Open Circuit Combustible Gas Detector Market — Strategic Preview for 2026 Decision-Making

Executive snapshot

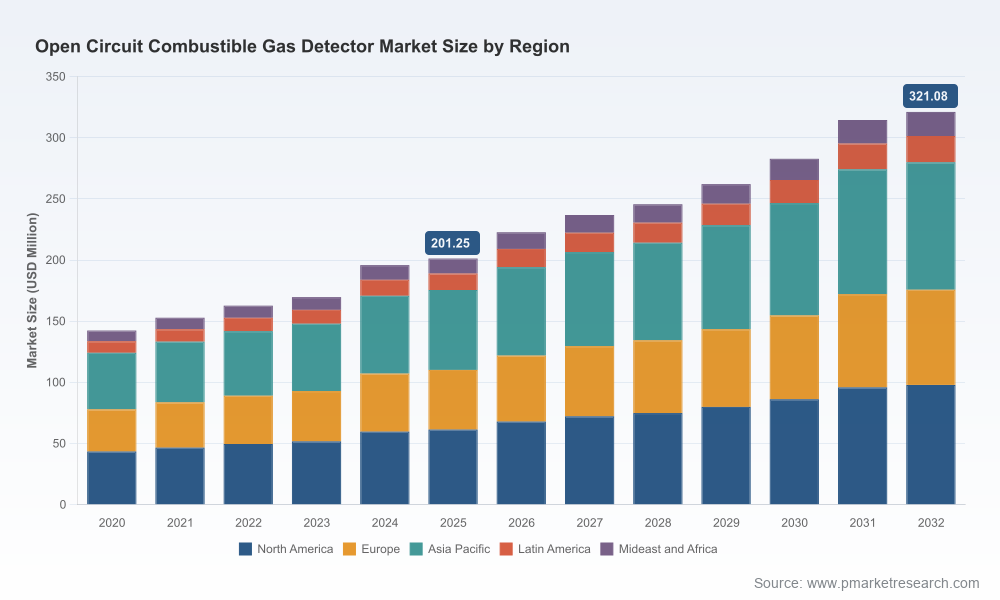

PW Consulting’s latest market study on Open Circuit Combustible Gas Detectors offers a forward-looking, actionable intelligence package timed for executive planning cycles in 2026. The market has demonstrated steady expansion through the first half of this decade — rising from roughly USD 142 million in 2020 to about USD 201 million in 2025 — and our base-case projection (2026–2032) anticipates continued growth at a compound annual growth rate of 6.85%. Under our layered scenarios the market reaches the low‑hundreds of millions by the late 2020s and approaches a materially larger footprint by 2032.

Open Circuit Combustible Gas Detector Market

Market concentration is moderate: the three largest vendors account for just under forty percent of reported revenues, with the top five nearing the majority share. That structure creates a dynamic environment where incumbent scale advantages sit alongside material opportunities for specialist entrants, vertical integrators and disciplined consolidators.

Open Circuit Combustible Gas Detector Market

Why this report matters for 2026 corporate strategy

- Capital planning: vendors and end users need confidence on demand trajectories before committing to multi‑year manufacturing or field deployment investments.

- Product roadmaps: technology choices (infrared, catalytic, laser and sensor fusion platforms) and connectivity requirements must align with projected operating environments and regulatory expectations.

- M&A and partnerships: with a moderately concentrated market, strategic acquisitions and technology alliances can be high-impact levers to scale offerings or enter fast-growing adjacencies.

- Regulatory compliance & risk mitigation: pending and standing approvals influence acceptable design, testing and certification timelines — a critical input to time-to-market and tender responsiveness.

What the report delivers — practical, transaction-ready intelligence

This study is designed as a working tool for leadership teams, corporate development groups, product management and safety engineers. Key deliverables include:

Open Circuit Combustible Gas Detector Market

- Market sizing and a granular forecast model spanning 2026–2032, with scenario sensitivity for demand drivers and downside stress tests for raw material inflation.

- Vendor landscaping and competitive benchmarking: profiles, capability maps and commercial positioning for manufacturers, distributors and system integrators.

- Technology deep dives that evaluate trade-offs across open-path infrared, catalytic open-circuit and emerging laser-based and sensor-fusion solutions, including performance, false-alarm characteristics and lifecycle cost implications.

- Regulatory and standards mapping (including relevant industry approvals and test standards), plus an assessment of compliance timelines by product class.

- Go-to-market playbooks: tender strategies, service & aftermarket monetization models, and retrofit prioritization frameworks tailored for asset owners in heavy industry.

- A proprietary Excel model and executive dashboard for what-if analysis — enabling procurement teams and CFOs to stress-test budgets and ROI for deployment scenarios.

To preserve the integrity of our primary data assets and to ensure that client engagements are built on verified detail, the public briefing intentionally omits the full segmentation tables and line-item forecasts; these are accessible through our report portal.

Competitive landscape — strategic implications

The competitive set combines diversified industrial conglomerates, specialist safety vendors and regional distributors. Key players we profile and assess include:

- Emerson (Rosemount / Spectrex): A scale incumbent with a deep installed base in harsh hydrocarbon environments. Emerson’s open-path infrared offerings are positioned to leverage enterprise procurement cycles and service contracts; their product breadth supports large-scale replacement programs but also invites continuous innovation to defend against niche entrants.

- MSA Safety: With established IR detector lines and recent activity around connected portable detectors, MSA is advancing a platform play — integrating field devices into broader safety and asset‑management ecosystems. Their emphasis on false‑alarm rejection and connectivity is strategically aligned to customers prioritizing operational intelligence over point-detection cost alone.

- Teledyne Gas & Flame Detection: Product previews and pre‑launch activity signal a push on laser-based and next‑generation open-path devices, particularly for challenging target gases. Trade-show previews indicate an aggressive product cadence aimed at both retrofit and new-build oil & gas opportunities.

- GDS Corp: As a regional distributor and systems partner, GDS provides local market reach and aftermarket capabilities that remain critical for field service-dependent segments. Distributors like GDS are important acquisition targets for vendors seeking improved channel control.

- Det-Tronics (UTC): A platform vendor focused on industrial-grade continuous monitoring systems, Det‑Tronics’ offerings are suited for customers with high safety/regulatory demands; their product certification depth is a competitive moat in safety-critical verticals.

Recent market activity — for example product previews and connected-detector launches in late 2025 — underscores a tactical pivot across vendors: accelerating feature-rich devices (connectivity, improved algorithms for false alarm mitigation, and laser detection for specific chemistries) while protecting certified performance levels that buyers require for site approvals.

Market forces and dynamics shaping 2026 decisions

- Regulatory and standards pressure: Longstanding standards and approvals frameworks remain decisive for procurement. Performance requirements embedded in industrial standards inform acceptable product architectures and testing regimens; compliance timelines should be baked into product commercialization schedules.

- Technology convergence: Laser-based detection and enhanced infrared systems are reducing some historical trade-offs between sensitivity and range. Meanwhile, advances in digital connectivity and analytics are shifting value capture to software and services — elevating aftermarket revenue potential.

- Raw material and cost pressure: Inflationary input-costs and supply-chain disruption continue to influence unit economics and pricing flexibility. Manufacturers who secure diversified suppliers and invest in design-for-cost now will enjoy margin resilience.

- Service & retrofit demand: A large installed base of legacy systems creates a multi-year market for upgrades, retrofits and managed services. Vendors that bundle installation, calibration and remote-monitoring subscriptions will unlock higher lifetime value per asset.

- Consolidation potential: Moderate concentration suggests room for targeted M&A to secure technology gaps (e.g., laser detection, connectivity stacks) and to expand regional service footprints.

Actionable recommendations for 2026 planning

For executive teams preparing budgets and strategy for the coming year, PW Consulting recommends a prioritized six-point plan:

- Align R&D investments with certification roadmaps. Prioritize development paths that meet approved performance standards to avoid costly rework when seeking site acceptance.

- Adopt a dual-channel go-to-market: maintain distributor and systems integrator partnerships for reach, while piloting direct managed-service offerings on strategic accounts to capture higher-margin recurring revenue.

- Design retrofit-first product variants that lower installation complexity and present fast ROI for asset owners; these accelerate adoption amid capex-constrained customers.

- Harden supply chains: lock sourcing agreements for critical sensor components and qualify secondary suppliers to mitigate input-price volatility and lead-time risk.

- Build data and software capabilities: invest in cloud-native analytics and predictive maintenance apps — these are increasingly decisive in procurement evaluations.

- Screen acquisition targets using a two-tier filter: (1) technology fit (sensor, optics, software) and (2) channel value (installed base, regional service capability). Targets that meet both criteria deliver rapid scale and margin uplift.

How to use PW Consulting’s report in executive workflows

- Strategy teams: use the included scenarios to stress-test three-year capex and product investments.

- M&A and corporate development: apply the vendor benchmark and valuation playbook to shortlist and prioritize targets.

- Sales and product management: leverage the go-to-market playbooks and retrofit strategies to shape the 2026 commercial calendar.

- Safety and engineering: consult the standards mapping and technology trade‑offs when drafting procurement specifications and tender documents.

Next steps

This preview is intended to orient 2026 decision-making and to signal the strategic depth available in PW Consulting’s full market offering. The complete report contains the full segmentation datasets, vendor financial proxies, downloadable models and a prioritized shortlist of acquisition targets and pilot customers. For access to the full dataset, consultancy briefings and licensing of our forecast model, visit the report page on the PW Consulting portal or contact our industry desk to schedule a tailored executive briefing.

PW Consulting remains available to support rapid strategy workshops, vendor due diligence, and bespoke market-sizing requests tailored to your portfolio or geographic focus.

For detailed analysis of this topic, please visit the official page:Open Circuit Combustible Gas Detector Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com