Custom Tuxedo NYC: The Ultimate Guide to Black-Tie Style and Perfect Fit

Other |

2026-06-22 16:49:43

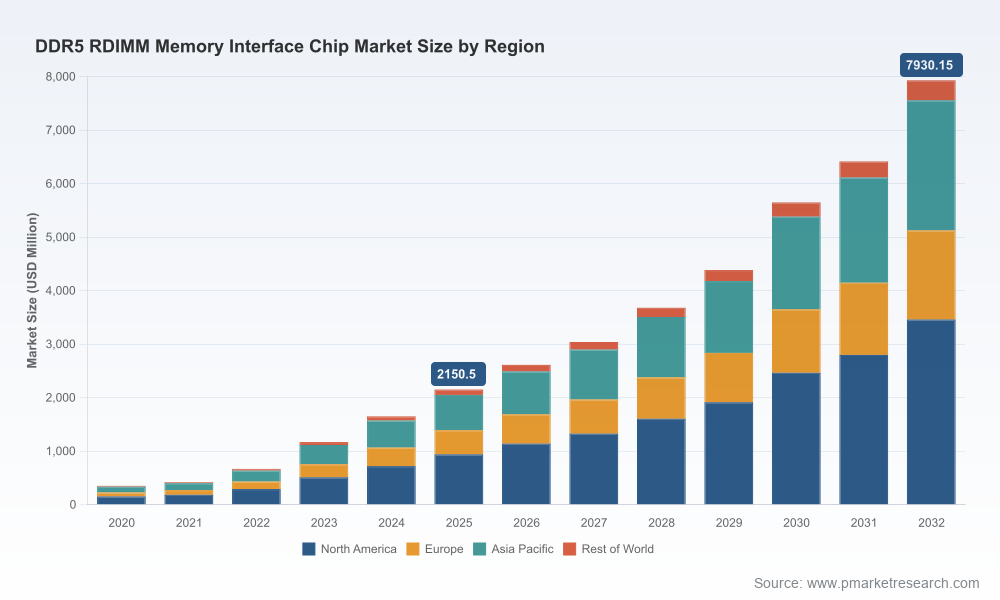

PW Consulting today publishes an executive briefing from our comprehensive DDR5 RDIMM Memory Interface Chip Market report (base year 2025). The briefing synthesizes our quantitative market model and hands-on strategic playbook to help senior executives make high-confidence decisions in 2026. At the macro level, the RDIMM interface market has accelerated from USD 350.0 Million in 2020 to USD 2,150.5 Million in 2025, and our forecast anticipates continued expansion to USD 7,930.15 Million by 2032 — a compound annual growth rate (CAGR) of 20.45% over the 2026–2032 forecast window. These numbers capture a structural shift driven by AI-driven compute demand, server refresh cycles and the mainstreaming of DDR5 register and power-management solutions.

DDR5 RDIMM Memory Interface Chip Market

Technology inflection: The market is transitioning from Gen4 to Gen6 performance envelopes. Product introductions and mass-production ramps in 2024–2026 are reshaping BOM compositions for server RDIMMs and setting new thermal, signal-integrity and power-delivery requirements for module manufacturers and system OEMs.

DDR5 RDIMM Memory Interface Chip Market

Supply-chain reconfiguration: 2025 regulatory changes — including tariff adjustments affecting semiconductor components — together with geographic demand shifts have accelerated supplier re-shoring, dual-sourcing and regional qualification programs.

DDR5 RDIMM Memory Interface Chip Market

Demand shock from AI and hyperscale: Capacity and bandwidth requirements from AI training and inference workloads are driving higher-content RDIMMs per server and compressing lead times for high-speed registered clock drivers (RCDs), PMICs and related interface chips.

Market concentration: A small group of specialized players captures the majority of interface chipset value, raising strategic questions about supplier leverage, co-development opportunities and potential single‑source risks.

Transparent market model — a validated, bottom-up demand model spanning 2020–2032 with scenario layers for AI, cloud, enterprise refresh and workstation uptake.

Technology adoption timeline — Gen3→Gen4→Gen6 transition mapping with performance breakpoints, qualification timelines, and OEM adoption milestones.

Supplier scorecards — multi-dimensional assessments of product performance, roadmap alignment, capacity, quality and geopolitical exposure across device classes (RCD, data buffers, PMIC/SPD hubs).

Commercial playbooks — pricing and negotiation levers, contractual structures (volume commitments, hedges, consigned inventory), and go‑to‑market templates for module makers and system integrators.

Cost & TCO tools — module BOM sensitivity models, thermal and power budgets, and TCO comparators to decide when to integrate higher-function chips versus outsource.

Risk & scenario planning — supply disruption heatmaps, tariff impact analyses and mitigation strategies optimized for 12‑, 24‑ and 36‑month horizons.

M&A and partnership screening — priority targets, capability gaps, and a valuation overlay that integrates technology readiness and customer concentration.

Rambus (San Jose, CA): A complete DDR5 server DIMM chipset provider with leading high‑speed RCD capability and integrated PMIC/SPD solutions. Recent industry recognition for its 8000 MT/s RDIMM chipset underscores its capacity to couple performance with production-readiness for data center and AI workloads.

Renesas Electronics (Tokyo): Delivering Gen4 and Gen6 RCD roadmaps; recent product launches place it among the earliest suppliers claiming 9600 MT/s registered clock drivers for next‑generation RDIMMs. Renesas’ regional commercial focus is an important factor for OEMs evaluating local supply options.

Montage Technology (Shanghai): A high-volume supplier that has transitioned Gen4 RCDs into mass production, offering a cost-performance profile attractive to large-scale module manufacturers pursuing established server platforms.

Power and analog specialists — Texas Instruments, Analog Devices, Infineon: These vendors are the backbone of DDR5 PMIC evolution. Their roadmap choices on thermal efficiency, multi-rail integration and manufacturability materially affect module BOM and system cooling strategies.

Market structure note: Our concentration analysis shows a high share controlled by the top-tier suppliers, amplifying the strategic importance of supplier choice, design partnerships and contractual protections for buyers.

Product and awards: Recognition of high‑speed chipsets in 2026 validates ramped performance in production environments — a key signal for hyperscalers prioritizing marginal bandwidth gains per rack.

Mass production events in 2025: They indicate the window in which module makers can lock in mature, cost-competitive DDR5 interface solutions versus waiting for next-gen yields to improve.

Regulation and tariffs: Early‑2025 tariff adjustments have already prompted sourcing shifts; organizations must bake tariff scenarios into procurement and RFQ planning to avoid margin surprises.

Raw-material and contract-price pressure: With contract prices for memory modules projected to rise under AI-driven demand, TCO optimizations and long-term supply agreements are no longer optional for cost-sensitive operators.

Embed performance roadmaps into product planning: If your products target data center or AI markets, accelerate validation tracks for Gen6-capable RCDs and PMIC integration now, because qualification cycles and thermal rework can take multiple quarters.

Establish dual‑track sourcing: Combine a tier‑1 strategic partner with a secondary qualified supplier to manage lead‑time and concentration risks without forfeiting performance optimization.

Negotiate modular commercial clauses: Include yield-based price adjustments, volume callbacks and shared ramp commitments to align incentives with suppliers during early production ramps.

Hedge raw-material exposure and pricing: Use our price sensitivity matrices to decide between short-term spot coverage and multi-year contracts tied to production milestones.

Invest in co-engineering: For system OEMs and hyperscalers, co-developing RCD/PMIC integration with chip vendors reduces system-level redesign and accelerates time-to-performance.

Prioritize thermal and power optimization: PMIC choices materially affect rack-level power and cooling; early thermal co-design avoids late-stage BOM churn and unplanned CAPEX for cooling upgrades.

Run M&A and partnership screens: Identify target capabilities (e.g., local footprint, specialized analog IP, or deep server customer relationships) that would accelerate your roadmap with a favorable cost of integration.

Prepare for regulatory permutations: Have approved alternate sourcing routes and tariff pass-through clauses ready to deploy under short notice.

Interactive Excel models and downloadable dashboards that let you stress-test demand, price and supply scenarios against your internal assumptions.

Supplier due-diligence templates and a negotiation playbook tailored for both module makers and system OEMs.

Roadmap synchronization templates that map supplier launches to OEM qualification gates and production milestones.

Action-ready risk mitigations — shortlists of alternate suppliers, conversion cost calculators and regional qualification checklists.

CEOs & CFOs: Use the market trajectory and TCO scenarios to set capital allocation priorities and decide on strategic partnerships or M&A lanes in 2026.

VPs of Procurement & Supply Chain: Apply the supplier scorecards and negotiation playbook to reshape sourcing strategies and mitigate tariff and concentration risks.

CTOs & Product Heads: Leverage the technology adoption timelines and co‑engineering recommendations to de-risk product launches and avoid costly late-stage rework.

Investors & Strategic Planners: Use the concentration and growth metrics to identify consolidation targets, investment windows and exit scenarios within the supply ecosystem.

PW Consulting’s full DDR5 RDIMM Memory Interface Chip Market report contains the granular segmentations, module-level price curves, supplier rankings and downloadable models that underpin the recommendations summarized here. In keeping with our “trailer” approach, this release surfaces the strategic implications and high‑level model outputs to guide 2026 decisions — the detailed segmentation tables, regional demand curves and supplier-level financials are available in the full report on our website.

For board-level briefings, procurement deep dives or a customized scenario run tied to your product roadmap, PW Consulting provides tailored engagements that embed our models into your planning cadence. Contact our industry team to schedule a briefing and obtain the full dataset and playbooks referenced in this briefing.

For detailed analysis of this topic, please visit the official page:DDR5 RDIMM Memory Interface Chip Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com