Medical Fiber Laser Market 2026: Strategic Preview — What Leaders Must Know Now

As PW Consulting’s Senior Strategy Advisor and Head Industry Analyst, I present a concise, forward-looking briefing distilled from our comprehensive Medical Fiber Laser Market report (base year 2025). This executive preview highlights the market dynamics, competitive fault-lines, regulatory contours, and the near-term strategic choices that will shape outcomes through 2026. It is deliberately evaluative rather than exhaustive — a “trailer” that demonstrates methodological rigor and actionable insight while reserving proprietary segmentation detail for the full report.

Medical Fiber Laser Market

Market Snapshot: Momentum and Scale

The medical fiber laser market has transitioned from a specialized niche into a broadly adopted clinical toolset. Our historical analysis shows the market expanding from roughly USD 554 million in 2020 to about USD 950 million in 2025. Underpinning that expansion is sustained clinical adoption across urology, dermatology, ophthalmology and general surgery, coupled with iterative product launches that improve ergonomics, fiber durability, and clinical outcomes.

Medical Fiber Laser Market

Looking ahead, we forecast robust growth over the 2026–2032 horizon, with a compound annual growth rate (CAGR) of roughly 11.24%. By 2032 the market is on track to exceed USD 2 billion, driven by both unit-level innovations and increasing procedure volumes where fiber lasers offer clear clinical or workflow advantages. Market concentration is meaningful: the three largest players account for a significant share of revenue, and the five largest firms collectively control over half the market — a dynamic that shapes pricing, distribution access, and standards-setting.

Medical Fiber Laser Market

Why 2026 Is a Pivotal Decision Year

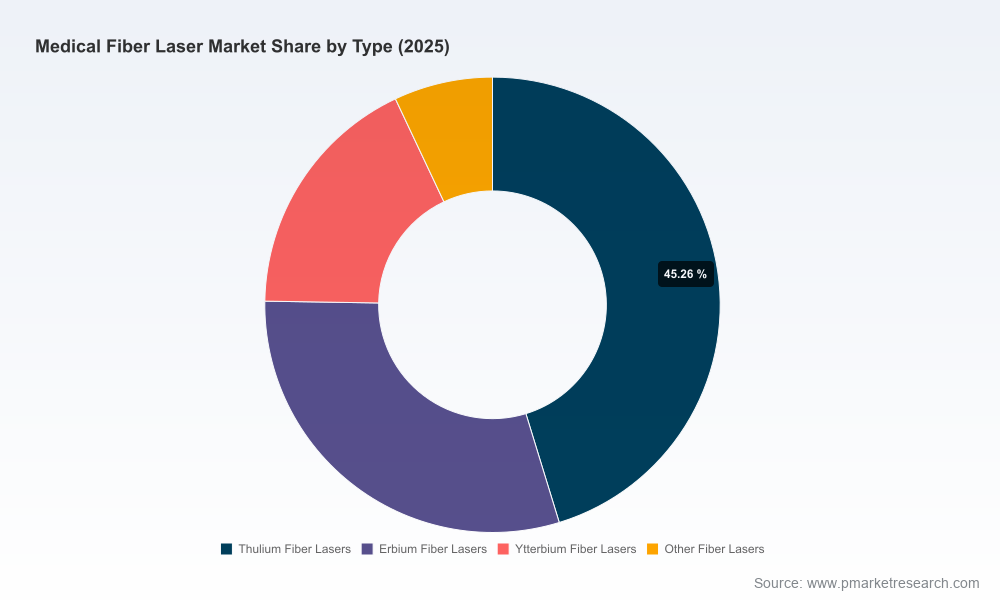

- Technology inflection points — Thulium fiber laser architectures, alongside specialty erbium and ytterbium variants, are reaching maturity in terms of reliability, size, and clinical performance. Vendors that consolidate clinical evidence and translate it into integrated system-fiber offerings will be advantaged.

- Commercial consolidation and channel leverage — Distribution partnerships and single-use consumable strategies are becoming decisive for access to ORs and procedure suites. Firms that combine platform sales with optimized recurring revenue streams (fibers, accessories, disposables) will widen margin differentials.

- Regulatory clarity — With multiple 510(k) decisions and established device-class pathways, faster-to-market entrants must still demonstrate substantial equivalence and robust post-market surveillance plans to sustain adoption in major markets.

- Reimbursement stability — Fiber-laser-based procedures are generally accommodated within existing CPT/DRG frameworks; therefore, the commercial rationale hinges on procedural efficiency, outcomes improvements, and provider economics rather than new code creation.

Technology & Clinical Trends to Watch

- Thulium fiber lasers (TFL) — Increasingly favored in urology for “dusting” strategies and reduced retropulsion in lithotripsy; high-frequency, compact designs enable new procedural workflows and outpatient migration.

- Erbium and specialty wavelengths — Erbium-doped fluoride fiber lasers (e.g., cold ablative modalities) are gaining traction in dermatology and aesthetic resurfacing where controlled ablation with minimized thermal injury matters.

- Fiber design and disposables — Advances in surgical fiber durability, side-fire geometries, and single-use sterile formats are shifting procurement logic from platform-first to ecosystem-first decision-making.

- Complementary system features — Integrated software, procedural presets, and user interfaces that lower training burden are becoming key purchase differentiators in hospital and ambulatory settings.

Regulatory & Reimbursement Context

Medical fiber laser systems and their delivery fibers fall under established regulatory pathways in major markets. In the U.S., they are typically regulated as Class II devices requiring 510(k) clearance with substantive equivalence to predicate devices for indications such as soft tissue ablation, coagulation, and lithotripsy. Compliance with GMP, labeling, and post-market surveillance is non-negotiable; companies should budget for lifecycle regulatory spend beyond the initial clearance.

From a reimbursement standpoint, procedures performed using fiber lasers generally map onto existing CPT/DRG codes for laser surgery. This reduces near-term coding uncertainty but raises the bar for vendors to demonstrate provider-level economic benefits (reduced OR time, complication reduction, outpatient migration) to support adoption when list price and consumable economics are scrutinized by hospital procurement teams.

Competitive Landscape — Who’s Shaping the Market

The competitive topology is heterogeneous: global laser OEMs, medical device distributors, and specialized fiber manufacturers each bring distinct strengths. Key players profiled in our study include legacy photonics leaders, endoscopy OEMs, and agile innovators focused on single indications. Recent market activity underscores a bifurcation between platform incumbents and focused challengers pushing differentiated wavelengths or consumable models.

- IPG Photonics / IPG Medical — Leveraging deep fiber laser engineering, IPG supplies thulium fiber laser systems and surgical fibers, with partnerships extending distribution reach. Their capability in laser source manufacturing gives them scale advantages in cost control and customization for urology applications.

- Coherent Corporation — With targeted launches of TFL platforms designed for therapeutic urology, Coherent is attempting to blend medical-grade reliability with clinical usability. Their packaged fiber assemblies are positioned to streamline clinician adoption.

- Quanta System — European OEM known for focused clinical systems; its TFL offerings aim at precise soft-tissue work and lithotripsy, often distributed through surgical channel partners to reach diverse markets.

- Acclaro Medical — A specialist on erbium-doped fluoride fiber lasers for dermatology, Acclaro’s clinical bench and active engagement at dermatology forums signals intent to broaden indications and gather multicenter evidence for premium dermatologic applications.

- Boston Scientific — As a major urology player, Boston Scientific combines distribution muscle with consumable strategies (single-use fibers) and leverages partnerships to integrate third-party TFL platforms into physician workflows.

- Cook Medical — A strategic distributor in procedural markets; Cook’s channel relationships enable laser OEMs to accelerate clinical penetration in specific geographies and specialties.

- Light Guide Optics — Specialist fiber manufacturer whose recent 510(k) clearance reinforces the commercialization tailwinds for higher-performance surgical fibers across wavelengths.

- Olympus Corporation — Endoscopy and surgical systems incumbent; its TFL offerings are part of a broader play to own end-to-end procedural ecosystems.

Recent regulatory and market events reflect an active competitive environment: new product launches for TFL platforms, FDA clearances for surgical fibers and system updates, and clinical presentations expanding indication sets. These moves accelerate the pace at which hospitals reassess their laser portfolios.

What Our Full Report Offers (Operational and Strategic Deliverables)

- Proprietary demand-modeling and scenario analysis covering 2026–2032 with sensitivity to pricing, adoption curves, and consumable attach rates.

- Go-to-market playbooks for OEMs and distributors, including channel partnership archetypes, pricing strategies, and procurement negotiation levers.

- Clinical adoption roadmaps by specialty that map evidence-generation priorities to reimbursement and hospital adoption milestones.

- Regulatory gap analysis and a tactical 510(k) playbook tailored to wavelength-specific device classes.

- Balanced scorecards and M&A target screening frameworks to identify acquisition candidates that deliver strategic capability (e.g., fiber IP, distribution, complementary console tech).

- Five-year financial impact models for stakeholder types (OEMs, distributors, hospital systems, private equity) showing ROI timelines under conservative, base, and optimistic scenarios.

Immediate Strategic Recommendations for 2026

- For OEMs: Prioritize bundled solutions that marry laser consoles with optimized fibers and clinical training. Invest in real-world evidence generation to shorten sales cycles and defend premium pricing.

- For Distributors & Channel Partners: Build flexible inventory models for single-use consumables and develop clinical liaison teams that reduce clinician onboarding friction.

- For Hospital Systems: Treat fiber laser acquisitions as platform decisions; evaluate lifetime consumable costs, training burden, and OR throughput impact rather than upfront capital cost alone.

- For Investors: Target firms with defensible consumable economics, regulatory clarity, and demonstrated clinical outcomes. Consider roll-up plays that combine OEM technology with established distribution footprints.

Conclusion & Next Steps

The medical fiber laser market in 2026 is not just growing — it is professionalizing. Suppliers who can align platform performance, consumable economics, and clinical evidence will win durable share. For executive teams making 2026 budget, partnership, or M&A decisions, the critical questions are: which wavelengths and use-cases will drive recurring revenue, how will regulatory timelines affect time-to-revenue, and what go-to-market model will secure long-term OR share?

PW Consulting’s full Medical Fiber Laser Market report provides the granular segmentation, scenario models, and vendor-level benchmarking that will support those decisions. This preview surfaces the strategic imperatives; the full report contains the data and tools required to operationalize them. For access to the complete dataset, downloadable models, and our vendor scorecard, visit PW Consulting’s report page.

For detailed analysis of this topic, please visit the official page:Medical Fiber Laser Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com