Mold Flux for Continuous Casting Market 2026: Strategic Imperatives for Steelmakers and Suppliers

PW Consulting is pleased to announce the release of our latest industry study, "Mold Flux for Continuous Casting Market: Strategic Outlook 2026–2032." Built on a five-year historical base (2020–2025) and a seven-year forecast horizon (2026–2032), this report synthesizes commercial, metallurgical, regulatory, and supply-chain intelligence into a single playbook designed to inform boardroom decisions in 2026. Below we present an executive-grade preview of the report's strategic value—demonstrating our analytical depth while intentionally withholding the granular splits that are available in the full publication.

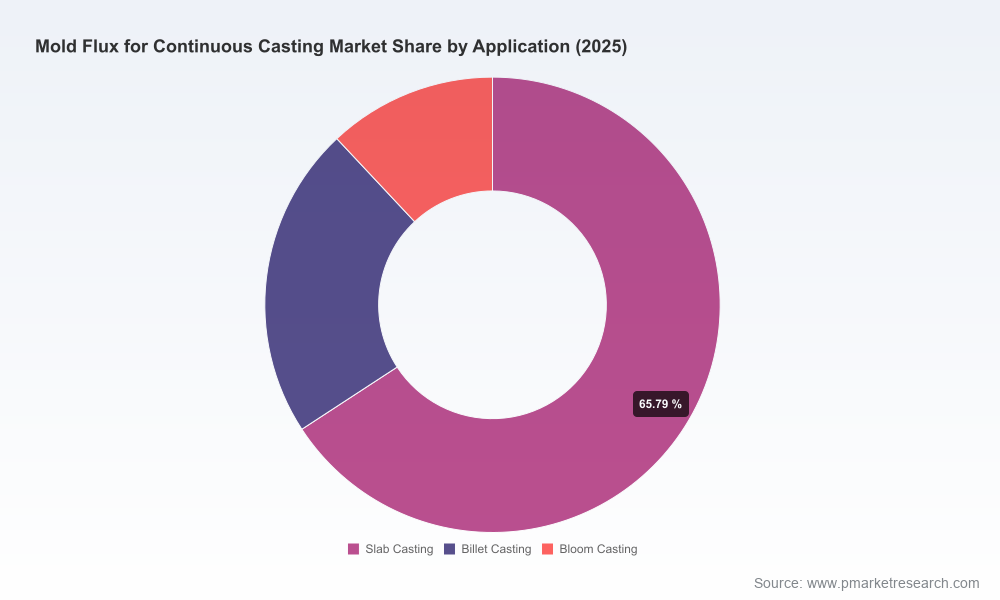

Mold Flux For Continuous Casting Market

Market Snapshot: Size, Trajectory and Concentration

The global market for mold flux used in continuous casting totaled approximately USD 564.3 million in 2025. Our projection model anticipates a steady expansion through the forecast period, driven by modest growth in casthouse throughput, iterative product innovation toward low-emission chemistries, and targeted capacity additions in high-growth manufacturing corridors. The market is expected to grow at a compound annual growth rate (CAGR) of roughly 3.85% over the forecast window, reaching a projected market size of about USD 735.1 million by 2032.

Mold Flux For Continuous Casting Market

Market structure analysis shows a moderately consolidated landscape: the top three firms account for a meaningful share of industry revenues, while the top five firms extend that influence further—indicators of both technical barriers to entry and the value of scale in procurement, spray-drying, and global technical support. The report quantifies this concentration and maps competitive positionings to inform strategic options for entrants and incumbents alike.

Mold Flux For Continuous Casting Market

What the Report Contains — Practical, Executable Intelligence

- Commercial Forecasting: Annualized market-sizing and scenario-driven forecasts through 2032, segmented by product typology, application family, and high-level geographic regions. (Note: detailed split tables are available in the full report.)

- Demand Drivers & Sensitivities: A causal model linking steel grades, casting yield improvements, thin-slab initiatives, and environmental regulation to mold flux demand. The model allows sensitivity testing for pricing shocks, raw-material scarcity, and demand-side shifts.

- Supply-Chain Diagnostics: End-to-end mapping of upstream mineral inputs (e.g., silica, lime, fluorite alternatives), midstream processing (grinding, spray drying, pre-fusing), and logistics bottlenecks—highlighting single-source exposures and mitigation options.

- Competitive Intelligence: Strategic profiles, capability audits, and product-portfolio analysis of the leading global and regional suppliers—paired with an M&A heatmap identifying likely consolidation targets and strategic acquirers.

- Technology & Regulatory Tracker: Evaluation of low-fluorine and fluorine-free chemistries, development pathways for carbon-free powders, and evolving occupational and emissions standards that are reshaping R&D priorities.

- Action Playbooks: Turn-key strategic recommendations for producers, mills, and investors—covering commercial negotiation levers, plant investment sizing, partnership archetypes, and R&D roadmaps for 2026 implementation.

Competitive Landscape — Who Matters and Why

The sector combines a mix of global engineering-driven suppliers and regional specialists. Large engineering-materials firms bring integrated service propositions—technical support, tailored formulations, and multi-site sourcing—while smaller, specialist producers offer rapid formulation innovation and craft-scale quality. Recent corporate developments have underlined two strategic themes: consolidation to gain technology and regional reach, and capacity expansion in proximate steel clusters.

- Nippon Steel Metal Products (NITTEX Division) remains a technical anchor with deep integration into steelmaking operations and an installed base that provides defensible commercial relationships based on decades of metallurgical know-how.

- Shinagawa Refractories has accelerated its globalization strategy via acquisition activity to integrate high-quality niche manufacturers into a broader platform—an approach that strengthens product breadth and localized service footprints.

- Vesuvius continues to leverage its metallurgical product line breadth and recent plant investments to secure supply to integrated steel projects and OEMs requiring tailored solutions.

- Regional players and specialist manufacturers—from established refractories groups to craft producers—play a critical role in serving short lead-time requirements and specialized steel grades.

Our competitive analysis includes capability matrices, channel assessments, and an M&A likelihood scoring model to help decision-makers prioritize partners and targets based on strategic fit (technology, customer access, geographic coverage) rather than headline valuations alone.

Recent Strategic Moves — Signals to Watch in 2026

- Acquisitions that stitch niche technical capabilities into global platforms are reshaping supplier dynamics—evidenced by a majority stake purchase in a U.S. craft mold-flux manufacturer in early 2026 that combines innovation speed with global distribution reach.

- Plant inaugurations and hub investments in India and other proximate manufacturing clusters indicate a pivot towards onshore production to serve large steel hubs and reduce logistics intensity.

- Capacity expansion announcements tied to refractory-and-flux hubs emphasize a longer-term view on demand durability, especially where steelmakers are upgrading casting productivity.

Technology & Regulatory Dynamics — Product Evolution is Accelerating

Product innovation is the single largest near-term differentiator. Two linked trajectories are reshaping supplier roadmaps: a shift away from high-fluorine chemistries toward reduced- or fluorine-free systems using alternatives such as B2O3, TiO2 and Li2O; and the development of carbon-free powders to support ultra-low-carbon steelmaking. These transitions are driven by equipment-corrosion constraints, workplace safety standards, and emissions regulations. Concurrently, raw-material volatility for traditional inputs (e.g., fluorite) is motivating formula diversification and circular-material experiments—opportunities that the report evaluates both technically and commercially.

Strategic Recommendations for 2026 Decision-Making

For 2026, the following prioritized actions translate the report's findings into executable steps for manufacturers, steelmakers, investors, and procurement teams.

- Audit Supply Exposure: Immediately map single-source dependencies for critical mineral inputs and high-complexity processing steps (spray drying and pre-fusing). Establish dual-sourcing contracts or strategic stock buffers for nodes with high lead-time sensitivity.

- Pursue Focused M&A and JV Activity: For suppliers seeking scale, target acquisitions that add either a unique chemistry (e.g., low-fluorine expertise) or a footprint in a high-growth steel region. For steelmakers, selective equity stakes in specialist flux makers can secure priority access to bespoke formulations.

- Accelerate Formulation R&D: Allocate R&D capital to low-emission formulations and to validate performance parity under lifecycle cost assumptions. Fast-track trials by co-funding pilot campaigns with leading casthouses to reduce adoption friction.

- Optimize Plant Siting & Logistics: Re-evaluate production location strategies to be nearer to major steel clusters to lower freight, improve responsiveness, and reduce carbon footprint—especially for spray-dried and pre-fused products with higher logistics sensitivity.

- Commercial & Pricing Playbooks: Structure contracts that marry volume certainty with flexibility clauses for formula adjustments as regulations evolve. Consider performance-tied pricing where suppliers co-share the risk of new chemistries through trial windows.

- Governance & Compliance: Implement forward-looking compliance roadmaps for emerging occupational and emissions limits. Use independent testing protocols to demonstrate performance and regulatory alignment to downstream partners and authorities.

- Capability Partnerships: For mills lacking in-house flux expertise, form technical alliances with suppliers for integrated process control services—bundling formulation with casting parameter optimization to capture joint value.

How PW Consulting Supports Your 2026 Agenda

Our full report includes the data tables, supplier scorecards, sensitivity models, and executive playbooks required to operationalize the recommendations above. Clients receive access to a scenario modeling tool that allows rapid re-stressing of the forecast under alternative assumptions for steel demand, raw-material price paths, and regulatory timelines—useful for 2026 capital planning, procurement hedging, and R&D budgeting.

To preserve the strategic advantage of our subscribers, this preview intentionally omits the granular regional, product-type and application breakdowns that commercial teams and corporate strategy functions rely on for negotiation and investment decisions. The full market study contains those detailed splits, along with downloadable data appendices and supplier contact matrices.

Next Steps

- Procurement and strategy teams planning 2026 budgets should prioritize immediate access to the report to lock in supplier negotiation frameworks and plant-capex scenarios.

- R&D leaders should leverage the technology tracker and pilot protocols in the full study to accelerate low-fluorine and carbon-free proof-of-concept timelines.

- Private equity and corporate development groups can use our M&A heatmap to identify high-conviction targets for bolt-on acquisitions that de-risk technology transitions.

PW Consulting’s "Mold Flux for Continuous Casting Market: Strategic Outlook 2026–2032" delivers the actionable intelligence required to make defensible, high-value choices in 2026. For access to the full dataset, segmentation tables, and proprietary scenario tool, please visit our report landing page or contact our Industrial Materials practice team for a briefing and demo.

For detailed analysis of this topic, please visit the official page:Mold Flux For Continuous Casting Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com