Amorphous Metal Sheets Market 2026: Strategic Imperatives for Executives — PW Consulting Release

PW Consulting today publishes an executive briefing accompanying our full Amorphous Metal Sheets Market report (base year 2025, forecast 2026–2032). The briefing synthesizes the report’s strategic value for 2026 corporate decision-making — distilling market momentum, competitive posture, supply‑chain constraints, regulatory risk, and actionable playbooks — while preserving proprietary segment-level datasets for subscribers.

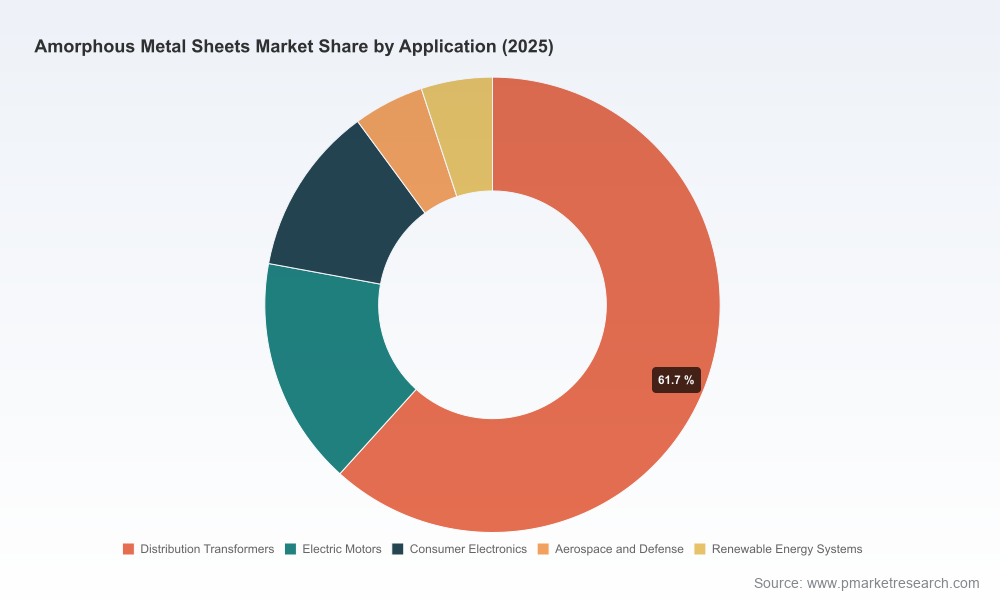

Amorphous Metal Sheets Market

Macro snapshot: growth that forces strategic choices

Our analysis finds a market that has transitioned from a niche materials play into a critical element of energy‑efficient electrical systems. The global market expanded from approximately USD 1.39 billion in 2020 to about USD 2.19 billion in 2025. Under our baseline assumptions, the market is forecast to grow at a compound annual growth rate (CAGR) of 9.4% through 2032, reaching roughly USD 4.10 billion by the end of the forecast window. That trajectory is sustained by stronger end‑market demand for lower‑loss transformer cores and motor laminations, scaling electrification projects, and industrial efforts to meet energy and decarbonization targets.

Amorphous Metal Sheets Market

Why this report matters for decisions made in 2026

- Capital allocation: the growth profile requires CFOs to reassess capex prioritization between raw materials capacity, downstream processing (lamination, stamping, bonding) and high‑precision BMG manufacturing lines.

- Procurement and sourcing: anticipated policy shifts and capacity expansions demand a reassessment of supplier concentration, hedging strategies, and local content requirements.

- R&D and product roadmaps: new amorphous product forms and bonded laminates change design tradeoffs for xEV motors, distribution transformers and power electronics.

- M&A and partnerships: the market’s moderate concentration and ongoing technology consolidation create distinct windows for vertical integration, bolt‑on acquisitions, and strategic alliances.

What the report provides — pragmatic, execution-oriented deliverables

PW Consulting’s full report is built to be operationally useful for boards, strategy teams, and product leaders. Key deliverables include:

Amorphous Metal Sheets Market

- Proprietary bottom‑up revenue model and demand curves by end‑use and region (base year 2025, 2026–2032 forecast) to stress‑test investment cases.

- A cost‑curve analysis covering feedstock, rapid‑solidification processing, lamination and post‑processing to identify margin pools and likely consolidation pressure points.

- Supplier scorecards and capacity maps with capability assessments (ribbon throughput, bonded ribbon, BMG/precision forming, additive options) to inform sourcing and qualification timelines.

- Tariff and regulatory impact module, quantifying effects of recent policy moves and offering mitigation options for import‑sensitive supply chains.

- Scenario toolkits (base, acceleration, downside) tied to quantified KPIs and trigger points to guide contingency planning and capital deployment timing.

- A playbook for OEMs and investors: sourcing playbooks, co‑development templates, M&A screening filters, and regulatory engagement checklists.

Note: this press briefing purposely omits granular segment-level values and percentages that are available only in the full report; this ensures readers can rely on PW Consulting’s validated datasets when making high‑stakes decisions.

Competitive landscape: who matters and why

The market shows a mix of long-standing ribbon specialists, materials innovators focused on bulk metallic glass (BMG), and high‑capacity producers scaling commodity volumes. Our concentration metrics indicate a market where a small group of leaders hold meaningful share — a CR3 in the high‑50s and a CR5 north of 70 — which creates both supplier leverage and clear strategic targets for consolidation.

- Metglas Inc. — a leader in rapid‑solidification ribbon production and a reference supplier for high‑efficiency transformer cores. Their extensive heritage in ribbon and thin‑foil processing makes them a bellwether for product performance expectations.

- Proterial, Ltd. — continuing to invest in bonded laminated ribbon and motor‑grade materials; recent product launches show how materials engineering can unlock higher packing density and handling for xEV motors.

- VACUUMSCHMELZE (VAC) and Heraeus Amloy — European technology‑intensive players focusing on high‑permeability alloys and precision BMG components, respectively, serving electronics, defense and precision industrial markets.

- China‑based manufacturers (multiple large producers) — demonstrating scale through recent capacity additions and aggressive downstream integration; these players are increasingly competitive on both cost and delivery for transformer and industrial applications.

- Emerging specialists (Amorphology, Liquidmetal, Orbray) — focused on high‑value, precision applications leveraging the unique mechanical properties of metallic glass (wear, corrosion resistance, and high strength‑to‑weight), opening new verticals outside commodity transformer work.

Recent corporate moves — such as major capacity expansions in China and targeted technology acquisitions in 2026 — confirm a market in which incumbents are both defending installed bases and investing to capture the next wave of demand.

Supply chain, raw‑material and policy dynamics

- Upstream feedstock: amorphous sheets are predominantly produced from iron‑based alloys with metalloid additions using rapid solidification processes. Broad availability of crude steel and metallurgical feedstocks has remained stable through 2025, but cost exposure is not immaterial and depends on alloy mix and specialty inputs.

- Policy risk: recent tariff actions in April 2026 tightened duties on core metal imports, raising the cost of imported precursors and finished metal products for some buyers. These policy moves create a near‑term incentive to localize production or re‑negotiate supply contracts with tariff pass‑through clauses.

- Decarbonization alignment: amorphous cores materially reduce core losses versus conventional crystalline steel in specific applications, aligning product value with corporate ESG commitments and public policy that penalizes inefficiency.

Technology trends and product differentiation

Two parallel technology pathways are reshaping competitive advantage:

- Process and form innovation for large‑volume electrical applications — bonded laminates, high‑packing‑density ribbons, and improved stamping techniques are enabling replacement of conventional grain‑oriented steels in targeted applications.

- BMG and additive approaches for precision and performance niches — metallic glass processing and powder‑based techniques open applications in robotics, medical devices, and high‑precision gears where mechanical properties drive premium pricing.

Companies that can bridge high‑volume ribbon economics with downstream precision forming will command both scale and margin premiums.

A practical strategic playbook for 2026

- Supply strategy: implement a two‑tier sourcing approach — (1) secure a primary supplier relationship with performance guarantees and long‑lead allocations; (2) pre‑qualify secondary domestic or regional suppliers to mitigate tariff and logistics disruption.

- Capacity and capex: evaluate modular downstream investments (lamination, bonding, stamping) with short payback horizons; prioritize investments that shorten qualification cycles for key OEM partners.

- R&D and customer co‑development: deploy joint design‑for‑material programs with motor and transformer OEMs to accelerate substitution cycles and capture system‑level efficiency value.

- M&A and partnerships: target bolt‑on assets that fill capability gaps (e.g., bonded lamination lines, precision BMG processing, or powder metallurgy for additive routes) rather than chasing large, high‑capex greenfield builds in isolation.

- Regulatory and commercial hedging: incorporate tariff clauses, local content fallbacks, and strategic inventory buffers into supplier contracts; engage regulators early where product energy‑efficiency credentials can influence policy outcomes.

Scenario triggers and what to watch in 2026

Key triggers that will materially change outlooks include rapid capacity ramps from major producers, additional tariff or trade policy shifts, and breakthrough adoption in EV drive motors driven by changes in motor design standards. PW Consulting’s scenario tool links these triggers to financial outcomes and is designed to inform near‑term board decisions about capital allocation and M&A timing.

Conclusion — the strategic edge for 2026

For executives making strategic choices in 2026, the amorphous metal sheets market presents both clear growth opportunity and non‑trivial execution risk. The technology’s alignment with energy efficiency objectives creates enduring demand, while supply concentration, policy volatility, and rapid technological evolution mean that timing, partner selection, and operational flexibility will determine winners.

PW Consulting’s full Amorphous Metal Sheets Market report delivers the granular, transaction‑grade intelligence that boards, investment committees, and corporate strategy teams need to translate market signals into defensible actions. To access the complete dataset, supplier scorecards, and our scenario model that underpins the recommendations in this briefing, please consult the PW Consulting report page.

For detailed analysis of this topic, please visit the official page:Amorphous Metal Sheets Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com