Palm Kernel Shell (PKS) Market Outlook 2026: Strategic Imperatives for Energy Buyers, Processors and Investors

Executive summary

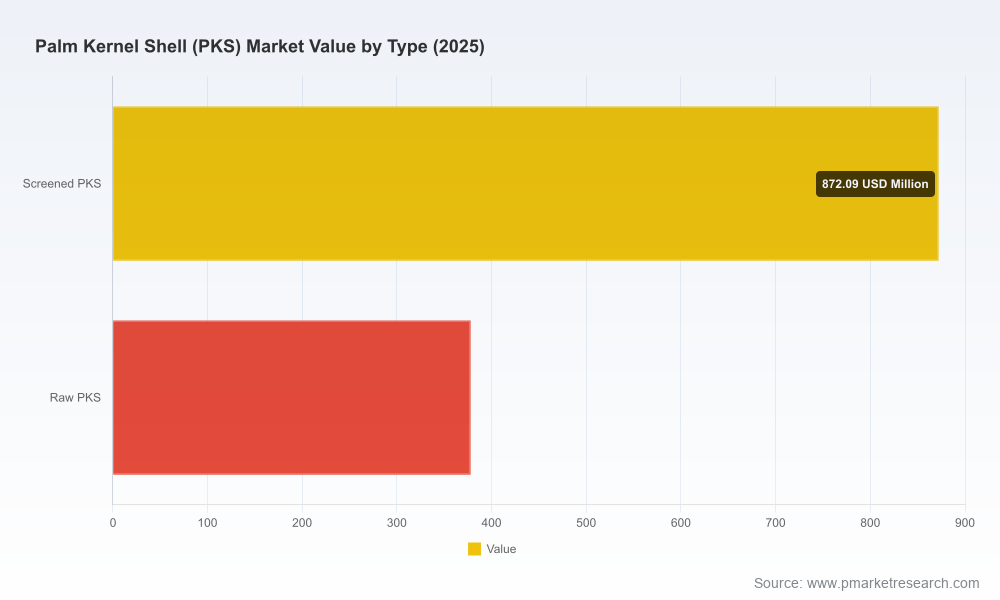

PW Consulting’s latest Palm Kernel Shell (PKS) Market report — with base year 2025 and a forecast window to 2032 — crystallizes the practical intelligence procurement teams, plant operators, and strategic investors need to act with confidence in 2026. The global PKS market expanded steadily from the early 2020s, reaching USD 1,250 million in 2025, and is projected to grow at a 6.0% compound annual growth rate (CAGR) through 2032, reaching roughly USD 1,880 million by the end of the forecast horizon. These headline figures reflect an established biomass commodity that is maturing into a tradable, policy-sensitive, and increasingly certified supply chain.

Palm Kernel Shell (PKS) Market

Why this matters for 2026 decision-making

Energy buyers, cement and steel operators, and biomass processors are all facing a 2026 landscape where commercial outcomes will be driven as much by policy and certification regimes as by classical supply-demand fundamentals. Our report translates the macro trajectory into three immediate decision nodes for 2026:

Palm Kernel Shell (PKS) Market

- Procurement strategy: locking flexible supply contracts and specifying certification and quality clauses to preserve premium value under tightening subsidy regimes;

- Capex planning: sizing processing, drying, and storage investments to secure margin capture from “cleaner” PKS product lines; and

- Market entry and M&A timing: assessing consolidation risks and partnership pathways as the market displays moderate concentration and several large integrated players deepen their downstream roles.

Market trajectory: what the numbers reveal (without giving away the splits)

The PKS market’s growth to USD 1,250 million in 2025, after consistent expansion since 2020, underpins a business case for investment in processing, logistics, and certification services. Projected to grow at about 6.0% CAGR through 2032, the market is becoming large and liquid enough to support standardized contracts and indexation mechanisms for long-term offtake. Our analysis shows that this maturity is accompanied by regional flows, trade policy levers, and buyer-driven quality segmentation that collectively reshape pricing dynamics and supply security considerations.

Palm Kernel Shell (PKS) Market

Key dynamics reshaping supply and demand in 2026

- Certification and subsidy access: Regulatory tightening in major buyer markets is elevating third‑party environmental certification as a non‑negotiable. For example, buyers operating under feed-in tariff schemes now require robust certification pathways, forcing suppliers to invest in recognized schemes to retain market access.

- Trade and fiscal levers: Export taxes and levies have become a deliberate policy tool in producer countries, altering landed cost calculations and prompting suppliers to re-optimize logistics and contract clauses. Market participants should treat such levies as an ongoing variable in pricing models.

- Processing and quality differentiation: Investments in drying, screening, pelletizing and covered storage are increasingly rewarded with price differentials because “cleaner” PKS attracts premium demand from industrial users seeking predictable combustion and emissions performance.

- Supply base & raw availability: PKS is a milling byproduct with multi‑million‑ton annual availability from key producing countries. That inherent scale supports established export corridors and the emergence of specialist processors focused on value‑added PKS products for international markets.

- Demand concentration and offtake patterns: The market shows moderate concentration among top suppliers and integrated groups, making strategic partnerships, offtake diversity, and counterparty due diligence essential for buyers seeking resilience.

Competitive landscape: who matters and what they are doing

Our competitive mapping identifies several distinct supplier archetypes and specific corporate strategies that buyers should treat as market signals.

- Specialist traders and aggregators (e.g., firms sourcing across Indonesia and Malaysia) are positioning PKS as a certified, carbon‑neutral biofuel for biomass power plants; they emphasize multi-source supply portfolios and in-house quality analytics to offer contractual reliability.

- Processing-first players have invested in large-scale drying and screening facilities to produce premium PKS products for export markets. These investments reduce moisture and contaminants — improving combustion performance and logistics economics for end-users.

- Integrated palm oil groups treat PKS as an internal resource and a commercial line, often prioritizing internal energy needs but selectively selling to external buyers to optimize mill economics and sustainability metrics.

Specific company examples and strategic behaviors analyzed in the report include:

- Companies emphasizing certified sourcing and in-house testing protocols to meet premium market specs.

- Processors expanding export-oriented capacity near port infrastructure to reduce handling costs and transit risk.

- Large palm groups leveraging scale to offer predictable volumes but often tying supply terms to broader palm oil commercial relationships.

From a market structure perspective, concentration indicators show that the top three suppliers account for a material share of the market, while the top five consolidate a clear majority share — a dynamic that increases the importance of counterparty selection and scenario planning in 2026.

Recent industry developments you must factor into strategy

- Trade promotion and buyer engagement initiatives have accelerated: producer associations and national delegations are actively promoting PKS at international biomass forums, reinforcing established trade corridors to major buyer markets.

- New processing capacity has come online aimed specifically at export-grade PKS, signaling that supply‑side quality upgrades are being monetized and that competition for premium buyers will intensify.

- MoUs and offtake partnerships between processors and power or industrial buyers indicate a shift toward formalized, long‑term supply relationships rather than spot transactions.

- Producer-country fiscal policy — including export taxes and levies — is being deployed to capture additional domestic value, and buyers must explicitly model these in landed cost scenarios.

Strategic implications and practical recommendations for 2026

- Procurement and contract design: Specify certification, moisture, and foreign‑matter tolerances and include step‑in rights for alternative certified suppliers. Where feasible, build pricing clauses that reflect variable export levies and certification costs.

- Portfolio construction: Blend offtake tenors across spot, medium‑term, and processed‑product contracts to balance price exposure and supply security. Consider layered supply from specialist processors and integrated producers to diversify risk.

- Capex and logistics: Prioritize covered storage and upstream processing (drying/screening) where on-site economics justify the investment. For buyers without scale, partner with port‑proximate processors to reduce moisture and quality risk.

- Certification and compliance pathway: Integrate third‑party certification timelines into procurement cycles. Failure to secure certified supplies may preclude access to certain subsidy regimes and utilities’ procurement lists.

- Scenario planning: Run upside and downside scenarios that incorporate export tax adjustments, certification adoption rates among suppliers, and shifts in offtake patterns from power generation to industrial cofiring.

What the PW Consulting PKS report delivers (practical toolkit)

Designed as an operational playbook for 2026, the report combines market intelligence with ready‑to‑use decision frameworks. Key elements include:

- Granular market size and trend modeling from 2020 to 2032, with clear base‑case, upside and downside scenarios;

- Supply chain maps and source‑country risk heatmaps that identify concentration risk, logistics bottlenecks, and port/processing infrastructure choke points;

- Procurement templates and contract clauses for quality, certification and force majeure tailored to PKS-specific risks;

- Price build‑up models and landed cost calculators that incorporate export levies, certification premiums, and processing differentials;

- Competitive profiles and strategic playbooks for the leading producer, processor and trader archetypes, including actionable negotiation levers and partnership models;

- Implementation roadmaps for buyers and processors aiming to upgrade product specification, secure certified supply, or invest in processing capacity.

How to use the report in your 2026 planning cycle

For procurement teams: align sourcing tenders with certification timelines and include optionality for processed PKS as a premium line. For operations and engineering: use the report’s capex calculators to evaluate the payback period of drying, screening and storage investments under different fuel price trajectories. For corporate strategy and M&A teams: use our concentration maps and supplier scorecards to identify partnership targets and acquisition candidates that close strategic gaps in geography, certification, or logistics.

Next steps and access to full intelligence

PW Consulting’s PKS Market report is structured to move teams from insight to contract and from hypothesis to execution. This article highlights strategic takeaways and headline market metrics to guide 2026 planning; however, detailed regional and application splits, vendor‑level benchmarking, and the full set of price and volume matrices are intentionally withheld in this press summary.

For procurement playbooks, contract templates, and the complete dataset — including the region‑by‑region and application‑level analysis that underpins our scenario models — access the full report via PW Consulting’s report page. Our team is also available for bespoke briefings and scenario workshops that translate the findings into a detailed action plan for your organization.

For detailed analysis of this topic, please visit the official page:Palm Kernel Shell (PKS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com