Polarizer for OLED Market: Strategic Imperatives for 2026 — Preview of PW Consulting’s In-Depth Industry Report

As the OLED ecosystem enters a decisive inflection point, PW Consulting’s forthcoming Polarizer for OLED Market report equips executives with the evidence-based insights they need to shape 2026 strategy. The global polarizer market for OLED displays has moved from niche component to a strategic battleground — driven by rapid adoption of flexible and high-contrast panels, supply-chain volatility in key feedstocks, and the emergent threat of polarizer-less architectures. Our analysis synthesizes historical performance (2020–2025), a robust forecast horizon (2026–2032), and scenario-led decision frameworks so that product, sourcing and corporate development teams can act with clarity in 2026.

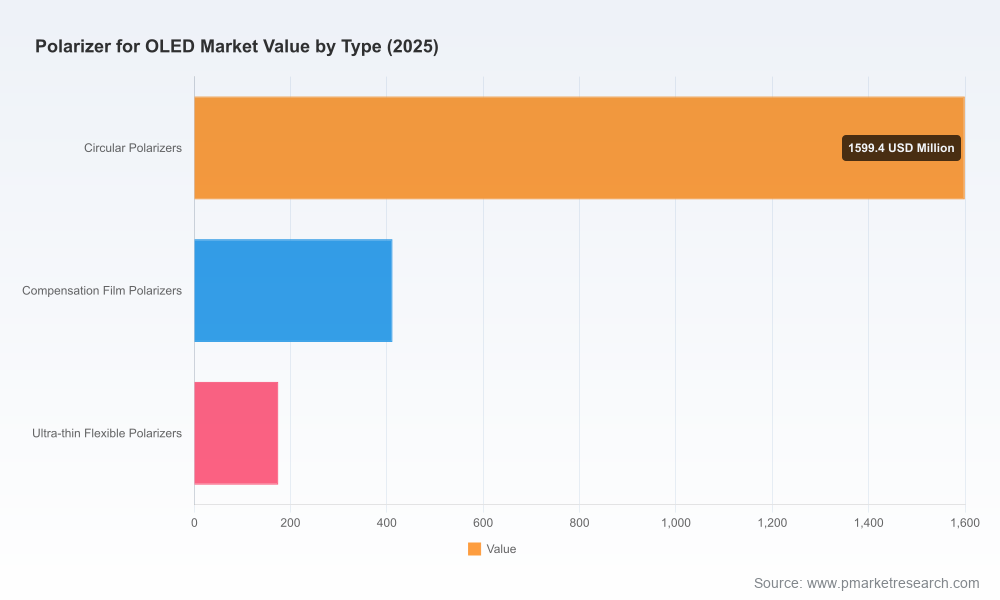

Polarizer for OLED Market

Macro snapshot: growth trajectory and market structure

PW Consulting’s base-year view (2025) sees the polarizer market for OLEDs firmly established as a mid-sized, fast-growing specialty segment with a compounded annual growth rate (CAGR) of 10.32% across our 2026–2032 forecast window. Under our core projection, the market more than doubles in scale across the forecast period, reflecting continued OLED penetration in consumer devices, new form factors (foldables, rollables), and premium large-format displays. Market concentration is substantial: the top three players account for the majority of industry revenues and the top five approach near-complete dominance — a structure that raises strategic questions about capacity, pricing and access for OEMs and smaller suppliers.

Polarizer for OLED Market

Why this matters for 2026 decision-making

- Investment timing: Rapid growth plus high concentration creates asymmetric opportunities — early capacity investments and selective partnerships can secure long-term supply and margin share, while late entrants face higher capital costs and pricing pressure.

- Supply-risk management: Dependence on a narrow set of feedstocks creates volatility windows that can compress margins or delay product roadmaps; 2026 is a critical year to operationalize hedging and sourcing playbooks.

- Technology disruption readiness: Breakthroughs in polarizer-less display approaches are progressing from lab to production feasibility. Companies must both defend current polarizer value pools and prepare transition options.

Key dynamics shaping 2026 strategies

- Raw material pressure: Polarizer manufacturing remains PVA- and iodine-intensive. Iodine market dynamics are non-trivial — recent industry analysis projects multi-billion-dollar demand for iodine in 2026 with a majority of supply concentrated in a single country. This concentration amplifies price and availability risk for polarizer producers and downstream OEMs.

- Margin realities: Public disclosures and industry benchmarks indicate gross-profit mid-single- to low-double-digit ranges for many polarizer businesses. Given this margin profile, small swings in raw material costs or conversion yields materially affect supplier viability and outsourcing economics.

- Trade and policy tailwinds/tensions: Tariff regimes and localization policies are in flux. Policymakers in key production hubs are reconsidering long-standing duty exemptions on display sub-films, while geopolitical frictions continue to influence sourcing decisions and capital allocation.

- Technology substitution risk: Independent analysts and display makers are increasingly public about polarizer-less solutions. Projections show polarizer-less shipments ramping meaningfully into the 2030s for specific product classes — a development that will alter product roadmaps, cost structures and value chains over the next decade.

Competitive landscape — positioning and strategic options

The polarizer value chain is characterized by a handful of established multinational suppliers and an ascending set of regional producers expanding capacity and capability. Our report profiles, benchmarks and scores the leading and emerging suppliers across technology, scale, cost competitiveness and customer exposure.

Polarizer for OLED Market

- Nitto Denko Corporation (Japan) — Distinguished by leadership in ultra-thin and circular polarizer technology, Nitto is well-positioned in flexible OLED niches. Its strengths include depth of process know-how and close integration with display manufacturers. Strategic considerations: continue to monetize premium differentiation while exploring scale partnerships to defend cost curves.

- Sumitomo Chemical Co., Ltd. (Japan) — A major PVA-film incumbent focused on high optical performance films for premium panels. Strategic considerations: translate material science leadership into differentiated supply contracts and co-development with OEMs to reduce substitution risk.

- LG Chem / Shanjin Optoelectronics (Korea / China) — Retained OLED-specific capabilities and access to large-format panel supply chains give this group strength in TV/monitor polarizers. Strategic considerations: balance large-format demand with investments to serve flexible form factors.

- Samsung SDI (Ace Digitech) (Korea) — A specialist in foldable-focused polarizers tightly integrated with Samsung’s display ecosystem; business status is subject to ongoing strategic review. Strategic considerations: decisions here may change competitive access for OEMs and open windows for third-party suppliers.

- BenQ Materials (BQM) (Taiwan) — Notable for bendable circular polarizers and a strong position in foldable device supply chains. Strategic considerations: scale-up execution and IP protection will determine how much value BQM captures as foldables grow.

- Regional players (Japan, Taiwan, China) — A range of mid-tier suppliers are expanding capability sets into flexible films and higher-volume production. Their collective move into advanced polarizers is intensifying price competition and raising the bar on operational reliability.

Strategic playbook for companies in 2026

- Tier-1 suppliers: Double down on technology leadership while negotiating multi-year, value-sharing contracts with OEMs. Consider selective forward integration into sub-film value pools and long-term feedstock agreements to stabilize input costs.

- OEMs and panel makers: Adopt dual-track sourcing — secure incumbent polarizer supply for immediate roadmaps while accelerating co-development of polarizer-less and alternative-thin-film optics to hedge medium-term disruption.

- Private equity and investors: Prioritize capital allocation toward firms with proprietary process IP, diversified customer portfolios, and demonstrable feedstock risk-management strategies. Margin sensitivity analyses (included in our report) are essential to avoid value traps.

- Startups and material innovators: Support rapid prototyping and pilot scale partnerships with established panel makers to de-risk commercialization; licensing or strategic acquisition by established suppliers remains a high-probability exit route.

Operational levers that matter in 2026

- Feedstock security: Locking iodine and PVA via multi-year contracts, geographic diversification, and vertical sourcing partnerships reduces EBITDA volatility. Our report includes supply-chain stress tests and procurement playbooks tailored to polarizer manufacturers.

- Yield and conversion efficiency: Small improvements in coating uniformity, drying cycles and defect rates translate into outsized margin gains. We provide an operations diagnostic framework that quantifies the value of incremental yield improvements.

- Product modularity: Offering configurable polarizer stacks that can be adapted for both conventional and emerging polarizer-less-ready architectures can extend product lifecycles and preserve customer relationships.

- Geographic footprint optimization: Given regional trade uncertainty, optimal footprint strategies balance cost, lead-time and tariff exposure; our scenario models evaluate multiple relocation and capacity-expansion options.

What PW Consulting’s report delivers (practical, actionable content)

The full report is designed as an executable toolkit for 2026 planning cycles. Highlights include:

- Bottom-up demand model (2020–2032) with configurable scenarios (base / fast-adoption / polarizer-less acceleration).

- Supplier benchmarking that combines technology, cost-to-serve, capacity outlook and strategic risk scoring.

- Cost-of-goods sold (COGS) models and sensitivity analyses referencing key raw-material drivers and yield levers.

- Tariff and trade-impact simulations with recommended mitigation pathways for different company archetypes.

- Deal and partnership playbooks for buyers and suppliers, plus a set of M&A valuation cases that reflect margin compression and technology substitution risk.

- Operational checklists for plant upgrades, pilot lines for ultra-thin flexible polarizers, and sample R&D roadmaps to reduce reliance on scarce feedstocks.

Near-term signals to monitor in 2026

- Supplier earnings commentary for raw-material pass-throughs and capacity or utilization announcements.

- OEM display roadmaps that commit to polarizer-less pilots or to new module architectures that reduce polarizer footprint.

- Policy announcements in major manufacturing hubs concerning tariffs, incentives, or localization mandates for optical films.

- Feedstock market moves — particularly iodine pricing and supply concentration events — which can rapidly alter supplier viability.

Concluding guidance for executives

2026 is the year to reframe polarizers from a cost line-item to a strategic frontier. Whether you are a supplier seeking to protect margin and market share, an OEM optimizing supply security, or an investor evaluating exposure to display materials, the decisions you make this year will echo across product roadmaps and balance sheets for the next decade. PW Consulting’s Polarizer for OLED Market report provides the models, scenarios and supplier intelligence necessary to act with speed and confidence — while also prescribing contingency plans for technology substitution and raw-material shocks.

To access the full, data-rich analysis, supplier scorecards, and the interactive scenario model that underpin these strategic recommendations, please visit our report page for the complete dataset and downloadable executive tools.

For detailed analysis of this topic, please visit the official page:Polarizer for OLED Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com