3D Parts Catalogs Software Market Report 2034: US Secures the Leading Share Globally

Other |

2026-04-28 13:57:42

PW Consulting’s latest Magnesium Bisglycinate API Market report (base year 2025; forecast 2026–2032) delivers a focused, decision-grade synthesis for executives shaping supply, product, and M&A strategies in 2026. The global market is expanding at a robust mid-single-digit to high-single-digit pace (projected CAGR: 8.12% across the forecast window), moving from a well-established 2025 base into a materially larger opportunity by 2032. This briefing summarizes the report’s practical value, highlights structural dynamics and competitive posture, and outlines the strategic actions senior leaders must prioritize this year — while preserving the detailed segment-level datasets and unit economics for readers who access the full report.

Magnesium Bisglycinate API Market

Timing: 2026 is the year many ingredient buyers, CDMOs, and finished-goods manufacturers will revisit sourcing strategies as demand for chelated magnesium accelerates across supplements, targeted medical nutrition and select pharmaceutical formulations. Our forecast window (2026–2032) aligns with typical capital planning and product development cycles, enabling immediate operational adjustments and medium-term capacity investments.

Magnesium Bisglycinate API Market

Clarity on scale: The report quantifies market scale and trajectory at a level suitable for board-level discussions — inclusive of year-by-year revenue build to 2032 — enabling stress-tested scenarios for capacity utilization, price sensitivity, and working-capital needs.

Magnesium Bisglycinate API Market

Competitive benchmarking: We map the supplier landscape, regulatory dossiers, and certification footprints that materially affect qualification timelines for USDMF/DMF, CEP/COs, and global nutraceutical registrations — a critical gating factor for 2026 product launches and contract awards.

Market sizing and trajectory: Detailed annual revenue series from historical years through 2032, accompanied by scenario analyses reflecting raw-material stress and accelerated uptake in targeted end-use categories.

Supplier scorecards: Actionable vendor assessments covering manufacturing standards, certification status, geographic supply nodes, typical lead times, quality accreditations and dossier coverage (e.g., DMF/USDMF/CEP), plus qualification checklists for procurement teams.

Commercial playbooks: Recommended sourcing strategies (dual-sourcing, tolling, contract manufacturing), pricing negotiation levers, and inventory buffer models tuned to API shelf-stability and non-hygroscopic grades.

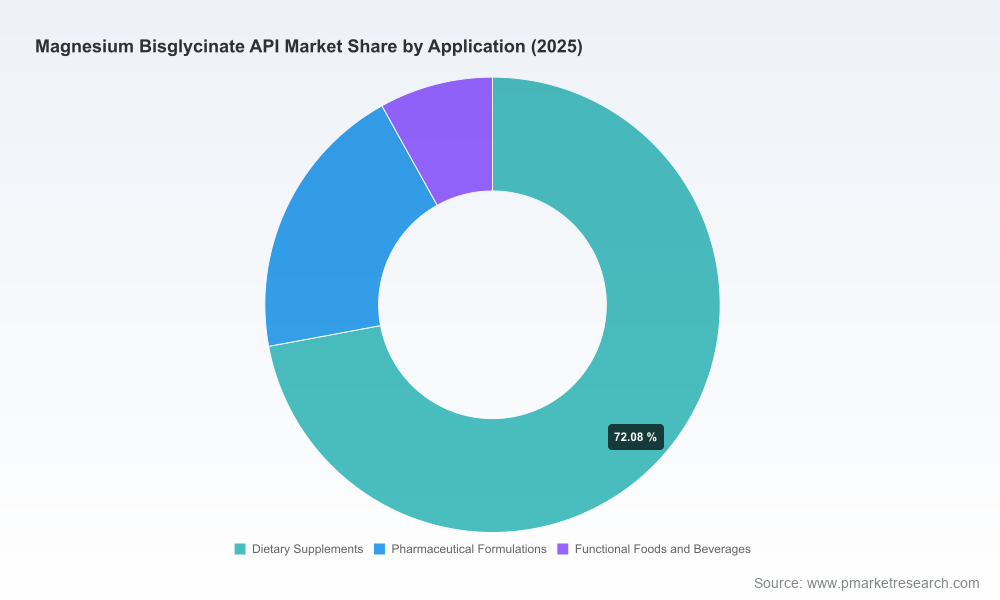

Formulation and positioning guidance: Evaluation of purity grades and chelate technologies tied to bioavailability and gastrointestinal tolerability, with guidance on label claims, clinical endpoints, and route-to-market implications for supplements versus pharmaceutical applications.

Regulatory and quality risk register: A prioritized list of dossier gaps, audit triggers, and remediation timelines that influence go-to-market windows, including recommended audit cadences and CAPA templates.

Executive dashboards: KPI templates for procurement, R&D and C-suite monitoring — from supplier concentration metrics and CR3/CR5 indicators to margin sensitivity under raw-material shock scenarios.

Our analysis points to a moderately consolidated supplier base; the top-tier competitors account for a majority share of the market by revenue and certified pharmaceutical supply. Concentration metrics indicate significant supplier influence in pricing and qualification timelines. For procurement and corporate development teams, this translates into a few concrete actions: lock in multi-year supply contracts with visibility on quality documentation, invest selectively in dual-sourcing for critical SKUs, and consider strategic equity or off-take arrangements where timeline certainty is essential.

The competitive field spans heritage European specialty producers, established Indian API manufacturers, and US-based chelate innovators. Key providers combine differentiated chelation technologies, clinical evidence, and regulatory dossiers — attributes that materially shorten product qualification cycles in regulated markets.

Specialized European producers maintain leadership in fully reacted true chelates and emphasize clinical positioning around tolerability and targeted health outcomes. Their investments in certification and consumer-facing claims (e.g., formulations targeting sleep and recovery) make them preferred partners for premium formulations.

Large Indian API manufacturers offer scale, cost flexibility, and extensive DMF/USDMF/CEP coverage that appeal to contract manufacturers and high-volume supplement brands. Their role is central to cost optimization and regional supply continuity.

US-based innovators leverage proprietary chelation technologies and clinical-trial-backed platforms to command premium positioning in nutraceutical and clinical nutrition channels; their value proposition is speed to differentiated label claims and formulation support.

Recent company-level developments underscore these dynamics: a leading European manufacturer renewed food-safety certifications while explicitly repositioning its chelate for sleep and “restorative recovery” applications in longevity-oriented formulations; Indian producers have been reinforcing API quality credentials and publicizing production under stringent pharma-grade controls; US players continue to emphasize clinically researched chelate platforms and robust regulatory filings — all of which influence qualification and commercial timelines in 2026.

Raw-material volatility is a central sensitivity in our scenario modeling. Key inputs such as magnesium hydroxide and elemental magnesium have shown recent price moves and should be modeled explicitly in procurement and pricing strategies. For example, magnesium hydroxide pricing in North American markets evidenced a firm upward trend in late 2025, while elemental magnesium spot valuations moved appreciably in early 2026. Independently, broader oxide markets are forecast to expand materially over the coming decade, creating potential upstream scarcity and substitution pressures.

Operational implications for 2026:

Incorporate raw-material pass-through clauses and trigger points into supplier contracts to protect margins without compromising supply continuity.

Quantify lead-time risk by mapping critical-path raw-material sourcing to finished-API production and finished-goods launches; prioritize inventory for high-value SKUs with constrained supply windows.

Evaluate toll-manufacturing and backward integration options where on-site conversion capabilities materially reduce exposure to upstream price swings.

High-purity and pharmaceutical-grade documentation (DMF/USDMF, CEP, GMP/WHO-GMP) remain decisive for access to regulated markets. The report includes a prioritized audit matrix that correlates dossier completeness with expected qualification lead time — a pragmatic tool for R&D and regulatory teams that must certify suppliers for clinical, Rx, and medical-food uses within 12–18 month windows.

Key recommendations:

Prioritize suppliers with up-to-date certifications and public audit histories when planning 2026 launches in regulated territories.

Invest in pre-qualification sampling and accelerated stability testing for chelated APIs to compress time-to-market for clinical nutrition products.

Use contract clauses to secure documentation updates and audit access as a condition of supply renewal.

Formulation-side innovation is shifting demand toward chelates that can substantiate bioavailability and GI tolerability claims. Our market intelligence shows premium product positioning — including sleep, recovery, metabolic health, and age-related nutrition — increasingly leverages clinically validated chelate platforms. For R&D teams, this raises an important trade-off: favor proprietary, clinically backed ingredients to command pricing power and consumer trust, or opt for cost-optimized suppliers for mass-market formulations.

Investor interest is converging on three themes: specialty chelate technologies with clinical validation, API producers with pharma-grade certifications, and integrated players able to offer finished-formulation support. The market’s concentration profile makes targeted bolt-ons attractive for companies seeking rapid scale in certified supply. For private equity and corporate development teams, the report provides valuation sensitivities tied to revenue growth and margin under varying raw-material scenarios, facilitating faster transaction screening and diligence prioritization.

Procurement leaders: adopt the supplier scorecards and audit templates to compress qualification timelines and mitigate concentration risk.

R&D and product teams: use the formulation guidance to select chelate platforms aligned with intended claims and regulatory pathways.

CFOs and corporate development: model capex and M&A scenarios using the annualized market projections and CR-based concentration inputs to validate investment timing and deal sizing.

Quality and regulatory heads: implement the prioritized audit matrix and dossier-gap remediation playbook to de-risk 2026 launches in regulated markets.

This executive brief is intentionally scoped to surface the strategic implications most relevant to 2026 planning while reserving the granular segment tables, pricing grids, regional allocations, and supplier financials for the full report. PW Consulting clients and report purchasers receive the complete datasets, supplier scorecards, and modeled scenario workbooks that underpin the conclusions summarized here.

For procurement, R&D, and M&A teams preparing tactical plans this year, the full report is the operational toolset that converts the high-level imperatives above into executable project plans — from supplier qualification checklists and contract templates to scenario-modeled P&L and capex cases. Contact PW Consulting to obtain the full Magnesium Bisglycinate API Market report and the associated data workbook to inform your 2026 decisions.

For detailed analysis of this topic, please visit the official page:Magnesium Bisglycinate API Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com