Europe Home Ventilation System Market Share, Demand Drivers and Industry Trends

Other |

2026-06-22 11:29:38

PW Consulting’s latest market intelligence on the Lead Based Rare Earth Alloy market (base year 2025) reframes how manufacturers, battery OEMs, materials traders and investors should approach 2026. This sector—anchored to legacy lead metallurgy but increasingly shaped by rare‑earth inputs, regulatory pressure and end‑market electrification dynamics—presents a predictable mid‑single digit growth profile alongside episodic upstream volatility. Our forecast model projects the market at USD 306.0 Million in 2025, rising to USD 317.76 Million in 2026 and expanding at a 5.0% CAGR across the 2026–2032 forecast window to reach USD 430.57 Million by 2032. This report is designed to support boardroom decisions, capex prioritization, procurement strategies and M&A target screening in the coming 12–24 months.

Lead Based Rare Earth Alloy Market

Transitional demand drivers: Lead‑acid battery markets remain a core application for lead‑rare earth alloys. While mobility electrification shifts some battery spend toward lithium chemistries, industrial, stationary and start‑stop automotive segments continue to underpin demand for alloy performance improvements in grid corrosion resistance and mechanical durability.

Lead Based Rare Earth Alloy Market

Supply chain tightness and upstream price shocks: Rare earth concentrates and separated products are experiencing renewed price pressure driven by concentrated upstream supply. Notably, industry reporting indicates a marked step‑up in rare earth concentrate pricing in Q2 2026—an early warning that procurement and hedging strategies must be rethought.

Lead Based Rare Earth Alloy Market

Regulatory and ESG constraints: Lead‑based manufacturing remains highly regulated for environmental and occupational health reasons. Investment decisions in 2026 must now internalize both direct compliance costs and the reputational premium associated with cleaner production footprints and robust worker protection systems.

Historic sizing in our baseline model captures recovery and retrenchment between 2020 and 2025, with the market moving from USD 240.5 Million in 2020 to USD 306.0 Million in 2025, reflecting cyclical rebounds and structural demand for higher‑performance alloys. In 2026 the market is projected to expand to USD 317.76 Million, and our scenario suite indicates a steady aggregate growth trajectory over the forecast horizon (CAGR 5.0%), albeit with intermittent upticks tied to raw‑material shocks and regional policy interventions. These macro trajectories are robust enough to support investment planning, but sensitive enough that optimal timing and sizing of capital deployment require scenario testing against supply‑side discontinuities and regulatory inflection points.

Upstream concentration: Rare earth feedstock supply remains geographically and institutionally concentrated. Price setting and availability at the upstream end directly influence alloy cost curves. For example, Q2 2026 price movements for rare earth concentrate reported regionally underscore quarter‑on‑quarter supply tightness and rapid cost pass‑through risk for alloy producers.

Vertical integration vs. market purchasing: Firms with integrated rare‑earth or non‑ferrous upstream assets demonstrate resilience to spot price shocks. For non‑integrated players, long‑term off‑take, vertical partnerships, or investments in domestic separation and metallization capacity are strategic levers to stabilize input costs.

Secondary supply and circularity: Recycling and closed‑loop recovery of lead and rare‑earth enriched alloys are gaining traction as a cost and compliance mitigation strategy. Our cost‑curve analysis demonstrates early movers in alloy recycling can capture margin expansion while reducing exposure to concentrate price volatility.

Domestic and international policy programs are reshaping competitive dynamics. Public funding initiatives in 2025 targeting rare earth processing capacity illustrate how governments are willing to underwrite strategic on‑shore capability, which can re‑rank supply risk for firms with exposure to concentrated foreign sources.

Lead‑related environmental and occupational health standards continue to tighten. Compliance readiness—measured through emissions control, worker protection processes and traceability systems—has moved from a compliance checkbox to a commercial differentiator in supplier selection and offtake contracting.

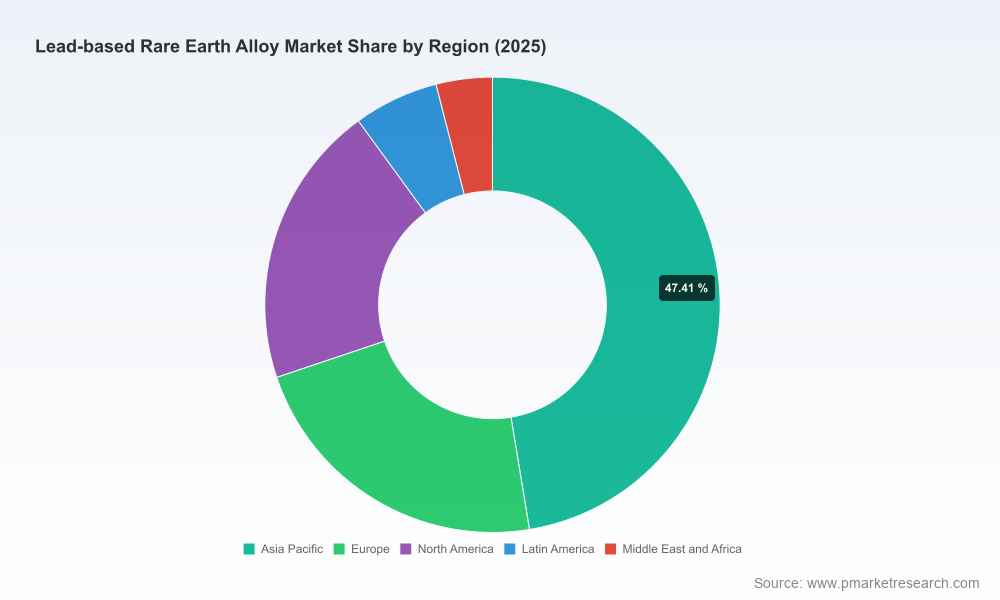

The market displays a moderate level of concentration — the top three players account for a meaningful share of the market and the top five further consolidate supply. Leading firms are predominantly vertically integrated non‑ferrous groups with end‑to‑end exposure across primary lead, zinc and rare‑earth inputs. Examples include tradenames and groups active in China’s non‑ferrous ecosystem, plus specialized manufacturers focused on master alloys and customized Pb‑Re product forms.

Integrated producers: Several large non‑ferrous and mining groups provide an integrated pathway from raw metal through alloy production. Their strategic advantages include guaranteed feedstock, scale economics and the ability to blend rare‑earth inputs to customer specifications for battery grid performance improvements.

Specialized alloy fabricators: Firms focused on master alloy production and downstream forms (wire, strip, forgings) compete on product purity, custom formulations and logistical service levels. These capabilities matter for OEMs seeking tight process control in battery manufacturing or radiation‑shielding applications.

Strategic implications for MNCs and entrants: New entrants without upstream access or strategic partnerships will face margin pressure during raw material spikes and must therefore plan for either strategic alliances, targeted capex in recycling/separation, or niche product differentiation that commands premium pricing.

Our research pack goes beyond headline forecasts to deliver operationally actionable intelligence for 2026 decision cycles. Key elements include:

A transparent, auditable forecasting model (2026–2032) with scenario toggles for raw‑material price stress, regulatory tightening and demand substitution (e.g., migration of battery applications to alternative chemistries).

Supplier risk heatmaps and a procurement playbook that quantify counterparty delivery risk, price pass‑through exposure and contractual levers for risk sharing (indexed pricing, minimum take obligations, reciprocal inventory).

Competitor benchmarking and capability maps across eight manufacturing and product dimensions—feedstock integration, product range, form factor capability, QC and traceability, environmental controls, certification footprint, geographic reach and customer concentration.

Practical M&A and JV target shortlists derived from liquidity profiles, asset complementarity and strategic fit criteria, plus a phased integration playbook for supply chain and R&D consolidation.

Regulatory compliance templates, capital‑budget scenarios for emissions control retrofits and an ROI model for circularity investments (scrap recovery, alloy reprocessing).

Secure and diversify upstream access: Move from spot exposure to a layered procurement posture—combining strategic off‑take agreements, syndicate purchasing and, where justified, minority equity in separation/metallization capacity.

Accelerate circularity pilots: Commission targeted investments in scrap collection and reprocessing trials where feedstock quality can be demonstrated. Early commercial pilots can reduce input cost volatility and provide compliance advantages.

Prioritize compliance‑driven capex: Upgrade emissions controls and worker safety systems as a near‑term commercial bet—a failure to meet evolving regulatory thresholds increasingly risks customer de‑listing and fines.

Differentiate via product engineering: Invest in alloy R&D that optimizes the rare‑earth mix for specific grid applications and end‑use conditions; product differentiation commands premiums and mitigates commoditization.

Embed scenario‑based planning in board reviews: Use the report’s scenario suite to stress test capex, pricing and inventory strategies against plausible raw‑material shocks and policy shifts through 2032.

We pair the market model with hands‑on execution support: procurement negotiation playbooks, technical due diligence on alloy production assets, operational integration blueprints for recycling lines, and regulatory audit frameworks. For clients pursuing inorganic growth, we provide valuation overlays that incorporate commodity‑price contingent earnouts and compliance‑linked warranty structures.

The executive summary above intentionally presents the strategic contours without reproducing the granular regional and application‑level splits and client‑level contract benchmarks that are essential to transactional work. The full report contains those datasets, plant‑level capacity maps, and downloadable model files that enable bespoke scenario tailoring. If your 2026 strategy depends on defensible procurement, targeted capex or selective M&A in the Lead Based Rare Earth Alloy market, PW Consulting can provide the full suite of analysis and transaction support to convert insight into action.

Contact PW Consulting to arrange a briefing and obtain the full report and model access. Our team will walk your leadership through the scenarios most relevant to your footprint and deliver a prioritized action plan suitable for board approval cycles in 2026.

For detailed analysis of this topic, please visit the official page:Lead Based Rare Earth Alloy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com