TheDrewHouse Apparel for Stylish Casual Looks

Shopping |

2026-05-11 20:17:42

PW Consulting's new market research publication on PHS (polyhydroxystyrene) resins for KrF photoresists offers a timely, decision-grade synthesis for executives, investors, and procurement leaders preparing for 2026. This briefing distills the strategic takeaways from our full report: market trajectory, competitive positioning, supply–demand levers, and the practical toolset our clients use to convert insight into action. In keeping with the “trailer” principle, we expose the analysis framework and directional conclusions while reserving proprietary segment-level matrices and supplier scorecards for report subscribers.

PHS Resin for KrF Photoresist Market

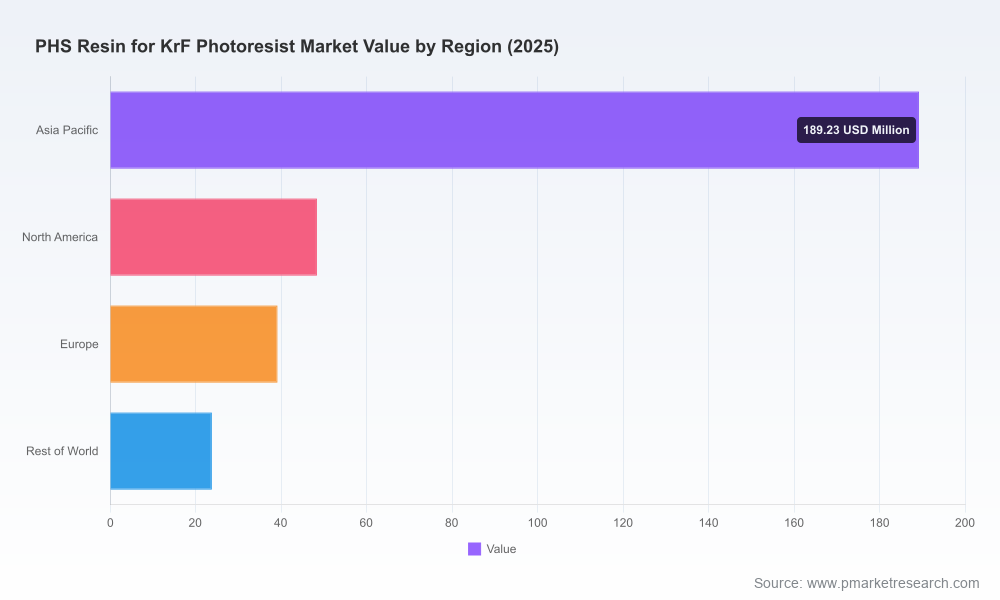

The global PHS resin market serving KrF photoresist applications is at an inflection point. Our base-year assessment places the market at approximately USD 301 million in 2025; the demand pathway embedded in our forecast model implies a mid-single-digit compound annual growth rate (CAGR) of 6.82% through the 2026–2032 horizon. Under the central-growth scenario, this market rises steadily toward the latter half of the decade, driven by a mix of legacy node lithography needs, incremental capacity for specialty packaging, and regional supply-chain rebalancing.

PHS Resin for KrF Photoresist Market

Optical and process fit: PHS-based polymers retain a unique combination of transparency at 248 nm, thermal stability, etch resistance, and predictable behavior when functionalized with protective groups and photoacid generators. These attributes sustain their centrality for KrF chemically amplified resist platforms.

PHS Resin for KrF Photoresist Market

Qualification inertia: Mature fabs continue to prefer qualified PHS chemistries because qualification cycles for resist materials are long and the risk of yield-impacting impurities is high. This makes PHS not only technically preferred but operationally entrenched for many customers.

Regulatory vectors: Industry-level efforts to reduce persistent or problematic chemistries (for example, certain fluorinated PAGs) are accelerating. To date, full-performance non-PFAS PAG replacements for KrF-class performance have not materialized at scale, creating both compliance pressure and R&D opportunity for PHS ecosystem participants.

Capacity and localization: Leading suppliers have announced capacity increases and validation programs. These moves change qualification timelines and create windows for new entrants and domestic substitution initiatives to secure demand from local photoresist formulators.

Concentration and bargaining power: The market demonstrates high concentration at the top tiers of supply. A small group of established suppliers controls a majority of commercially available, high-purity PHS offerings, which affects negotiating dynamics and time-to-qualify for alternative sources.

Segmentation of demand: Continued demand comes from mature-node logic and memory (including advanced packaging and 3D-stacking flows) even as leading-edge lithography shifts to shorter wavelengths. The coexistence of legacy and advanced flows sustains a robust addressable market for KrF chemistries across several manufacturing profiles.

Price and raw-material volatility: Feedstock variations and shifts in polymerization capacity introduce periodic pricing pressure. Procurement strategies that rely on single-sourced, long-lead suppliers face elevated exposure during capacity ramp cycles.

Technology and formulation R&D: Incremental improvements—copolymer design, protective-group chemistry, and PAG tuning—remain primary levers for performance and for differentiation among suppliers. Intellectual property around these formulation building blocks is increasingly a commercial moat.

Our competitive analysis synthesizes corporate footprints, technology roadmaps, capacity signals, and recent public developments. Two features stand out: (1) a group of long-established Japanese and U.S. players maintains leadership in high-purity, qualified PHS resins; and (2) a growing cohort of regional Chinese suppliers is maturing from pilot to commercial scale, supported by domestic demand and strategic investment.

Nippon Soda Co., Ltd. — A long-standing supplier of high-purity PHS derivatives and branded polymer platforms. Strengths: deep chemistry expertise and longstanding customer relationships in KrF resist supply chains.

Maruzen Petrochemical Co., Ltd. — Known for its PHS polymer lines used as base polymers in KrF systems; positions itself on polymer control and reproducibility.

Shin-Etsu Chemical Co., Ltd. — Offers advanced lithography materials and protected PHS systems; benefits from scale and integrated materials know-how across semiconductor chemicals.

DuPont de Nemours, Inc. — Expanded capacity in recent years and leverages formulation expertise across KrF and other DUV chemistries; strategic moves suggest a focus on secure supply for major customers.

TOHO Chemical Industry Co., Ltd. & Tokyo Ohka Kogyo (TOK) — Both maintain technology-rich portfolios with strong emphasis on compatibility between polymer backbone design and PAG strategies, useful for customers seeking tuned performance.

Chinese ecosystem players (selected) — Several companies have transitioned from lab and pilot outputs to kilogram-to-ton scale production and are positioning on cost, proximity, and tailored supply agreements. Their trajectories are noteworthy for buyers aiming to diversify supply or localize content.

Our full study is structured as a practitioner’s playbook, not just an academic exercise. Core deliverables include:

Validated market-sizing and demand-model spreadsheets calibrated to lithography node mix and application-tailored take-rates, with sensitivity toggles for scenario planning.

Supply-mapping and capacity-phasing visualizations that reconcile announced expansions, pilot programs, and likely commissioning timelines.

Supplier scorecards that synthesize technical capability, scale readiness, qualification track record, and commercial posture to support sourcing decisions.

Technology deep-dives on polymer architecture, protective-group choice, and PAG interactions, including decision trees for formulation trade-offs.

Procurement playbooks (dual-sourcing templates, stock policy optimization, lot-acceptance criteria) and an M&A screening framework for companies targeting vertical integration or bolt-on acquisitions.

Risk heatmaps (supply disruptions, regulatory exposures, feedstock volatility) with mitigation pathways prioritized by cost-to-implement and time-to-benefit.

For resin manufacturers: Balance near-term volume capture with investment in formulation IP. Prioritize quality-by-design processes to shorten qualification cycles for large OEMs and claim a premium position against lower-cost entrants.

For photoresist formulators: Implement staged qualification programs to diversify sourcing without compromising yield. Lock early co-development agreements with polymer suppliers to secure prioritized dispatch during capacity tightness.

For semiconductor fabs and package houses: Treat KrF PHS supply as a strategic input. Define multi-year demand profiles and support vendor validation where strategic alignment reduces overall supply risk.

For investors: Track consolidation signals and capacity announcements closely. Targets with robust process control, validated customer footprints, or proprietary protective-group chemistry present asymmetric value capture opportunities.

For policy and procurement planners: Consider targeted incentives that accelerate domestic qualification capabilities, but calibrate support to avoid lock-in on subscale technologies that cannot meet high-purity semiconductor standards.

Organizations that convert our insights into executed plans use three control points: a clear demand-to-capacity roadmap, a prioritized supplier engagement playbook, and an operational qualification timeline aligned with fab ramp schedules. The full PW Consulting study provides the quantitative models, supplier intelligence, and checklist templates needed to reduce time-to-decision and shorten negotiation cycles while safeguarding yield outcomes.

This brief outlines the strategic contours of the PHS resin market for KrF photoresists and the critical levers for stakeholders planning their 2026 moves. We have highlighted high-level market sizing, concentration dynamics, technology drivers, and the practical deliverables executives need to move from strategy to implementation. The detailed, segment-level datasets, supplier scorecards, and interactive demand-model workbooks that underpin these conclusions are available in the full report and through our advisory services. For teams that need to finalize capital plans, secure long‑lead chemical agreements, or evaluate M&A targets in 2026, the full PW Consulting package is designed to be the operational reference.

Contact PW Consulting or visit our report page to request the full PHS Resin for KrF Photoresist Market report, to schedule a tailored briefing, or to commission a bespoke scenario analysis aligned to your portfolio.

For detailed analysis of this topic, please visit the official page:PHS Resin for KrF Photoresist Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com