

Recent corporate moves underscore these dynamics: product-line expansions embracing keto and organic claims, retailer launches of ready-to-bake convenience formats, and high-profile safety recalls and allergy alerts that highlight the commercial and legal risks of complex supply chains. These developments reiterate two points: product reputation and supply-chain transparency are financial assets, and operational failures have immediate P&L and share repercussions.

Labeling and nutrition transparency: Proposed front-of-pack nutrition signaling in the United States and similar moves elsewhere will alter shelf perception and may require reformulation or repositioning of legacy SKUs. Delays are possible, but planning and pilot compliance programs should commence in 2026.

Packaging EPR and material restrictions: New EPR laws and container bans are increasing the total cost of packaging compliance. This raises the strategic premium on recyclable and reusable pack formats, as well as supplier partnerships that can amortize retrofit costs.

Tariffs and trade friction: Recent tariffs on agricultural and packaging inputs are exerting upward pressure on landed costs. Expect procurement teams to redesign sourcing footprints and negotiate indexed contracts to mitigate swings.

Commodity volatility: Wheat and flour markets have shown variability that compresses margins in thinly priced categories. Scenario planning with unit-cost breakpoints is essential for margin protection and price cadence strategies in 2026.

Prioritize actions that preserve gross margin today without sacrificing long-term brand equity: selective SKU delisting, tactical price architecture, and value-tier innovation are higher-return moves than across-the-board price increases.

Invest in labeling and packaging readiness now: even if regulatory timelines stretch, early movers win shelf-space and reduce 2026–2027 compliance costs.

Lock strategic supply arrangements and flex capacity: multi-year supplier accords, optionality in raw-material sourcing, and co-manufacturing can convert input uncertainty into competitive advantage.

Build a digital-first distribution layer: the rise of e-commerce and direct-to-consumer bundle formats means channel diversification is no longer optional for premium growth and consumer testing.

Use M&A to acquire capabilities, not just volumes: targets that provide cold-chain, clean-label capacity or DTC fulfilment will be more valuable than scale-only acquisitions.

This press briefing is intended to demonstrate the analytical depth and tactical relevance of PW Consulting’s Packaged Baked Goods study while preserving the granular segment and regional splits that deliver operational value. The full report contains the complete segmentation by region, product type and channel with near-term forecast slices, granular SKU-level elasticity testing, and modeled price/margin sensitivities—information that will materially change negotiation stances, capex phasing, and M&A valuation models. We purposely withhold those segment-level tables here to encourage decision-makers to access the full dataset and proprietary scenario workstreams.

For C-suite briefings: Schedule a tailored session with our industry leads to translate the findings into a 100-day strategic plan for 2026.

For private equity: Use our acquisition playbooks and screening filters to refine target lists and term-sheet assumptions in market processes launched in 2026.

For commercial and product leaders: Request the retailer negotiation and SKU rationalization modules to implement immediate margin-protection measures ahead of the 2026 promotional calendar.

PW Consulting’s Packaged Baked Goods Market report combines rigorous market-sizing, scenario-driven forecasting and hands-on implementation tools. For access to the full report, proprietary datasets and to arrange a bespoke strategy workshop, please contact PW Consulting’s Packaged Foods practice.

For detailed analysis of this topic, please visit the official page:Packaged Baked Goods Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com