FGFR Inhibitor Drug Market Insights and Growth Trends

Other |

2026-03-16 05:49:28

PW Consulting’s latest market study on Low Powered Electric Motorcycles and Scooters establishes a forward-looking framework for executive decision-making in 2026. Using 2025 as the study base year and projecting through 2032, the report models a market that expands from USD 27,300 million in 2025 to approximately USD 60,920 million by 2032 — a compound annual growth rate (CAGR) of 12.15%. This release is a strategic preview: we surface high-confidence, actionable conclusions while intentionally reserving detailed segment and regional breakdowns for subscribers to the full report.

Low Powered Electric Motorcycle And Scooter Market

The sector is entering a phase where scale economies, product differentiation, and regulatory alignment will determine winners. While aggregate demand continues to accelerate (12.15% CAGR through 2032), the competitive environment remains neither a monopoly nor atomized — top firms account for a meaningful but not overwhelming share of global sales, leaving room for aggressive challengers and regional champions. For 2026, the question for management teams is not whether the market will grow, but how to translate volume growth into durable margin and share advantages before commoditization intensifies.

Low Powered Electric Motorcycle And Scooter Market

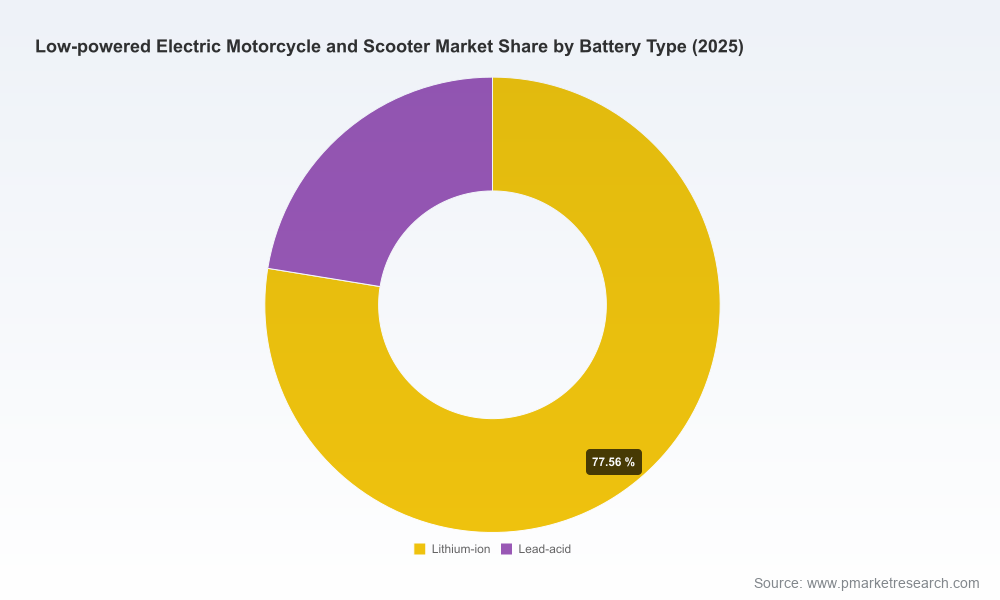

Downward pressure on battery costs. Lithium-ion pack prices declined materially in 2024 and continued into 2025, driven by a combination of low critical mineral prices and capacity oversupply in major supply hubs. That structural price easing opens near-term margin and affordability opportunities, but it also accelerates product parity among mass-market offerings.

Low Powered Electric Motorcycle And Scooter Market

Regulatory tightening around safety and battery systems. Global regulators are focusing on battery safety, vehicle classification, and EV-specific standards — including mandates based on established frameworks such as national FMVSS equivalents and UL testing outlines for vehicle electrical systems. Manufacturers that invest early in certification engineering and compliance pathways will shorten time-to-market in major markets in 2026 and avoid costly recalls or market access delays.

Urban mobility and commercial demand coexist. The market continues to be driven by personal urban commuting use-cases, with last-mile commercial applications growing faster in select dense urban corridors. This duality rewards modular product platforms that can be adapted by powertrain, battery configuration, telematics, and load-carrying packages rather than one-off models.

Technology convergence and ecosystem plays. Connectivity, battery-swapping ecosystems, and integrated service models (finance, insurance, charging/swapping) are shifting value capture from hardware alone to platform-enabled recurring revenue. Players that control software and backend services can extract superior lifetime value even as unit hardware margins compress.

The marketplace is populated by a mix of legacy two‑wheeler OEMs, large-volume Chinese manufacturers focused on affordability, and a set of innovative challengers prioritizing software and ecosystems. Market concentration metrics indicate that the top three and top five vendors control a noticeable share of sales, but not enough to prevent rapid disruption by well-capitalized entrants or regional leaders pursuing differentiated strategies.

Large-volume manufacturers (e.g., major China-based OEMs) retain cost and distribution advantages for entry-level models. Their scale and channel depth will continue to pressure margins in the lower end of the market, especially in price-sensitive regions.

Smart, connected-vehicle specialists are monetizing software, telematics, and battery-swapping strategies. Companies that couple hardware with digital services are creating defensible recurring revenue streams and higher VOMO (value of mobility) per customer.

Traditional OEMs and mobility incumbents are selectively entering or expanding in the segment, bringing brand equity and dealer networks — but they must retrofit manufacturing and software capability to compete on a global scale.

Recent product and strategic highlights illustrate these dynamics. Notably, an established performance-oriented manufacturer revealed a new LS1 scooter as part of its 2026 lineup, signaling intent to compete in accessible urban segments. Another large producer convened a strategic summit to highlight flagship full-size scooters featuring third-party electric drivetrain partnerships and removable lithium-ion batteries — a reminder that collaboration across the value chain (motors, BMS, suppliers) is now table stakes.

Rebalance portfolios toward modular platforms. Prioritize architectures that allow quick reconfiguration across power, range, and payload so engineering and CAPEX are levered across multiple market segments and customers.

Lock in battery and BMS options with layered risk controls. With battery pack prices falling, secure multi-sourced supply agreements that include price collars, quality SLAs, and second-life pathways to manage warranty and residual-value risk.

Operationalize regulatory-first product development. Embed compliance engineers in platform development teams and map certification timelines to product roadmaps to prevent market-entry delays in regulated markets.

Monetize software and services. Introduce subscription-based telematics, predictive maintenance, and battery-as-a-service pilots tied to specific vehicle cohorts to boost lifetime margins.

Forge strategic partnerships and selective M&A. Consider bolt-on acquisitions to gain software capabilities, localized manufacturing capacity, or proprietary battery-swap infrastructure rather than pursuing capital-heavy greenfield expansion.

Supply chain volatility. Even with current oversupply in some battery components, geopolitical or demand shocks could reintroduce raw material price spikes or allocation constraints. Scenario planning should test margin sensitivity across a range of battery-cost outcomes.

Regulatory fragmentation. Differing safety and classification regimes across major markets create complexity for a single global platform. Localized homologation costs can erode expected synergies from global scale.

Competitive commoditization. Unit-level price competition among high-volume manufacturers could depress ASPs, making software and services the pivotal margin lever.

Technology obsolescence. Rapid shifts in battery chemistries, motor topologies, or charging/swapping standards could render some platform investments suboptimal within a few years.

Our full report is organized to support immediate strategy, commercial planning, and investment decision-making for 2026 and beyond. Key deliverables include:

Proprietary demand models and scenario-driven forecasts for 2026–2032 (base year 2025), including sensitivity analyses for battery-cost paths and regulatory outcomes.

Competitive benchmarking and capability scorecards for manufacturers, suppliers, and ecosystem players; identification of realistic M&A and partnership targets by capability gap.

Go-to-market playbooks for premium, mass, and commercial (last-mile) segments — covering pricing, channel design, and aftersales economics.

Supply-chain and procurement risk maps with a focus on critical minerals, component dual-sourcing strategies, and battery end-of-life solutions.

Regulatory and certification navigator tailored to priority markets, integrating relevant safety frameworks and recommended engineering checkpoints to accelerate market access.

CapEx and manufacturing scale models that quantify the trade-offs between greenfield, brownfield, and contract manufacturing strategies under multiple demand scenarios.

To honor our “trailer” principle, this preview surfaces the strategic conclusions but withholds detailed regional and application-level splits, price points, and firm-level revenue allocations. These granular data, model inputs, and full dashboards are available in the subscriber package and are indispensable for underwriting investments, joint ventures, or new product programs.

Rapid due diligence for M&A: 60–90 day diligence packages that combine commercial validation, supply-chain deep dives, and integration planning.

Market-entry acceleration: localized certification roadmaps and dealer-partner selection strategies to accelerate first commercial deliveries in target metros.

Strategic procurement programs: master-supplier negotiation playbooks, risk-mitigation contract clauses, and inventory hedging strategies aligned to battery-price scenarios.

Growth in the Low Powered Electric Motorcycle and Scooter market is robust and multi-year. However, by 2026 the strategic contest shifts from simply capturing volume to embedding defensibility through modular platforms, software-enabled services, and regulatory-compliant product families. For many organizations the window to establish structural advantages is narrow — accelerating decisions on supply-chain architecture, platform investments, and ecosystem partnerships will determine who captures the disproportionate value this expansion will create.

To access the complete dataset, regional and segment-level forecasts, company scorecards, and implementation playbooks, please visit the PW Consulting research portal or contact our industry desk for a subscriber briefing.

For detailed analysis of this topic, please visit the official page:Low Powered Electric Motorcycle And Scooter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com