Moving Millions – Growth Dynamics in the Railway Traction Motor Market

Other |

2026-06-11 09:13:44

PW Consulting’s Como Catalyst Market report establishes a clear, actionable view on the hydrotreating catalyst landscape for 2026 decision-makers. Using 2025 as the base year, the market reached approximately USD 648.5 Million (USD Million unit basis) after a steady recovery from 2020, and PW’s scenario-led forecast projects continued expansion through 2032 to roughly USD 842 Million, driven by a compound annual growth rate of 3.8% over the 2026–2032 forecast window. These headline metrics underline a market that is neither nascent nor saturated: it is sufficiently mature to reward operational excellence, yet dynamic enough to create outsized opportunities for suppliers and refiners that adapt to feedstock shifts, regulatory tightening and raw-material volatility.

Como Catalyst Market

Regulatory momentum and evolving feedstocks: Stricter sulfur limits in mobility fuels, together with the rise of renewable diesel and variable-quality VGO feedstocks, are altering hydrotreating unit duty cycles and catalyst selection criteria. For many operators the balance between deep desulfurization performance, hydrogen consumption and cycle life is now a primary commercial lever.

Como Catalyst Market

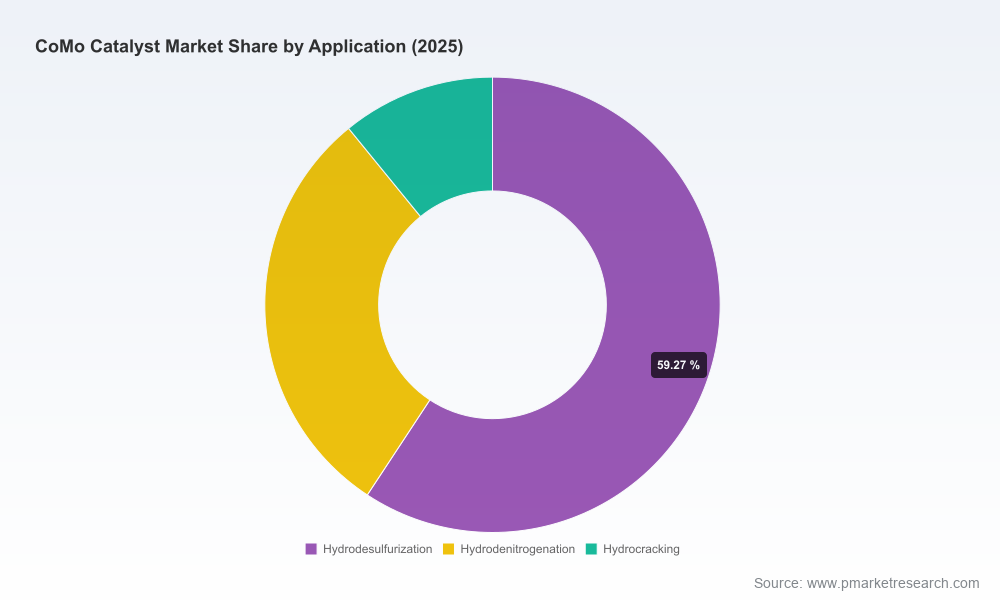

Technical differentiation: CoMo formulations retain a distinct role in low-to-medium pressure hydrodesulfurization because of favorable selectivity characteristics vis-à-vis NiMo in certain duty profiles. However, their performance remains sensitive to process variables such as carbon monoxide partial pressure — a nuance that shifts technical preference in integrated refinery configurations.

Como Catalyst Market

Supply-side pressure points: Recent raw-material dislocations (notably cobalt supply restrictions and molybdenum price variability) have moved procurement from a tactical to a strategic function. Manufacturers and buyers that lock-in resilient sourcing and circular material flows will materially reduce cost volatility over the planning horizon.

The report is structured to convert market intelligence into executable actions. Key deliverables include:

Robust top-down sizing and a granular, scenario-based forecast (2026–2032) with sensitivity analyses for feedstock mix, hydrogen cost and regulatory tightening.

Segmentation studies across region, catalyst type and application with decision-ready implications for procurement and technology selection (note: detailed split tables and model workbooks are reserved for the full report).

Vendor benchmarking and a scorecard framework that combines technical performance, supply-chain resilience and commercial terms—designed for rapid incorporation into RFPs and supplier negotiations.

Supply-chain risk assessment emphasizing raw-material concentration, recycling levers, and hedging strategies tied to cobalt and molybdenum market dynamics.

Practical toolkits: an operational checklist for hydrotreating unit audits, an ROI model for catalyst changeouts under alternate feedstock scenarios, and a procurement playbook for long-term offtake and consignment models.

The market shows measurable concentration at the top: the three- and five-firm concentration metrics indicate that a set of established technology providers capture a material share of demand. That structure creates predictability around product roadmaps but also raises the stakes for mid-market and regional players to claim differentiated niches.

Haldor Topsoe (Topsoe) — Topsoe is doubling down on high-activity CoMo formulations aimed at ultra-low sulfur diesel and renewable diesel pre-treatment. Recent moves include a mid-2025 product introduction that extended cycle life and an early-2026 capacity expansion to support rising demand in sustainable fuel sectors. For refinery clients, Topsoe’s roadmap signals improved availability but also a premium on lead-time planning for advanced formulations.

BASF — With a long-standing portfolio of CoMo and NiMo solutions, BASF’s strength remains in trusted, application-proven catalysts for complex feedstocks such as pygas and coke-oven derived streams. Their value proposition centers on predictable performance and full-service technical support, which is attractive to large integrated refiners prioritizing uptime.

Axens — Axens focuses on middle-distillate ultra-deep HDS and VGO hydrotreating with a family of competitive CoMo products. Their approach bundles catalyst supply with process licensing and operational tuning—an important option for refiners seeking step-change performance without incurring integration risk.

Shell Catalysts & Technologies (Criterion) — Shell’s catalyst arm offers CoMo and NiMo lines that target distillate hydrotreating and low-pressure HDS niches. Their integration with Shell’s broader technical base and testing facilities supports data-driven selection and lifecycle management strategies, useful for complex revamp projects.

Kuwait Catalyst Company (KCC) — KCC supplies regionally focused, high-performance CoMo catalysts and has relevance for refiners operating in feedstock profiles typical to the Middle East. Their local presence shortens supply chains and reduces logistics risk for immediate turnaround windows.

Ketjen (former Albemarle refining catalysts) — Following corporate restructuring and ownership changes in 2025–2026, Ketjen’s refining catalysts business is repositioning. Market participants should watch product continuity, service agreements and potential shifts in commercial terms as new ownership integrates operations.

Commodity shifts in 2025–2026 have altered the calculus for catalyst manufacturers and users alike. A temporary cobalt export interruption and subsequent quota regime reshaped the cobalt supply picture, producing price spikes and tighter availability. Molybdenum has experienced short-term variability that, while smaller in amplitude, compounds procurement complexity when paired with cobalt exposure.

For 2026 strategy we recommend a three-tiered mitigation approach:

Supplier diversification and secured long-term contracts (including quota-aligned volumes) to reduce single-source exposure.

Investment in secondary sourcing and recycling: reclaim and recycle programmes for spent catalysts materially deflate effective raw-material intensity and shield buyers from spot-market shocks.

Technical adaptation: where process duty permits, evaluate low-cobalt or alternate-support formulations, and calibrate operating envelopes to minimize performance loss while reducing cobalt intensity.

Refiners: initiate a feedstock-risk heat map for all hydrotreating units and model catalyst life under at least three scenarios (base, high-VGO, and hydrogen-constrained). Use the PW ROI template to quantify net margin impact from catalyst swaps and unit derates.

Catalyst suppliers: accelerate product qualification cycles for lower-cobalt formulations and invest in regional service hubs to shorten lead times. Where possible, offer outcome-based contracts that align commercial terms with demonstrated cycle life.

Procurement teams: renegotiate contracts to include flexible quantity bands and price corridors linked to raw-material indices; implement inventory strategies that balance working capital with outage preparedness.

Investors and M&A teams: target assets that increase vertical control of critical raw materials, or that provide differentiated analytics and digital lifecycle services—both are premium drivers in a concentrated market.

The Como Catalyst Market report is deliberately practical: it combines market-level forecasts with operational tools and vendor scorecards that are immediately actionable in 2026 planning cycles. This release serves as a compact briefing; full access to the report provides the complete segmentation tables, downloadable financial models, step-by-step procurement templates and detailed vendor benchmarking data that underpin the recommendations summarized here.

For companies that treat catalyst strategy as a core element of refinery competitiveness, 2026 is the year to convert insight into inventory, technical and contractual action. The market’s moderate growth, combined with supply-side concentration and raw-material volatility, rewards early movers who pair rigorous scenario planning with pragmatic supply-chain adjustments. PW Consulting’s Como Catalyst Market report delivers both the strategic framing and the operational toolset to make those moves with confidence. For the full segmentation data, vendor scorecards and downloadable playbooks, access the complete report on the Como Catalyst Market portal.

For detailed analysis of this topic, please visit the official page:Como Catalyst Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com