How to Leverage Your Mutual Fund Investments for Quick Liquidity

Other |

2026-04-25 12:42:29

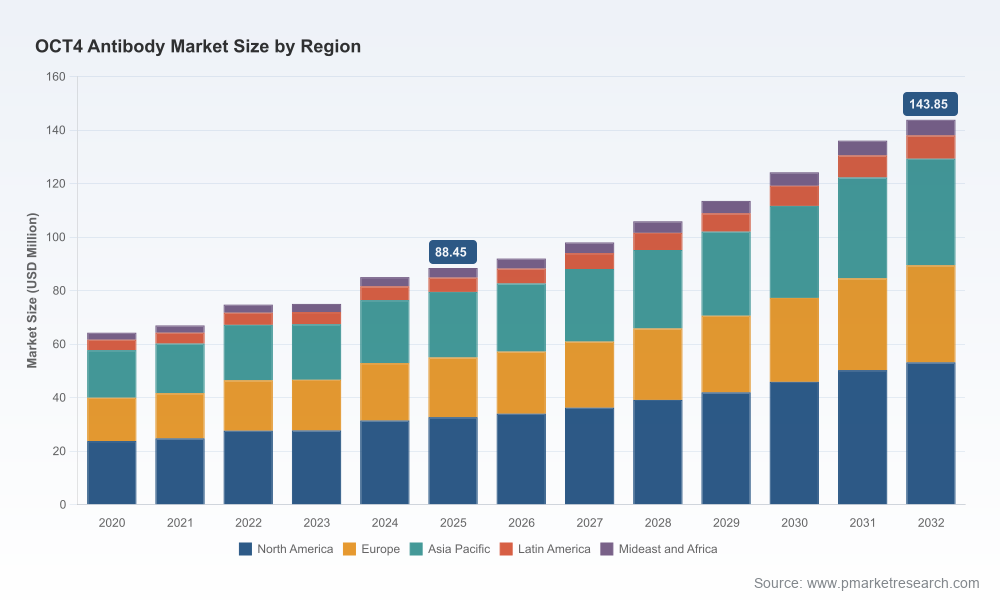

PW Consulting’s Oct-4 Antibody Market — Oct-4 Antibody Market (Base year: 2025; Forecast: 2026–2032) — anticipates a steady expansion driven by sustained demand in stem cell science, oncology research, and drug discovery. Our analysis finds the segment growing at a compound annual growth rate (CAGR) of 7.19% over the forecast horizon, with the total market moving from a documented 2025 baseline to a substantially larger opportunity by 2032. This briefing summarizes the strategic implications we expect to matter most to corporate leaders in 2026 while preserving the detailed segment-level intelligence in the full report that is available from PW Consulting.

Oct-4 Antibody Market

Strategic continuity: Oct-4 remains a core pluripotency marker with ongoing relevance across embryonic stem cell, induced pluripotent stem cell (iPSC) workflows, and multiple oncology research substreams. Demand is being sustained by both basic research and translational programs that rely on robust, validated OCT4 reagents.

Oct-4 Antibody Market

Product differentiation opportunity: Advances in antibody engineering (recombinant clones, conjugates, ChIP-grade polyclonals) are shifting buyer expectations from simple availability toward validated performance claims and application-specific documentation.

Oct-4 Antibody Market

Commercial leverage: Distributed purchasing by academic labs, contract research organizations (CROs), and biopharma creates repeatable revenue pathways for vendors that demonstrate reproducible lot-to-lot performance, clear RUO labeling, and flexible format availability.

Robust market sizing and trend model — a primary/secondary data-driven time series from 2020 through 2032, with scenario-based forecasts and sensitivity to key adoption vectors. The model supports what-if planning and M&A valuation work.

Go-to-market playbook — prioritized routes-to-market by buyer cohort (academic, translational, CROs, commercial R&D), SKU and format roadmaps, channel optimization guidance, and pricing strategy frameworks suitable for 2026 procurement dynamics.

Product performance matrix — independent cross-application validation benchmarking (WB, ICC/IF, IHC, Flow Cytometry, ChIP), recommended claims language, and best-practice validation datasets for vendors to adopt to accelerate conversion.

Supply chain & manufacturing checklist — capacity mapping, quality control gating, and contingency planning for reagent sourcing and conjugation services; a practical section designed to reduce time-to-market for new OCT4 SKUs.

Competitive scorecards — comparative positioning on product breadth, validation depth, commercial reach, and academic citation performance to support benchmarking, partnership targeting, and white-space identification.

Regulatory & risk advisory — clear exposition of RUO labeling constraints, substitution/discontinuation risks for legacy SKUs, and communications strategies to mitigate buyer uncertainty while avoiding impermissible clinical claims.

Deal & partnership playbook — M&A screening criteria, bolt-on acquisition archetypes, and JV partnership templates for market entrants or incumbents seeking to accelerate capability in OCT4 reagents and adjacent pluripotency markers.

The Oct-4 antibody market is populated by a mix of large life-science platforms and specialized reagent houses. Leaders combine breadth of catalog, validated application claims, and strong academic visibility. Key competitor archetypes we analyze in depth include:

Large-platform vendors (example profiles: Thermo Fisher Scientific / Invitrogen, Abcam, Sigma-Aldrich/Merck) — leverage global distribution, broad catalog integration, and standardized supply chains. Strategic advantage: rapid fulfillment and extensive conjugate options. Strategic vulnerability: slower product iteration relative to specialist producers.

Quality-focused reagent specialists (example profiles: Cell Signaling Technology, R&D Systems / Novus Biologicals, Bio-Techne) — emphasize deep validation, high citation traction in stem cell literature, and curated technical support. Strategic advantage: credibility for demanding applications (e.g., ChIP, IHC-P). Strategic vulnerability: narrower SKU breadth compared to platform players.

Niche and flow-specialized suppliers (example profiles: BioLegend, STEMCELL Technologies, Diagenode) — provide application-specific conjugates and ChIP-grade products that serve targeted workflows. Strategic advantage: high conversion in specific buyer segments. Strategic vulnerability: limited cross-application reach.

Regional and cost-competitive providers (example profiles: Proteintech, GeneTex, CUSABIO) — offer validated clones across species reactivities with cost advantages for routine assays. Strategic advantage: price-sensitive procurement channels. Strategic vulnerability: variability in validation depth and brand perception.

Recent product movements underscore tactical plays companies are making to capture incremental market share: updated IHC-P listings and promoted monoclonal clones, broader publication-quality ChIP-grade polyclonal offerings with batch-specific validation, and refreshed monoclonal listings positioned specifically for pluripotency detection. These product-level adjustments reflect a market where validation data and documentation are primary differentiation tools.

RUO status is universal for commercial Oct-4 antibodies; vendors must maintain explicit product disclaimers and avoid clinical or diagnostic claims. This constraint shapes claims language, marketing collateral, and the permissible scope of co-development agreements.

Manufacturers face reputational risk if legacy SKUs are quietly discontinued without migration paths; transparent SKU rationalization and validated replacement strategies mitigate customer churn.

Expectation management: buyers increasingly request lot-specific validation data and traceability for high-impact studies; vendors that provide batch-level performance evidence gain procurement advantage.

Prioritize validated, application-specific SKUs: Invest in recombinant monoclonal clones and ChIP-grade polyclonals that include verifiable validation datasets. A documented validation package reduces buyer friction in translational programs.

Expand conjugate and format breadth selectively: Focus on high-frequency formats in flow cytometry and ICC/IF, while maintaining a curated IHC-P and ChIP portfolio — avoid unfocused SKU proliferation that dilutes QC resources.

Operationalize lot-level transparency: Implement batch tracking and publish batch-specific validation where feasible. This is a low-cost capability that materially increases conversion among translational buyers.

Strengthen academic and citation networks: Sponsor reproducibility studies, engage with high-impact labs for co-validation, and publish technical notes to elevate perceived credibility and accelerate adoption.

Adopt a disciplined SKU migration playbook: When discontinuing legacy clones, provide validated replacements and clear technical comparators to minimize switching resistance and preserve long-tail revenue.

Evaluate bolt-on M&A and strategic partnerships: Target small, high-quality vendors with specialized validation expertise or conjugation/manufacturing capacity to accelerate time-to-market for premium OCT4 offerings.

Optimize pricing by channel segment: Use tailored pricing and service bundles for academic, CRO, and industry customers; consider subscription/consumable models for high-volume buyers.

Plan for supply resilience: Secure critical raw materials for conjugation and consider dual-sourcing for high-value SKUs to reduce risk of unplanned discontinuations.

Short-term (Q1–Q2 2026): finalize SKU rationalization, deploy batch-level validation templates, and launch at least one recombinant or ChIP-grade flagship SKU with consolidated documentation.

Mid-term (H2 2026): secure strategic academic validations and a CRO partnership to accelerate adoption; establish regional distribution agreements in priority markets.

Longer-term (2027 planning): evaluate acquisition targets and scale manufacturing improvements based on demand curves captured in our forecast model.

Ongoing KPIs: conversion rate by application (WB, ICC/IF, Flow, IHC, ChIP), repeat order frequency, SKU uptime/discontinuation rate, and citation velocity in peer-reviewed literature.

This briefing encapsulates the strategic air cover you need to make immediate 2026 decisions: where to invest, which validation claims will buy you market resilience, and how to align product, manufacturing and commercial moves to a market growing at an approximate mid-single-digit CAGR. The full Oct-4 Antibody Market report contains the granular intelligence required to operationalize these recommendations — detailed tables, per-application demand drivers, consolidated competitor scorecards, and downloadable data models that support valuation, M&A screening, and commercial planning.

For a direct briefing, tailored scenario modeling, or access to the full dataset and company scorecards, contact PW Consulting. Our team will walk through the report’s model and customize recommendations to your portfolio and strategic objectives for 2026.

For detailed analysis of this topic, please visit the official page:Oct-4 Antibody Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com