PW Consulting LNG Market 2026: Strategic Imperatives for Decision-Makers

Executive summary

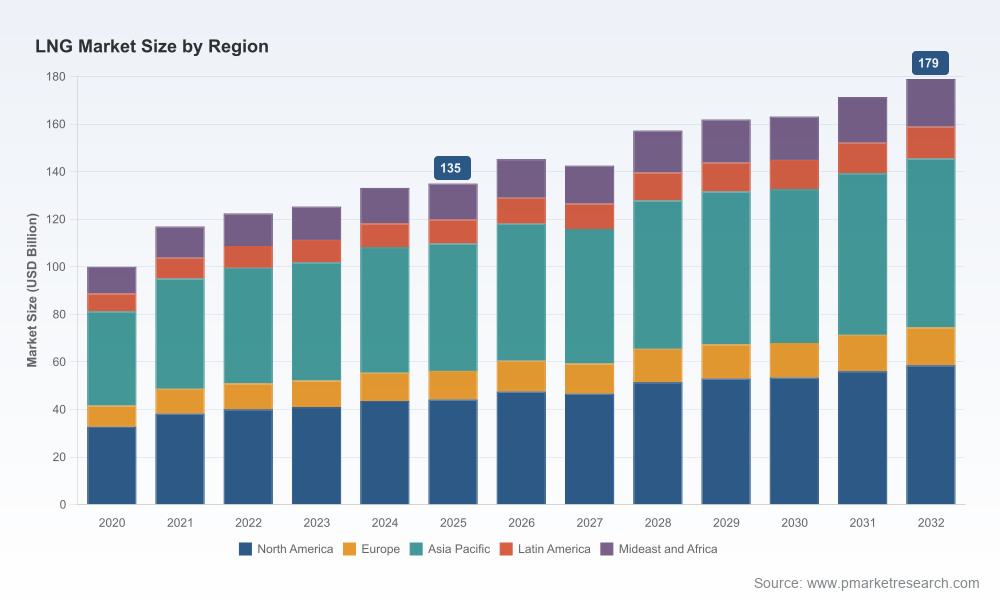

Our latest LNG Market report (base year 2025) equips senior executives, investors, and policy teams with the forward-looking intelligence needed to make high-consequence decisions through 2032. Building on a detailed historical analysis from 2020–2025, the report documents a market that expanded from roughly USD 100 Billion in 2020 to about USD 135 Billion in 2025. After a short-term inflection projected for 2026, total industry revenue is modeled to continue expanding at a compound annual growth rate of 4.09% across our forecast horizon, reaching approximately USD 179 Billion by 2032. These headline dynamics mask material second-order risks and opportunities—our report is designed to make those visible, measurable and actionable for 2026 planning cycles.

LNG Market

Why this analysis matters for 2026 planning

- Timing of investment decisions: Market growth is steady but non-linear. 2026 represents a pivotal year when near-term supply additions, regulatory shifts and evolving trade policy create windows for accelerated FID decisions or, conversely, call for optionality and staged investment.

- Commercial frameworks are changing: Pricing landscapes—anchored by Henry Hub dynamics—and the unfreezing of certain export permit pathways are reshaping contract duration, destination flexibility, and tolling structures. These changes require updated contracting playbooks for sellers and buyers alike.

- Policy and capital allocation: Recent domestic trade-policy and subsidy changes in major markets alter the economics of midstream and decarbonization investments. Companies must reconcile legacy capex schedules with new policy realities to preserve returns.

What the report delivers (practical modules)

We designed the report as an operational toolkit rather than a static narrative. Key deliverables include:

LNG Market

- Top-line and granular forecasts across multiple time horizons, stress-tested under price and demand scenarios.

- Project-level database with development status, expected commissioning windows, capex schedules and key contractual features (note: full project listings and levers are available in the report download).

- Supply–demand modeling that integrates fuel-price sensitivity, shipping constraints, and regasification capacity evolution to quantify shortfalls, surpluses, and marginal volumes under alternative scenarios.

- Commercial playbooks for contract structuring, pricing linkage alternatives, destination clauses and credit mitigation strategies tailored to sellers, buyers and portfolio optimizers.

- Risk heatmaps and mitigation matrices addressing permit timelines, financing stress points, construction risk and counterparty exposure.

- Decarbonization and product-differentiation pathways, including blue and green hydrogen linkages, methane-emissions mitigation options and certification strategies affecting offtake valuations.

- Actionable M&A and JV scorecards that translate strategic bets into financial outcomes and integration checklists.

Market dynamics shaping strategic choices

- Price environment: Natural-gas spot prices remain a primary sensitivity. Our benchmark analysis incorporates an observed Henry Hub average near USD 3.50/MMBtu in 2026 and tests a broad range of stress scenarios to quantify margin volatility across the value chain.

- Regulatory momentum: The resumption of export-permit approvals for a broader set of trade partners (lifted in early 2025) expands addressable markets but also raises competition for liquefaction capacity and charter tonnage. Companies must re-evaluate export strategies and contractual flexibility accordingly.

- Policy and subsidy shock: Recent legislative shifts that roll back some clean-energy tax credits change the calculus for certain low-carbon projects and manufacturing investments. This alters comparative paybacks for decarbonization investments versus traditional efficiency upgrades.

- Supply-side cadence: The market is absorbing a wave of new capacity additions across different project archetypes. Timing and execution risk—rather than structural demand alone—will determine short-term oversupply pockets and price impacts.

Competitive landscape: who matters and why

The LNG ecosystem remains concentrated among a limited set of global, integrated and project-focused players. Market concentration has meaningful commercial effects: the top three firms account for roughly half of market presence, and the top five approach three-fifths—a structure that sustains bargaining power around offtake terms, shipping allocation and capacity reservation. Our competitive chapter provides company-by-company strategic assessments, including capitalization approaches, project development pipelines, trading strength and partnerships that define ready access to key markets.

LNG Market

- Project developers and exporters: Major U.S.-based liquefaction developers continue to anchor incremental export capability, leveraging large-scale plants and integrated logistics. Their playbooks focus on long-term, portfolio-based offtakes and tolling arrangements.

- Global NOCs and IOCs: National oil companies and international oil majors bring deep upstream integration and capital access. Their strategies emphasize supply security, portfolio optimization across regions and direct long-term commercial relationships with buyers in Asia and Europe.

- Trading and marketing specialists: Companies with world-class trading platforms can monetize flex and navigate spot opportunities during dislocations—making trading capability a scalable source of margin.

Our report contains detailed competitive profiles—assessing balance-sheet capacity, contractual exposure, project delivery risk and trading footprints—for leading players whose actions will materially influence market outcomes.

Recent developments that matter (illustrative)

- First production milestones at major new facilities have shifted marginal supply assumptions and reset near-term shipping and berth utilization patterns.

- Multi-decade offtake agreements and inter-company supply pacts are recalibrating long-term offtake baselines for new projects.

- C-suite disclosures and activity outlooks from national producers underscore continued investment in portfolio resilience and regasification capacity upgrades.

These events are woven into our baseline and scenario models so users can quickly see the downstream impacts across revenue, utilization and pricing for their specific exposure set.

Scenarios and what could change the trajectory

- Upside scenario: Faster-than-expected industrial demand recovery in key import regions, combined with moderate fuel-price inflation, drives higher short-term utilization and accelerates merchant cargo trading margins.

- Base case: The market grows at an annualized rate consistent with our central 4.09% CAGR, with near-term volatility around commissioning schedules and short-lived price dislocations.

- Downside: Aggressive policy shifts or sustained low gas prices compress merchant margins, delay FIDs and raise the cost of capital for greenfield liquefaction projects, pushing developers toward smaller, modular or phased approaches.

Each scenario is supported by quantified supply–demand balances, cash-flow ladders, and trigger tables that translate macro moves into specific operational and financial decision points.

How energy companies should use this report in 2026

- Board and Investment Committees: Use the report’s FID decision framework and project-level break-evens to test approval timing and staging options.

- Commercial Teams: Adopt our contracting playbooks to redesign offtake terms, price linkages and destination flexibility that preserve optionality while capturing premium margin where available.

- Trading Desks: Leverage our shipping and cargo arbitrage models to identify structural opportunities and to size forward positions consistent with balance-sheet constraints.

- Policy and Government Affairs: Reference the policy impact analyses to model outcomes under alternative regulatory regimes and to design realistic advocacy strategies.

- Private Equity and Lenders: Apply our risk-adjusted return templates and scenario debt-service stress tests as the basis for diligencing and covenant design.

What we deliberately hold back (and why)

To preserve commercial value and incentivize primary engagement, this release emphasizes strategic insight and methodology while withholding proprietary segment-level tables, project-by-project financials and certain granular region/application stacks. The full report includes interactive datasets, downloadable model templates and project dashboards necessary for transaction execution and competitive bidding.

Next steps — how to get the full intelligence package

PW Consulting’s LNG Market 2026 report is accompanied by an executive workshop, database access and bespoke modeling support for clients preparing 2026 investment cycles. For access to the full dataset, the interactive forecast models and the project-level analytics that underpin our recommendations, please download the full report from our website or contact our research desk to schedule a briefing tailored to your strategic questions.

Final observation

In an environment where a handful of structural forces—price dynamics, permit regimes, and policy shifts—can alter decades of capital planning in months, the premium for decision-quality analysis has never been higher. Our report does not simply predict numbers; it prescribes the analytics and governance changes that enable leaders to convert market insight into defensible, value-accretive action in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:LNG Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com