BT Laminate Market 2026 Strategic Brief — Actionable Insights for Corporate Decision‑Makers

PW Consulting — Senior Strategic Advisor & Chief Industry Analyst

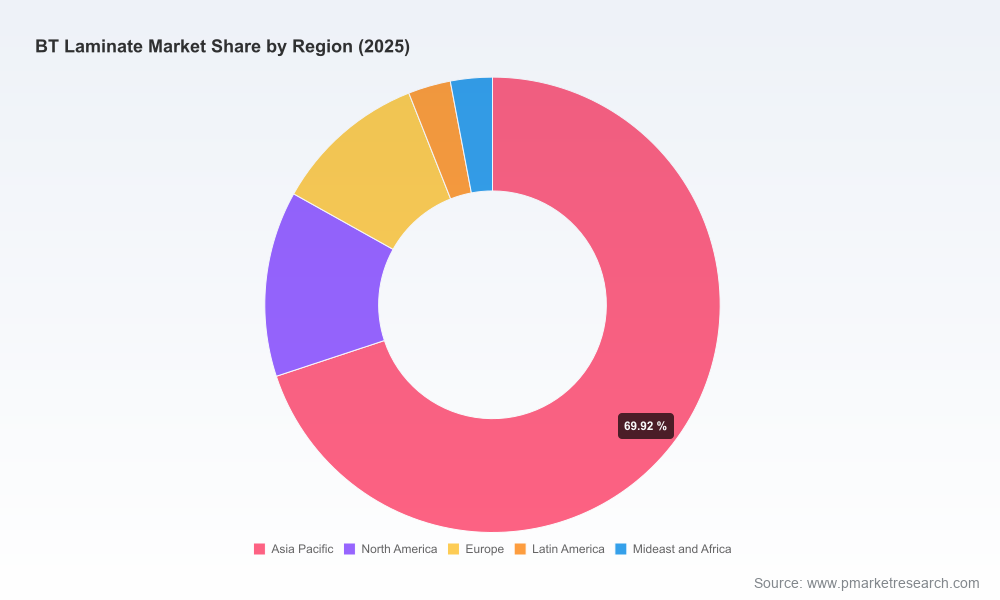

BT Laminate Market

Executive snapshot

The global BT (benzocyclobutene) laminate market is at an inflection point. Our latest market model values the industry at USD 3,212.45 Million in the 2025 base year and projects expansion to USD 5,243.45 Million by 2032, representing a compounded annual growth rate (CAGR) of 7.25% over the 2026–2032 forecast window. The 2026 step‑change will be driven by structural demand from semiconductors and high‑speed interconnects, concurrent with supply‑side re‑pricing and material constraints. For executives planning capital allocation, sourcing strategies, or M&A in 2026, these dynamics create both acute risks and clear, time‑sensitive opportunities.

BT Laminate Market

Why this brief matters for 2026 decisions

- It synthesizes near‑term price and supply shocks with multi‑year demand trends so leaders can prioritize immediate interventions without losing sight of secular growth.

- It frames tactical options — procurement, pricing, product strategy, capacity, and partnerships — that materially affect margin and market share through 2026 and beyond.

- It translates technical signals (low‑warp, low‑loss, halogen‑free BT grades) into commercial actions: which customers to defend, where to invest, and which assets to consider in M&A or JV discussions.

Market dynamics shaping 2026

The 7.25% forecast CAGR masks heterogenous forces that will command executive attention next year. We group these into three vectors:

BT Laminate Market

1. Supply‑side pressure and pricing

- Upstream inputs — copper foil, electronic‑grade glass cloth, specialty resins and logistics — experienced notable cost escalation in 2025–2026. This is not a localized price blip but a structural adjustment driven by constrained supply and higher energy/transportation and labor costs.

- In April 2026, a major BT resin and laminate supplier implemented a uniform 30% price increase across core materials. That action is the most consequential single pricing event in the sector in nearly a decade and will serve as a benchmark for spot and contract negotiations in 2026.

- Supply constraints in electronic‑grade fiberglass cloth tightened availability late in 2025, reducing short‑term substrate flexibility for memory and high‑density packaging customers during the start of 2026.

2. Technology and regulation as demand multipliers

- BT laminates are evolving from a commodity substrate to a differentiated materials play: low‑warpage, halogen‑free, and low‑transmission‑loss grades are now table stakes for advanced IC packaging, RF/microwave applications, and high‑reliability automotive electronics.

- Regulatory and OEM requirements for reduced hazardous substances are accelerating adoption of halogen‑free formulations — a shift that raises qualification time and upfront R&D investment but supports premium pricing and durability of revenue streams.

3. Concentration and competitive dynamics

The market remains oligopolistic, with the top three players controlling a dominant share and the top five commanding over 90% concentration by revenue. That structure produces two practical implications for 2026:

- Sellers have increasing leverage to pass through cost inflation, but only up to the point where demand elasticity and qualification cycles bite. Buyers should assume higher baseline ASPs in contract renewals.

- For challengers and fast followers, targeted differentiation (material grade, local capacity, service, co‑development) is the path to scale; competing on price alone is a weakening proposition in the face of upstream cost volatility.

Competitive landscape — what to watch in 2026

Our competitive assessment focuses on strategic positioning rather than market share micro‑data. Key players include legacy resin inventors, global PCB material groups, and regional scale manufacturers. Their differentiators are summarized below:

- Mitsubishi Gas Chemical Company (MGC) — Inventor of BT resin with deep IP in low‑warp and advanced grades. Recent award recognition for next‑generation low‑warp materials and a decisive 30% price adjustment in April 2026 make MGC a price leader and technological bellwether.

- Isola Group — Broad product portfolio focused on automotive and telecom customers; strength in advanced PCB materials and high‑density interconnect segments.

- Panasonic — Emphasis on thermal stability and signal integrity for consumer and packaging markets; global brand and channel reach.

- Shengyi Technology (SYTECH) — Large copper‑clad laminates manufacturing footprint, scale supply to 5G and compute markets; price competitive with regional integration benefits.

- Rogers Corporation — Specialist in RF/microwave and high‑performance substrates; attractive partner for high‑frequency applications.

- Sumitomo Bakelite, Nan Ya Plastics, ITEQ, Kingboard, Ventec, Doosan, and Elite Material — Each brings complementary strengths in scale, regional access, high‑reliability certifications, or niche product lines suitable for automotive, aerospace, or advanced packaging customers.

Strategic implications and recommended actions for 2026

We translate market signals into a concise 6‑point action set for executive teams making choices in 2026.

- Re‑price contracts proactively. Use supplier cost pass‑through as a negotiating baseline, incorporate indexed clauses, and prioritize multi‑year contracts with volume flexibility to stabilize supply and margin.

- Accelerate qualification of halogen‑free and low‑loss BT grades. OEMs and Tier‑1s will shorten acceptable supplier lists; early qualification locks higher ASPs and long lifecycle revenues.

- Implement a supply continuity playbook. Tactical measures include dual‑sourcing of glass cloth and copper foil, strategic inventory buffers for critical laminates, and near‑term co‑investment in upstream input capacity with strategic suppliers.

- Reassess capital projects vs asset‑light growth. Given the projected growth trajectory through 2032, selectively green‑field capacity makes sense only where long‑term feedstock is secured and time‑to‑revenue aligns with multi‑year demand curves; otherwise favour tolling, JVs, and offtakes.

- Pursue targeted M&A and JV opportunities. Focus on entrants that offer material differentiation (e.g., low‑warp grades, regional fabs with strong OEM ties) or access to constrained inputs — these can accelerate share gains in an otherwise concentrated market.

- Stress‑test product roadmaps against regulatory drift. Build a compliance matrix for emerging halogen and chemical mandates and prioritize R&D that shortens qualification while protecting IP.

Scenario thinking — three plausible 2026 inflection points

We recommend using scenario analysis for capital and procurement choices. At a high level:

- Baseline: Demand growth continues along the forecast CAGR; suppliers pass through a significant portion of input inflation; customers accept higher ASPs but extend qualification cycles. Outcome — steady revenue expansion with margin compression for non‑differentiated producers.

- Upside: Acceleration in memory and advanced packaging driven by AI and compute capacity expansion shortens payback on greenfield investment. Outcome — pricing stabilizes as volumes absorb higher costs; early investors capture outsized share.

- Downside: Prolonged raw material shortages or additional supply constraints (e.g., glass cloth) coincide with weakened end‑market demand, forcing deeper discounting and capacity idling. Outcome — consolidation accelerates and strategic buyers can acquire assets at attractive multiples.

What PW Consulting’s full report delivers (practical, executable content)

Our full BT Laminate Market report goes beyond narrative to provide tools that leaders can action within 90–180 days. Highlights include:

- Financial model with top‑down market projections and unit economics that can be customized to your supply‑chain, contract terms and portfolio mix.

- Supplier scorecard and risk heatmap assessing technology, capacity, margin sensitivity, and replacement lead time.

- Procurement playbook with contract clauses, indexation templates, and negotiation tactics for pass‑through and volume commitments.

- CapEx decision framework and ROI thresholds calibrated to our scenario suite and time‑to‑qualification inputs.

- M&A target shortlist and synergies template focusing on technology, regional access, and raw material control.

- Regulatory compliance checklist and product qualification workflows for halogen‑free and low‑loss BT grades.

How to use the intelligence — immediate priorities for leadership

- Finance: Re‑model 2026 budgets and covenant stress tests to reflect elevated baseline costs and potential ASP normalization timelines.

- Procurement: Execute supplier stress tests and secure priority allocation agreements for glass cloth and copper foil before H2 2026.

- Product & Engineering: Fast‑track cross‑functional qualification programs for premium BT grades to capture emerging OEM spec windows.

- M&A & Strategy: Revisit acquisition targets with a focus on upstream integration or differentiated IP to defend margins under higher cost structures.

Closing — why 2026 is a strategic pivot

The combination of secular demand (advanced packaging, RF, automotive electronics) and a materially higher cost baseline driven by upstream inflation creates a strategic pivot point. Firms that treat 2026 as a year of disciplined repositioning — tightening supply chains, codifying price pass‑through, investing selectively in differentiation, and using M&A opportunistically — will convert near‑term disruption into durable competitive advantage.

Next steps

PW Consulting’s full BT Laminate Market report provides the models, supplier assessments, and playbooks referenced here. For teams that must turn insight into action in 2026, the report is designed as a deployable toolkit rather than a static study. Visit our report page to access the complete analysis, download the interactive financial model, and schedule a strategy workshop with our industry team.

For detailed analysis of this topic, please visit the official page:BT Laminate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com