Fragrance Market Advances with Ethical and Clean Beauty Focus

Other |

2026-02-19 05:30:17

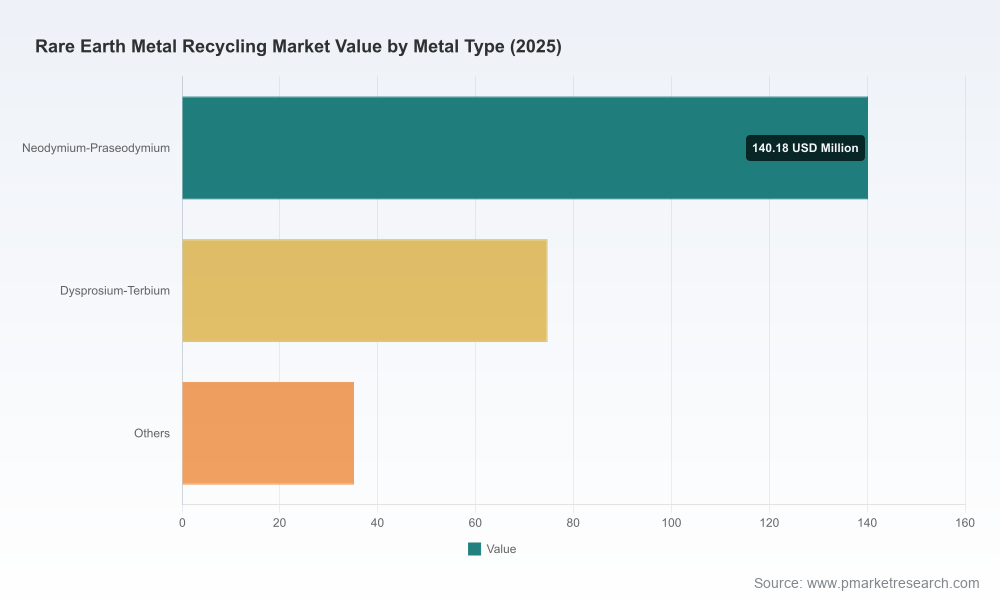

As rare earths migrate from geopolitical afterthought to strategic raw material in advanced electrified systems, corporate leaders face a compressed window to establish industrial-scale recycling positions. PW Consulting’s latest Rare Earth Metal Recycling Market report (base year 2025; historical period 2020–2025; forecast 2026–2032) quantifies this transition and translates it into actionable options for investors, OEMs, recyclers, and policy teams. The market is growing at a sustained double‑digit rate — a 17.5% compound annual growth rate (CAGR) through the forecast period — and moved from roughly USD 110 million (2020) to USD 250 million (2025, revenue unit: Million USD). Our projection shows the market scaling toward three‑quarters of a billion dollars by 2032, underscoring both the commercial upside and the operational complexity that will define winners and losers.

Rare Earth Metal Recycling Market

Expanding market base: Between 2020 and 2025 the industry roughly doubled in size; the forecast period (2026–2032) projects continued acceleration as electrification, wind energy, and high‑end electronics create ever‑larger flows of magnet‑bearing waste and end‑of‑life components.

Rare Earth Metal Recycling Market

Pricing and raw material shock: Spot and alloy prices have become a critical short‑term driver of recycling economics. Notably, NdPr alloy prices surged sharply in early 2026 (c. 138% YTD to approximately USD 126/kg by April 2026), compressing primary supply affordability and materially improving the competitiveness of recycled content streams.

Rare Earth Metal Recycling Market

Policy and finance tailwinds: 2025–2026 saw active industrial policy in several markets — from export controls and licensing actions with extraterritorial implications, to targeted public capital and credit lines intended to on‑shore processing and recycling. These dynamics change project IRRs and de‑risk supply chains for domestic manufacturers and allied producers.

This report is designed as a field manual for strategy and deployment, not an academic exercise. Key practical deliverables include:

Robust market sizing and revenue modeling (base year 2025, forecasts to 2032) with scenario sensitivity for price, feedstock availability, and policy interventions.

Supply chain maps and technology assessment across short‑loop and long‑loop recycling pathways, including hydrometallurgy, pyrometallurgy, hydrogen processing, and chromatographic separation approaches.

CapEx and OpEx benchmarking templates for plant‑level feasibility, including capacity step scales, feedstock conversion efficiencies, and break‑even pricing ranges (delivered as configurable worksheets).

Commercial playbooks — feedstock aggregation strategies, offtake contracting templates, joint‑venture and concession structures, and examples of industrial partnerships tailored to automotive, wind, and electronics value chains.

Regulatory and permitting timeline models, with mapped requirements across major jurisdictions and a risk matrix for export controls, licensing, and technology transfer sensitivities.

Investment due diligence checklists, an M&A target screening framework, and valuation sensitivity for early‑stage recycling ventures versus brownfield expansions.

Environmental and LCA modules to quantify emissions, water use, and circularity benefits — including templates to support recycled‑content claims and procurement negotiations.

The competitive map in 2026 combines diverse entrants: technology innovators, incumbent miners and processors moving downstream, pure recyclers scaling capacity, and vertically integrated manufacturers creating closed‑loop value chains. Market concentration is meaningful but not monopolized — the top three players control a material share of capacity and the top five an even larger portion, creating an environment where strategic partnerships and niche specialization are viable pathways to scale.

Core company archetypes and dynamics we analyze in depth:

Technology pure players (e.g., Cyclic Materials, REEcycle Inc., ReElement Technologies). These firms are focused on process differentiation and rapid scale‑up of recycling campuses and plants. Recent capacity investments and government support signals (including an USD 80 million concessional loan to a U.S. processor in late 2025) have de‑risked certain projects and accelerated investor interest in modular, scalable designs.

Integrated industrials and OEM partners (e.g., MP Materials, Lynas, Neo Performance Materials, Umicore). These players bring scale, downstream manufacturing capability, and market access for recycled magnet powders and oxides. Their strategies typically emphasize closed‑loop integration and securing feedstock via supplier or OEM agreements.

Emerging process innovators (e.g., HyProMag’s hydrogen processing pathway, university‑industry consortia). Short‑loop hydrogen‑based processes and chromatography approaches offer compelling economics for certain scrap streams, and commercialization progress is advancing through newly launched facilities and pilot‑to‑commercial scaling this year.

Regional specialists and niche recyclers (examples across Europe, North America and APAC). These firms often target particular waste streams — HDD magnets, EV traction motors, or industrial permanent magnet scrap — and can command premium margins where logistics and disassembly expertise matter.

Selected 2026 developments underscore strategic inflection points: large campus investments announced by recyclers, siting of a major magnet campus incorporating closed‑loop recycling in Texas, and the launch of world‑leading hydrogen processing facilities in the UK. These illustrate two intersecting themes — capital intensity at scale and the advantage of co‑locating recycling with magnet manufacturing and downstream users.

Feedstock aggregation is a first‑order constraint. Establishing streams of end‑of‑life motors, magnets, and electronics — via take‑back agreements, collection partnerships, or supply‑side acquisitions — will determine utilization rates and project economics. Leaders should prioritize contractual control over feedstock flows ahead of committing large CAPEX.

Technology risk is real but manageable. Selecting the right process mix (short‑loop vs. long‑loop) depends on feedstock characteristics and product spec requirements. Our decision matrices help corporates match plant design to feedstock and offtake profiles to maximize yield without overpaying for unnecessary flexibility.

Policy arbitrage can be monetized. Export controls, domestic financing packages, and procurement incentives are reshaping project returns. Companies that can align projects with government priorities (e.g., defense, critical minerals security, decarbonization) will access concessional capital and faster permitting windows.

Vertical integration vs. specialization is a strategic fork. Integrated magnet manufacturers and miners are investing to capture downstream recycling value; conversely, specialized recyclers can win by offering lower capex footprints and faster time‑to‑market. Our playbook quantifies the tradeoffs using multi‑year cash flow models and strategic option value assessments.

Partnerships beat lone‑wolf strategies in 2026. Joint ventures between recyclers and OEMs, co‑location with magnet plants, and technology licensing can accelerate volume capture and mitigate market concentration risks. The report contains model JV term sheets and partnership governance structures proven in recent transactions.

We present three core scenarios that matter for boardrooms and investment committees: a policy‑accelerated scenario (fast permitting, strong procurement incentives), a market‑driven scenario (sustained high primary prices supporting recycling margins), and a technology‑disruption scenario (rapid cost declines in certain separation technologies). Each scenario includes sensitivity tables for CAPEX, feedstock price, and recovery yield to quantify break‑points for investment.

For corporate strategists: Use the benchmarking modules to stress‑test your existing procurement and sourcing plans, and to size capital allocations to recycling versus primary sourcing.

For investors and PE: Apply the valuation frameworks and M&A target filters to identify acquisition candidates and roll‑up opportunities that can accelerate scale and capture structural premiums.

For policy teams and development banks: Leverage our permitting timelines and socio‑economic impact assessments to design interventions that maximize recycled yield and public value while minimizing market distortion.

Rare earth recycling is no longer an esoteric niche. Market growth, price volatility for key alloys, active industrial policy, and rapid technology maturation combine to create a multi‑year window for strategic decisive action. Our report gives you the data‑driven market map, the operational playbooks, and the competitive intelligence needed to make those choices in 2026 — while purposely leaving granular segment tables and downloadable financial models behind a single access point to enable bespoke client engagements. For decision‑makers preparing capital plans, joint ventures, or procurement mandates this year, the choices made now will determine the economics and market share trajectories for the remainder of the decade.

To obtain the complete report — including the full scenario models, plant‑level financial templates, and the segmented datasets that inform our forecasts — please visit PW Consulting’s Rare Earth Metal Recycling Market page or contact our advisory team for a brief walkthrough tailored to your strategic questions.

For detailed analysis of this topic, please visit the official page:Rare Earth Metal Recycling Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com