Data Centre Video on Demand Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-26 07:54:41

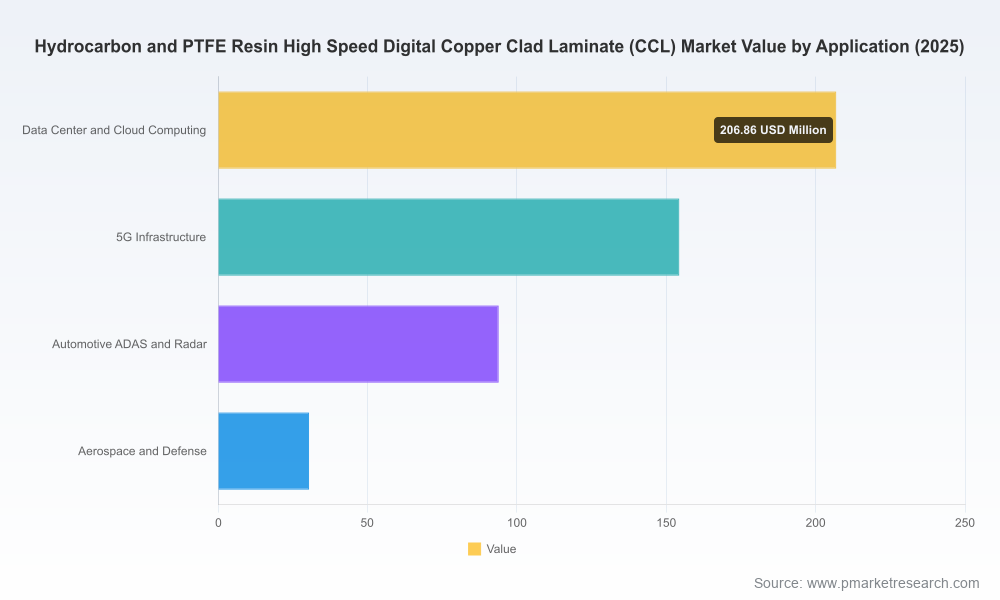

PW Consulting’s new market research briefing on Hydrocarbon and PTFE resin high-speed digital Copper Clad Laminates (CCL) synthesizes market modelling, supplier intelligence, and scenario-based strategy to help executives make high-confidence decisions entering 2026. Our analysis combines a rigorous historical baseline (2020–2025), a detailed 2026 pivot point assessment, and a forward-looking forecast through 2032. The overall market is projected to grow from an estimated USD 485.5 Million in the 2025 base year to approximately USD 898.96 Million by 2032, representing a compound annual growth rate (CAGR) of 9.2% over the forecast period.

Hydrocarbon and PTFE Resin High-Speed Digital Copper Clad Laminate (CCL) Market

2026 is not merely another year on the timeline — it is where technology deployments, raw-material dynamics, and regulatory pressures converge to reshape supplier economics and customer selection criteria across high-speed digital, 5G, datacenter, automotive radar and aerospace segments. Our report treats 2026 as the decision-making horizon: procurement contracts will be renegotiated, capacity expansions will be evaluated for payback under new price regimes, and material selection roadmaps for next‑generation platforms will be finalized.

Hydrocarbon and PTFE Resin High-Speed Digital Copper Clad Laminate (CCL) Market

Clear market momentum: After sustained growth in the early 2020s, our topline forecast shows near-doubling of market size by 2032, reflecting escalating bandwidth requirements, densification of high-frequency infrastructure, and server/network upgrades.

Hydrocarbon and PTFE Resin High-Speed Digital Copper Clad Laminate (CCL) Market

Consolidated supplier base: Market concentration remains meaningful (CR3 ~55.4%; CR5 ~68.2%), making competitive positioning and supply security central to procurement and M&A strategies.

Cost and compliance pressures: Volatility in PTFE and hydrocarbon resin pricing — coupled with developing regulatory scrutiny — will materially affect product cost-to-serve and formulation roadmaps in 2026 and beyond.

PW Consulting’s report is structured to move beyond descriptive industry narrative to actionable inputs executives can operationalize in 2026 planning cycles:

Modular forecasting engine: Granular topline and scenario models (base, downside, upside) that let you test demand, pricing and raw-material shocks and see P&L and margin impacts across alternative go-to-market choices.

Commercial playbooks: Channel and account-level strategies for OEMs, contract manufacturers and CCL producers — including commercial levers for premiumization, volume-based contracts, and risk-sharing clauses tied to resin cost indices.

Supply-chain risk matrix: Supplier tiering and contingency plans keyed to material concentration, geographic risk and production lead times; includes trigger-based actions for inventory, hedging and contract renegotiation.

Product roadmap alignment: Decision frameworks for material selection (PTFE vs. hydrocarbon vs. hybrid systems) that balance electrical performance, manufacturability, cost trajectory and regulatory compliance.

M&A and capacity playbook: Identifies target profiles, accretion/dilution sensitivities and integration risks to guide inorganic expansions or joint ventures.

Our quantitative model ties major growth drivers to measurable market outcomes. Key forces include increasing data center I/O speeds and channel counts, densification of 5G and mmWave deployments, broader adoption of automotive radar/ADAS modules, and sustained defense/aerospace requirements for high-reliability laminates. These end-market demands are amplified by advancements in signaling standards and serial link rates that increase sensitivity to dielectric loss and dimensional stability — attributes where PTFE and advanced hydrocarbon resins play differentiated roles.

Strategically, buyers and producers face a classic trade-off: PTFE-based systems often deliver the lowest loss at the highest cost and supply volatility, whereas modern hydrocarbon systems and ceramic-hybrid designs can offer cost/processing advantages with competitive performance for certain channel requirements. The right architecture choice depends on system-level electrical margins, manufacturing readiness, and the buyer’s tolerance for supplier concentration and regulatory exposure.

The market is shaped by a mix of global specialty-material players and regionally dominant laminate producers. PW Consulting’s competitive benchmarking highlights strategic positioning rather than transactional scorecards:

Rogers Corporation (Chandler, AZ) — recognized for RO4000 hydrocarbon ceramic laminates and PTFE-based XtremeSpeed platforms, Rogers combines broad product breadth with targeted investments in defense and automotive capacity.

AGC Inc. (Tokyo) — offers HF-series hydrocarbon CCLs and PTFE resin systems; AGC’s integrated upstream capabilities provide advantages when high-purity PTFE sourcing and vertical supply stability are priorities.

Taconic (AGC affiliate) — specialization in PTFE-based high-performance dielectrics makes Taconic a key partner where absolute low-loss attributes are critical.

Isola Group — positions on balanced portfolios of hydrocarbon and low-loss materials, leaning on processability and PCB fabricator adoption metrics.

Taiwan Union Technology (TUC) and ITEQ (Taiwan) — strong in high-speed and telecom-focused segments; their proximity to major EMS and PCB manufacturers is a competitive advantage for volume programs.

Shengyi Technology — aggressive capacity expansions underscore China-based capability to serve 5G and data center markets at scale.

Panasonic — MEGTRON series updates and new ultra-low-loss launches signal continued technology-led competition for server-network applications above 112 Gbps.

Recent moves (capacity expansions, product launches) highlight three tactical themes: (1) vertical optimization to secure resin supply and captive volumes, (2) premium product launches to capture server/telecom upgrade cycles, and (3) geographic capacity shifts to be closer to key OEMs and fabricators. The report maps these moves to likely price/margin outcomes and recommended responses for buyers, CMOs and mid‑market suppliers.

2025–2026 has seen pronounced raw-material noise that will reverberate through CCL economics. Notably, PTFE resin pricing diverged by region in late 2025, with U.S. benchmark prices reaching approximately USD 12,500 per metric ton while China prices were materially lower — a reminder of regional arbitrage and logistics playing a decisive role for global purchasers. High-purity PTFE supply remains concentrated among a handful of producers (e.g., Chemours, Daikin, AGC), and the market has exhibited price volatility in the 15–25% range in response to capacity constraints and feedstock shifts.

Hydrocarbon resin pricing also tightened: suppliers implemented price increases (reported up to 11% effective March 2026) driven by operating-cost inflation and feedstock availability. Combined, these movements erode gross margins for unconstrained OEMs and increase the importance of contractual pass‑throughs, shared-savings agreements, and index-linked pricing mechanisms.

Regulatory risk further complicates planning. Proposed EU restrictions on certain PFAS under REACH could materially raise compliance costs, require reformulation timelines, or limit access to specific PTFE grades in some markets. Our regulatory sensitives model quantifies potential cost uplifts and product discontinuation risk under multiple EU/US trajectories — guiding contingency plans for 2026 procurement cycles.

Lock flexible supply arrangements now: For producers and OEMs, establishing multi-tiered supply contracts — combining spot, term and strategic fill — reduces exposure to volatile PTFE and hydrocarbon resin markets. Include formulaic price adjustments tied to transparent indices.

Invest in portfolio segmentation: Differentiate product lines by target performance and cost-to-produce. Position premium PTFE offerings for applications where electrical margin justifies cost, and migrate high-volume, lower‑sensitivity use cases to modern hydrocarbon or hybrid materials.

Embed regulatory monitoring into product roadmaps: Run accelerated qualification studies for PFAS alternatives and maintain dual‑qualified material banks to avoid sudden market exclusions in key jurisdictions.

Use M&A selectively to secure capacity or vertical integration: Players with mid-sized footprints should prioritize targets that either secure high-purity resin access or offer near-market fabrication capacity to shorten lead times.

Commercially, renegotiate service-level agreements to include supply-disruption remedies and co-investment clauses tied to capacity expansions to share risk and upside.

PW Consulting’s deliverables are designed to slot directly into annual planning and strategic review processes. Executives can use our forecast scenarios to stress-test 2026 budgets, run supplier scorecards that incorporate CR3/CR5 concentration impacts, and prioritize capital allocation across R&D, capacity, and M&A. For commercial teams, playbooks and negotiation templates accelerate time-to-deal while reducing margin leakage.

We deliberately refrain from publishing detailed sub-segment tables and granular regional splits in this briefing to protect the report’s proprietary modelling outputs. The full report contains those critical inputs — including unit-cost build-ups, regional demand matrices, application-level growth rates, supplier benchmarking scorecards and a downloadable forecasting model that lets your team run custom scenarios.

For procurement, product, and corporate development leaders preparing plans for 2026, the full PW Consulting report is a practical toolkit: it couples market pathway clarity with execution-level recommendations and commercial instruments you can deploy immediately. To access the comprehensive dataset, modeling workbook and supplier deep-dives that underpin the conclusions summarized here, please visit the report page and request the full brief and accompanying scenario model.

For detailed analysis of this topic, please visit the official page:Hydrocarbon and PTFE Resin High-Speed Digital Copper Clad Laminate (CCL) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com