North America Pharmacy Automation Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-09 12:18:22

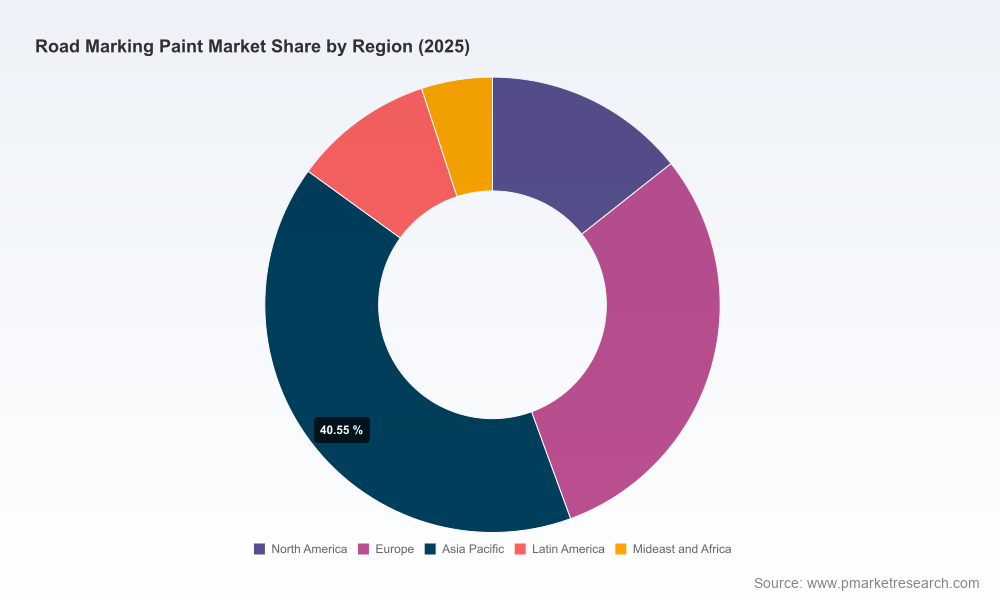

PW Consulting’s new Roadmarking Paints Market report (base year 2025; historical 2020–2025; forecast 2026–2032) delivers a practice‑oriented blueprint for executives, procurement leads, product teams and investors preparing for the crucial 2026 decision window. The market has expanded materially in recent years — driven by infrastructure renewal, elevated safety standards and growing demand for longer‑life materials — and our model projects continued expansion at a compound annual growth rate of 5.8%. From an estimated market value of approximately USD 7.18 billion in 2025, underlying demand dynamics point toward a multi‑billion dollar opportunity by the end of the 2026–2032 forecast horizon.

Roadmarking Paints Market

High‑impact decisions are concentrated in 2026: procurement cycles, formulation roadmaps and regulatory compliance programmes set this year will determine winners and laggards for the next decade.

Roadmarking Paints Market

Our analysis converts macro forecasts into executable choices — from hedging raw material exposure to prioritizing low‑emission coatings that meet evolving public specifications.

Roadmarking Paints Market

We combine quantitative forecasting with supplier‑level strategy so commercial teams can align product development, field operations and go‑to‑market plans around realistic adoption curves and margin scenarios.

Growth drivers: urbanization, renewed road networks, safety retrofits and public stimulus for transport infrastructure underpin steady demand. Lifecycle cost considerations are elevating preferences toward higher‑performance, higher‑upfront‑cost systems in many procurement frameworks.

Product evolution: waterborne formulations and advanced two‑component systems continue to displace older solvent‑heavy offerings in regulated jurisdictions, while thermoplastic and cold‑plastic solutions retain appeal where durability and high‑volume traffic resilience are primary concerns.

Supply chain constraints: volatility in specialty raw materials — notably resins and reflective media — is creating episodic margin pressure; managing these input risks is now a strategic capability, not a back‑office concern.

Regulatory inflection: tightening VOC standards and updated specifications (including recent updates to regional standards such as IS 164 for ready mixed road marking paint) are forcing reformulation investments and influencing procurement criteria.

Market structure: the sector displays meaningful concentration at the top: the three largest vendors capture a majority share and the top five control a strong majority, creating both competitive barriers and M&A opportunities in adjacent niches.

Global market sizing and seven‑year forecasts with scenario variants and sensitivity to input costs (resins, glass beads, solvents).

Regulatory mapping and compliance playbook: where to invest in low‑VOC tech and how to align product claims with emerging public procurement standards.

Raw material cost model and hedging strategies that translate commodity movements into margin impact at product and contract level.

Segment playbooks — capability and profitability profiles for waterborne, thermoplastic and cold‑plastic systems — presented as decision matrices (note: detailed numerical splits by segment and region are available in the full report).

Supplier scorecards and procurement negotiation templates to accelerate tender cycles and shorten time‑to‑award for large infrastructure programmes.

Investor dossier: valuation benchmarks, consolidation targets, and a prioritized M&A heatmap for 2026‑ready targets.

Case studies and implementation checklists from recent public‑sector tenders and private concession projects.

PPG Industries (ENNIS‑FLINT portfolio): leveraging an established waterborne and solvent‑based product suite, PPG is focusing on specification partnerships and global distribution scale. Their strength lies in brand recognition and broad regulatory approvals; strategic priorities include optimized supply chains for reflective media and continued investment in low‑VOC formulations.

Swarco: the firm’s mix of solvent, waterborne and two‑component systems positions it to serve demanding, specification‑driven projects. Swarco’s competitive advantage is a systems approach — combining materials with application equipment and services — which shortens customer procurement cycles and raises switching costs.

Meon Ltd: as a specialized player in line marking paints and cold plastic systems, Meon competes on technical depth and tailored solutions for parking, aviation and municipal clients. Specialist operators like Meon are attractive partners for larger manufacturers seeking niche capabilities or local market access.

Axalta Coating Systems: focused on traditional spirit‑soluble and modified alkyd formulations, Axalta’s strategy is to defend legacy specification relationships while exploring formulation upgrades to meet environmental standards in key markets.

Cloverdale Paint Inc: with regional approvals and waterborne traffic paint formulations compliant with local infrastructure specifications, Cloverdale’s value proposition is trusted performance in regulated procurements and speed to market in their core geographies.

Raw material volatility: episodic price spikes for soda‑lime glass beads and specialty resins materially affect unit economics. Manufacturers with secured supply contracts or vertical integration will preserve margin flexibility.

Regulatory tightening: new and updated standards (e.g., for ready mixed road marking paint and VOC limits) increase entry costs for new formulations and can accelerate obsolescence of solvent‑heavy products.

Procurement dynamics: increasingly, public procurements are shifting to total cost of ownership (TCO) models that favor durable, higher‑performance materials — this changes pricing power and payback calculations for field crews and contractors.

Adoption constraints: in budget‑constrained projects the incremental cost of higher‑performance chemistries can suppress uptake unless sponsors reframe evaluation metrics to include lifecycle benefits.

Manufacturers: prioritize a dual track — accelerate low‑VOC, waterborne or two‑component R&D for regulated markets while pursuing margin protection through long‑term agreements or backward integration for key inputs (reflective media, specialty resins).

Commercial teams: reconfigure tender responses to foreground lifecycle savings and maintenance intervals. Introduce modular service offers (application equipment leasing, training, maintenance contracts) to increase stickiness and generate aftermarket revenue.

Procurement and infrastructure owners: adopt TCO scoring and run pilot programmes to validate longer‑life systems under local traffic and weather conditions. Use staged procurement to phase in higher‑performance specifications while controlling budgetary impact.

Investors and M&A teams: target mid‑sized specialists and regional champions that provide route‑to‑market, technical IP or supply‑chain leverage; consolidation can capture synergies in procurement and R&D while diversifying exposure across product types.

Policy and standards engagement: proactively engage standards bodies and major specifiers where possible — influencing specification language can create first‑mover advantages for compliant formulations.

Custom workshops that convert our quantitative scenarios into board‑level decisions and one‑page investment playbooks.

Due diligence packages for M&A and JV targets, including supplier risk diagnostics and margin stress tests based on raw material scenarios.

Procurement optimisation and specification redrafting support to align tenders with lifecycle value and sustainability goals.

This release is a strategic preview: we have intentionally highlighted market trajectory, competitive dynamics and the decision levers that matter in 2026 while withholding granular segment tables and region/application level breakdowns to preserve the integrity of the full dataset. To access the complete market model, segment‑level forecasts, vendor benchmarking matrices and downloadable cost models, please consult the full PW Consulting Roadmarking Paints Market report and associated data package.

For detailed analysis of this topic, please visit the official page:Roadmarking Paints Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com