Flutes Instrument Market 2026: Strategic Imperatives for Manufacturers, Distributors, and Investors

PW Consulting’s latest Flutes Instrument Market report (base year 2025) arrives at a moment of structural change: regulatory pressure on cross‑border trade, renewed public investment in music education across emerging markets, and shifting consumer expectations around sustainability and experience. Our analysis shows the global flutes market (USD, revenue in Million) expanded from approximately USD 382.2 million in 2020 to about USD 467.2 million in 2025 and is forecast to reach roughly USD 627.7 million by 2032, tracking a 2026–2032 CAGR of 4.31%. These headline dynamics matter for every executive making product, supply‑chain, channel, or M&A choices for 2026 and beyond.

Flutes Instrument Market

Why this report matters to 2026 decision-makers

- Actionable macro-to-micro line of sight: We bridge top‑line market growth and the operational levers that drive margin and resilience—pricing architecture, sourcing strategies, and lifecycle services—so leaders can translate growth into profitable scale.

- Risk‑aware forecasting: The model integrates geopolitical shocks and tariff scenarios that have already affected trade volumes; this makes the 2026 planning horizon realistic rather than optimistic.

- Competitive playbooks: We unpack the strategic choices available to global OEMs, artisan builders, and education-focused brands—showing where to invest in product, where to defend with cost, and where to partner.

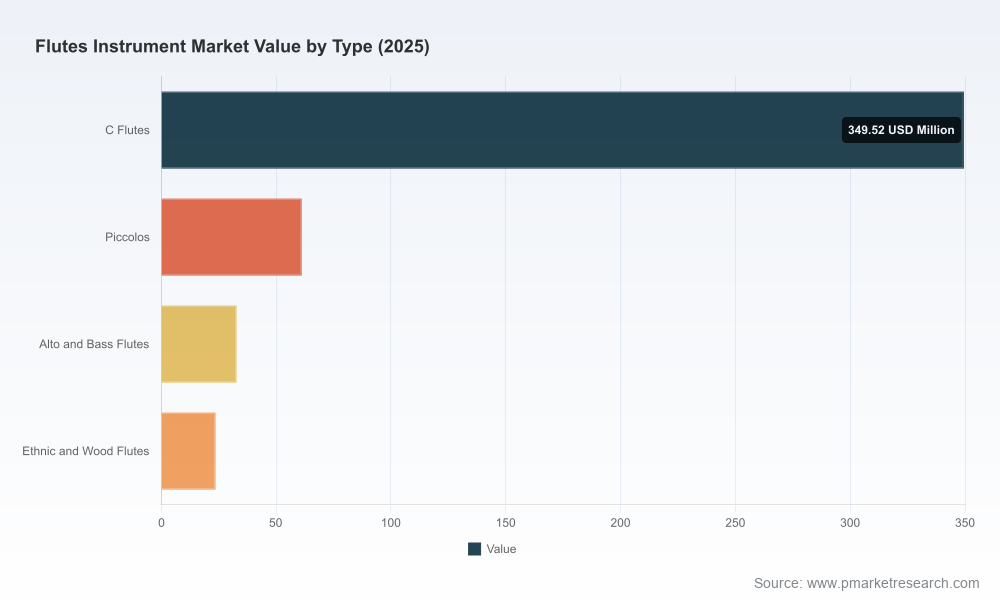

Executive summary of the market trajectory

The flute market is maturing: steady demand from education ecosystems and hobbyists underpins baseline volume, while premium orchestral and bespoke segments sustain higher ASPs (average selling prices). After recovering from near‑term export headwinds, our forecast anticipates steady expansion through 2032 driven by: (a) government investments in music education in several emerging Asian economies, (b) renewed experiential demand—museum exhibitions and cultural programming that spotlight wind instruments—and (c) manufacturers’ product‑level innovation in materials and sustainability. At the same time, trade policy volatility and tariff measures introduced in 2025 have injected cost risk into traditional import channels; risk mitigation is therefore front and center for 2026 planning.

Flutes Instrument Market

What’s inside the report (practical content you can apply in 2026)

- Proprietary market sizing and scenario model (2020–2032) with sensitivity runs for tariff, FX, and education‑funding permutations designed for CFO stress tests.

- Supply‑chain risk matrix: supplier concentration, lead‑time mapping, and near‑term disruption triggers, with recommended mitigation tactics (dual sourcing, nearshoring, local final assembly playbooks).

- Segmentation and product‑tier playbooks: go‑to strategies for student/entry, intermediate, and professional channels—covering pricing, bundling (cases, stands, lesson content), and channel mix by customer lifecycle stage.

- Competitive benchmarking and capability scoring for the 15+ principal market participants—manufacturing footprint, craftsmanship reputation, innovation cadence, distribution reach, and service network.

- Commercial acceleration toolkit: sample channel partnerships with education systems, rental/refurbishment economics for instrument-as-a-service, and a 12‑month pilot roadmap for direct‑to‑consumer premiumization.

- M&A and partnership pipeline: target profiles and valuation heuristics for bolt‑on acquisitions that add product breadth, channel access, or local manufacturing to neutralize tariff impact.

Competitive landscape — how to read the field in 2026

The flute market displays a moderate degree of concentration: the top three players account for a substantial share of revenue, and the top five amplify that position (our analysis records CR3 at 42.8% and CR5 at 56.45%). That structure creates two strategic realities for 2026:

Flutes Instrument Market

- Incumbent advantage in scale and distribution: large, diversified instrument groups leverage global manufacturing and distribution efficiencies, brand recognition across student-to-professional tiers, and broad after‑sales networks.

- Enduring value of craftsmanship and vertical differentiation: boutique makers and premium artisanal brands command outsized reputation capital in orchestral and professional channels—where product provenance and customization matter more than price.

Key category archetypes and strategic implications:

- Global diversified OEMs (scale + channel breadth): Manufacturers with integrated wind portfolios use scale to invest in sustainability, product bundling, and global marketing. These players are well placed to standardize supply‑chain compliance and roll out packaging redesigns that resonate with younger consumers.

- Mass‑market / education specialists: Brands focused on school and beginner instruments prioritize cost efficiency, partnerships with education authorities, and distribution through institutional channels and mass retailers.

- High‑end artisans and boutique houses: Handcrafted makers sustain premium margins and brand equity through limited production, custom options, and close orchestral relationships; these firms benefit from “place” recognition (e.g., craft clusters or city reputations) and museum/curatorial partnerships.

Recent industry moves underscore these dynamics. Leading manufacturers have introduced sustainability initiatives for entry‑level packaging, while cultural institutions are staging exhibitions that raise product visibility and create cross‑over marketing opportunities. Simultaneously, tariffs introduced in 2025 have raised import costs and contributed to measurable declines in export volumes in affected markets—an operational reality that should inform sourcing and pricing decisions in 2026.

Strategic implications and recommended 2026 playbook

We translate our findings into five immediate priorities for 2026 decision cycles—each specified with a recommended action and an executive-level KPI to track.

- Shield margin through sourcing redesign

Action: Implement a three-tier sourcing strategy—retain critical high-value manufacturing domestically or in low‑tariff jurisdictions; develop local final‑assembly hubs in priority markets; and secure dual suppliers for key components. KPI: Percentage of units assembled within target tariff-exempt jurisdictions (target: 25–40% in first 12 months).

- Monetize education demand with scalable service models

Action: Launch pilot instrument-as-a-service offers for school systems that bundle instrument rental, periodic maintenance, and teacher training; price to recover acquisition costs within 24 months. KPI: ARPU (annualized) per institutional account and uptake rate among targeted districts.

- Differentiate premium through provenance and experience

Action: Invest in bespoke product lines and artist partnerships; leverage cultural activations (museum exhibitions, masterclasses) to maintain premium pricing. KPI: Premium product ASP growth and share of wholesale to direct experiential sales.

- Embed sustainability as a commercial lever

Action: Standardize eco‑packaging for entry and intermediate lines, and publish measurable lifecycle targets; use sustainability labeling to secure institutional procurement mandates. KPI: Share of units shipped in certified sustainable packaging and procurement wins with sustainability criteria.

- Use targeted M&A to fill strategic gaps

Action: Prioritize bolt‑ons that add local manufacturing, digital learning platforms, or refurbishment/refurb finance capabilities. Run a 90‑day diligence sprint focused on supply‑chain synergies and customer overlap. KPI: Time to first integration synergies and projected payback on acquisition capital.

Risk matrix — what keeps CFOs awake

- Tariff volatility: Sudden rate changes can erode margin; hedging through local assembly and tariff classification reviews is a short‑term imperative.

- Education funding cycles: Public budget timing creates lumpiness—diversify balance between institutional and consumer channels to smooth revenue.

- Craftsman supply bottlenecks: Premium handmade producers face labor scarcity; succession planning and apprenticeship programs are strategic needs.

- Reputational risk around sustainability: Younger buyers prize ethical sourcing; failure to demonstrate progress can depress brand value, especially in student segments.

How to use the full report

This press summary highlights the decisive insights executives need to shape 2026 strategy. The full PW Consulting Flutes Instrument Market report includes the underlying datasets, segmentation tables, company profiles, and downloadable scenario models required to operationalize the recommendations above. We intentionally limit granular segmentation detail in this release to preserve the integrity of our proprietary market model—subscribers and clients can access the complete breakdowns, regional scenarios, and firm‑level benchmarking on our site.

Final note for boards and investors

Market growth is steady and predictable at the aggregate level, but value creation in 2026 will be driven by strategic execution: mitigating trade cost exposure, converting institutional education spending into recurring revenue, and defending premium positions through craft and experience. For boards, the practical questions are succinct: where will we source our next 30–40% of capacity, how will we convert school contracts into recurring revenue, and which niche producers, if acquired, would meaningfully accelerate market access or reduce tariff sensitivity? Our report equips you to answer those questions with the data and the scenario options required for confident decision‑making.

To request the full dataset, company scorecards, and the interactive forecast model, please visit the PW Consulting report page or contact our research team. The 2026 window for structural advantage is narrow; the organizations that align sourcing, channel, and product strategy now will capture the next cycle of growth.

For detailed analysis of this topic, please visit the official page:Flutes Instrument Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com