The Czech Capital Under the Stars: Where the Past Blends with the Celebration

Other |

2026-05-19 10:41:37

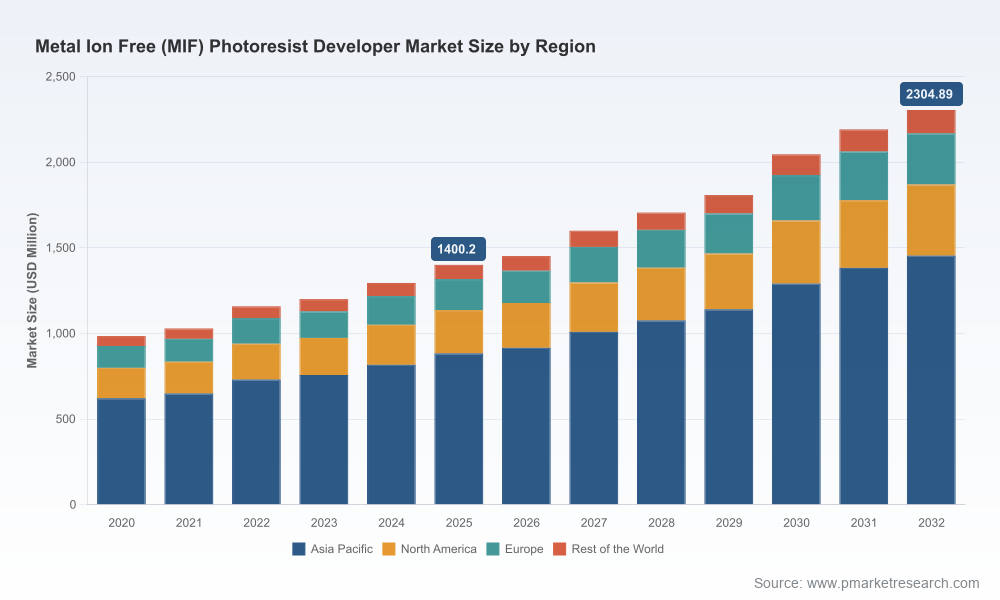

PW Consulting’s latest market research on Metal Ion Free (MIF) photoresist developers provides a forward‑leaning strategic framework for semiconductor, specialty chemical and advanced packaging executives preparing investment, procurement and product roadmaps in 2026. The market shows steady expansion from a post‑pandemic baseline (USD 984.5 Million in 2020) to USD 1,400.2 Million in 2025, with our projection pointing to continued growth through the decade. By 2026 the market is modeled at roughly USD 1,451.7 Million and the scenario analyses in this study project a rise to about USD 2,304.9 Million by 2032, implying a compound annual growth rate in the forecast window consistent with our headline CAGR of 7.38%.

Metal Ion Free (MIF) Photoresist Developer Market

Timing: 2026 is a pivotal year for many OEMs and fabs executing node transitions and qualification cycles; small changes in developer chemistry, supply continuity or cost profile can cascade into wafer yield and time‑to‑market outcomes.

Metal Ion Free (MIF) Photoresist Developer Market

Purity and process risk: MIF developers remain the technical standard for minimizing ionic contamination at sub‑0.5 µm and advanced lithography nodes. Our analysis translates that technical constraint into procurement and operational KPIs buyers must track this year.

Metal Ion Free (MIF) Photoresist Developer Market

Market consolidation and supplier leverage: The market is materially consolidated — a handful of suppliers control a dominant share — which creates both benefits (quality continuity, co‑development) and risks (single‑source exposures, pricing dynamics). Executives evaluating supply alternatives or partnership strategies need to account for concentration effects in 2026 contracting rounds.

Sustainability and regulation: New product introductions in 2024–2025 emphasize eco‑friendliness and regulatory alignment; suppliers that rapidly demonstrate lower environmental impact are gaining adoption in qualification pipelines this year.

The MIF photoresist developer market is expanding through a combination of ongoing lithography demand, migration to advanced nodes, and parallel growth in advanced packaging. After recovering from the cyclical troughs of the early 2020s, the addressable market scaled from under USD 1.0 Billion in 2020 to roughly USD 1.4 Billion in 2025. Our forecast models—rooted in capacity plans, bill‑of‑materials for wafer fab equipment and application intensity—show the market accelerating through the late 2020s as device scaling, mixed‑signal and memory demand push developer throughput higher.

Two structural forces underpin the forecast:

Technology imperative: chemically amplified resists and DNQ systems require metal‑ion‑free aqueous developers (typically TMAH‑based at industry standard normalities) to protect device reliability at finer geometries.

Supply architecture: a concentrated supplier base with high technical barriers to entry means lead times for qualification and ramp are non‑trivial — an operational reality that should shape 2026 sourcing strategies.

Our strategic vendor assessments highlight the following themes across the competitive set:

Scale and portfolio breadth: Large incumbents with broad photochemical portfolios and global manufacturing footprints are positioned to influence spec evolution and to offer compatible chemistries for both legacy and advanced resists. Their recent moves include launches of eco‑friendly or regulatory‑aligned MIF formulations and strategic partnerships to co‑develop customized solutions for high‑volume manufacturers.

Specialist incumbents and niche players: Several suppliers focus on lab‑to‑production transitions, drop‑in replacements and regionally optimized service models. These suppliers are often faster at responding to small‑lot customization requests and can be attractive as secondary sources or for pilot phases.

Distribution and channel roles: Dedicated chemical distributors and application specialists serve as important conduits for qualification at smaller fabs and R&D facilities, reducing time to test and enabling broader footprint for branded chemistries.

We profile the major competitors in the report, assess their R&D roadmaps, manufacturing redundancy, regulatory posture and channel strategies, and rank each on a tailored supplier scorecard that operationalizes risk, qualification time and co‑development potential. Recent industry activity (e.g., product launches of eco‑friendly MIF developers and strategic partnerships announced through mid‑2025) is already reshaping buyer expectations for sustainability and customization — factors that will influence contracting and qualification choices in 2026.

PW Consulting’s study is designed to be a working toolkit for commercial, procurement and technology teams. The full deliverable combines rigorous market modeling with operational playbooks and includes:

Proprietary market model with historical series and bottom‑up forecasts (2026–2032), stress‑tested under multiple demand and pricing scenarios.

Supplier scorecards and a qualification‑ready vendor shortlist tailored by risk appetite (rapid qualification, low total cost of ownership, sustainability priority).

Procurement playbook with recommended contract levers, inventory hedging tactics, and KPIs to embed in 2026 supplier agreements.

Technical due diligence checklist for MIF developer qualification, including test matrices for ionic contamination, photoresist compatibility and residue mitigation.

Price‑sensitivity and input cost analysis tied to TMAH feedstock movements and regional price trends, with actionable triggers for renegotiation or hedging.

Go‑to‑market and M&A considerations for chemical suppliers and private equity players seeking entry or consolidation opportunities.

Tetramethylammonium hydroxide (TMAH) is the primary upstream feedstock for MIF developers and is typically formulated at the well‑established normalities used across the industry. Our supply chain analysis identifies three near‑term pressure points for 2026 planning:

Feedstock volatility: TMAH price movements and regional demand shifts retained sensitivity in 2025; publicly available indicators showed softening in several regions due to cyclical semiconductor demand softness. Buyers should embed rolling‑window price triggers in contracts and consider multi‑sourcing strategies for critical qualification lots.

Regulatory and purity constraints: Buyers adopting more aggressive nodes must insist on documentation and lot traceability that explicitly addresses ionic contamination limits, given the material impact of metal ions on device yields.

Sustainability requirements: New formulations marketed as eco‑friendly have moved from novelty to selection criteria in supplier scorecards. Early engagement with suppliers on lifecycle assessments and waste‑water management can materially shorten qualification timelines.

For organizations making budgetary and sourcing decisions in 2026, the report advocates a pragmatic three‑track approach:

Protect current production: Immediately implement supplier resilience measures — dual‑sourcing for critical SKUs, fortified safety stocks for long lead time items, and accelerated qualification plans for approved alternates. Use our supplier scorecard to prioritize targets.

Optimize costs and margins: Negotiate forward‑looking purchase agreements with indexed price bands tied to transparent TMAH benchmarks, and condition renewal on supplier sustainability certifications that reduce long‑term compliance risk.

Invest in co‑development: For OEMs moving to advanced nodes, secure co‑development or exclusivity options early in 2026 with partners that have demonstrable R&D throughput and manufacturing redundancy; our partner suitability matrix highlights who can support accelerated node transition timelines.

In this preview we purposefully present the market trajectory, structural dynamics and supplier strategies while withholding the granular segmentation tables and unit‑level economics that make up the tactical playbook. The report contains detailed regional and application splits, pricing curves, contract template language and a downloadable vendor RFP checklist — the precise inputs procurement and product teams will use during 2026 negotiations and qualifications. Those granular datasets and executable templates are only available in the full report because they are the core instruments that enable action in contracting, sourcing and process qualification.

Our market model synthesizes primary interviews with fabs, photochemical suppliers and distribution partners conducted between 2024 and mid‑2025; purchase order and capacity reports from equipment and chemical manufacturers; and desk research including product launches and partnership announcements through June 2025. We triangulate demand scenarios with FAB capacity plans and upstream feedstock indicators (notably TMAH supply/demand trends) to produce a defensible range of outcomes and to stress‑test supplier concentration risk.

For strategic leaders the choice in 2026 is not simply which developer chemistry to specify, but how to structure relationships and contracts that ensure uninterrupted supply, compliance with tighter purity and sustainability requirements, and alignment with node migration timetables. PW Consulting’s MIF report is designed to convert market intelligence into operational decisions — from RFP language to co‑development timelines — and to reduce the risk of yield‑eroding surprises as device roadmaps accelerate.

Download the full report to obtain the complete segmentation, price curves and supplier RFP templates needed to execute 2026 procurement and qualification programs.

Contact PW Consulting for a tailored briefing that maps the report’s vendor scorecards directly to your bill‑of‑materials and technology roadmap.

PW Consulting — informed, pragmatic, and ready to convert MIF market intelligence into 2026 decisions that protect yield, reduce cost and accelerate time to market.

For detailed analysis of this topic, please visit the official page:Metal Ion Free (MIF) Photoresist Developer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com