Checkpoint Kinase Inhibitor Market: Insights, Key Players, and Growth Analysis

Other |

2026-06-22 12:51:08

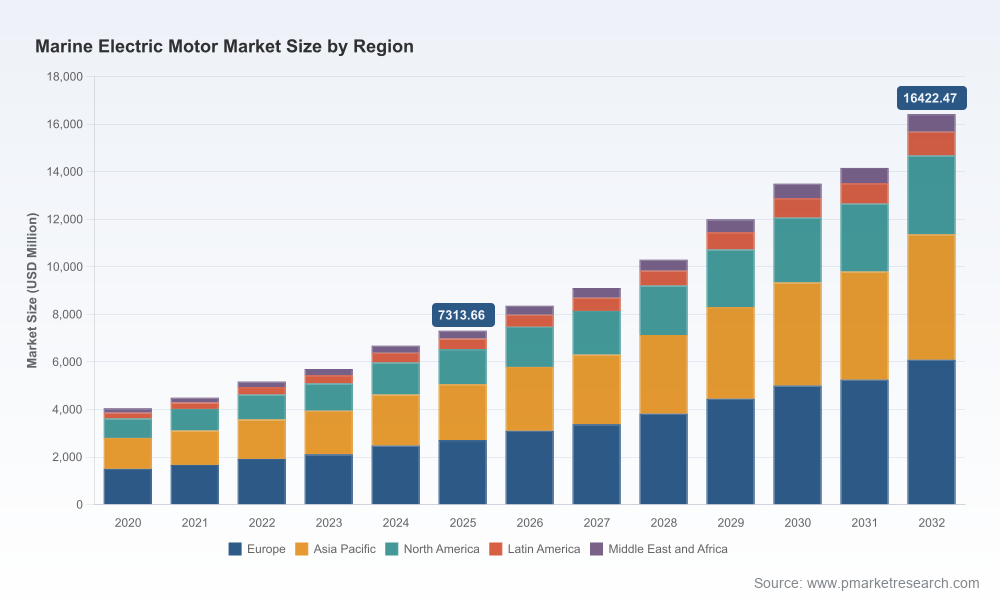

PW Consulting today releases a preview of its forthcoming Marine Electric Motor Market report (base year 2025, historic 2020–2025, forecast 2026–2032). The global market for marine electric motors has entered a sustained growth phase driven by regulatory acceleration, fleet-level decarbonization targets, and rapid technology maturation. Our modelling shows a compound annual growth rate of 12.25% across the forecast window, with the global market more than doubling from the mid‑2020s into the early 2030s (figures presented in the full report are expressed in USD Million). For executive teams planning near‑term capital allocation, product roadmaps, or M&A activity in 2026, the findings provide a pragmatic, decision‑grade synthesis of market trajectory, competitive dynamics, and supply‑chain risk.

Marine Electric Motor Market

Regulatory momentum becomes operational: the IMO’s net‑zero framework and accompanying measures adopted in 2024–2025 transition from policy to compliance readiness, with some mechanisms due to enter into force in the late 2020s. This accelerates demand for low‑carbon propulsion solutions and forces owners/operators to prioritise electrified propulsion or hybrid retrofits during scheduled dry‑dock cycles.

Marine Electric Motor Market

CapEx timing and fleet churn: many commercial fleets are aligning mid‑life investments and newbuild specifications in 2026–2028. These decision windows determine technology lock‑in for a decade or more, making 2026 a pivotal year for OEMs, shipyards, and system integrators to secure partnerships and reference projects.

Marine Electric Motor Market

Supply‑side constraints: raw material concentration risks and copper market tightness influence cost curves for motors and power electronics. Firms that shore up material access or design for material efficiency will gain margin and delivery advantages.

Our top‑line market model (published in the full report) quantifies a strong compounding growth pattern from the base year into 2032. For executives this implies three practical consequences:

Scale matters: manufacturers that can demonstrate manufacturing scale and predictable lead times will capture a disproportionate share of commercial vessel conversions and newbuild pipelines.

Product breadth is no longer optional: a multi‑tier offering that spans low‑power outboards to high‑power drive systems — coupled with modular power electronics and digital services — is required to address both recreational and commercial segments profitably.

Service and lifecycle revenue will be critical: as systems become electrified, buyers increasingly value integrated asset management, remote diagnostics, and retrofit pathways. These after‑sales capabilities create durable margins and customer stickiness.

Demand drivers: policy instruments (fuel standards, emissions pricing), tightening energy efficiency requirements (updates to SEEMP), and commercial logic (fuel cost avoidance and lower maintenance) are accelerating electrification across vessel classes.

Technology enablers: advances in permanent‑magnet motor topologies, improved insulation and thermal management for high‑power continuous duty, and integration with shore‑charging and onboard energy storage systems are expanding feasible application envelopes.

Headwinds: material supply concentration — in particular rare earth magnets and copper — creates episodic pricing and delivery volatility. Additionally, standards fragmentation across flag states and class societies introduces integration and certification complexity for system suppliers.

One of the decisive differentiators in 2026 will be supply‑chain architecture. Firms can pursue three pragmatic approaches, each with distinct risk/reward profiles:

Strategic sourcing partnerships and hedges: for companies with limited capital to vertically integrate, securing multi‑year offtake agreements and diversifying magnet and copper suppliers reduces exposure to concentration‑driven shocks.

Design for material efficiency: re‑engineering motor topologies and system architectures to reduce reliance on high‑risk inputs can preserve performance while lowering procurement volatility.

Selective vertical integration: larger OEMs may capture margin and timeline certainty by bringing magnet procurement, power electronics fabrication, or motor assembly in‑house — but this requires disciplined build‑vs‑buy assessment given capital intensity.

The market exhibits a mid‑to‑high level of concentration: our competitive analysis shows the top three vendors account for a meaningful minority share, with the top five representing just over half of global market value. This structure creates opportunity for well‑capitalised challengers and niche specialists alike.

Established industrial players: firms with deep electrification portfolios (power electronics, drives, and system integration) are orienting offerings to commercial and offshore applications. Their strengths include certification experience, global service networks, and turnkey propulsion systems.

Specialist disruptors: a cohort of startups and niche vendors focus on high‑efficiency outboards, pod drives, and modular motors for small to medium craft. Their advantages are agility, optimized thermal and acoustic designs, and fast product development cycles showcased at recent trade events.

Cross‑sector entrants: industrial motor manufacturers are adapting automotive and industrial drive technologies to maritime environments — competing on cost, robustness, and the ability to scale production quickly for large‑volume segments.

In the full report we provide vendor scorecards, technology mappings, and go‑to‑market playbooks for the principal incumbents and challengers. These tools are designed to support supplier selection, partnership due diligence, and competitor response planning for 2026 initiatives.

Trade shows and product launches in 2025–2026 are signaling a two‑track product evolution: miniaturisation and weight reduction for leisure and commuter craft; and higher‑power, ruggedized platforms for commercial and offshore use. This bifurcation requires different commercial models and engineering roadmaps.

OEMs are emphasizing hybridized system architectures as a pragmatic bridge for large vessels where full electric propulsion is presently constrained by energy density and range considerations. Expect a proliferation of hybrid retrofit offers into the 2026 orderbook.

Regulatory deliverables adopted by IMO and class bodies in 2024–2025 translate to a non‑negotiable timeline for compliance planning. Operators postponing electrification roadmaps risk costly last‑minute conversions and stranded capital decisions.

Our full market study is structured for immediate use by strategy, product, procurement, and corporate development teams. Key deliverables include:

Top‑down and bottom‑up market sizing (USD Million) with historicals (2020–2025) and a granular forecast (2026–2032) under multiple scenarios.

Segment‑level models and sensitivity analyses for motor type, power bands, and application classes — model access is provided in Excel to stress test assumptions for your business case.

Competitive scorecards, capability matrices, and supplier risk assessments that integrate technology maturity, certification track record, manufacturing capacity, and aftermarket footprints.

Supply‑chain risk maps highlighting critical materials (including rare earth dependencies and copper exposure) and pragmatic mitigation strategies tailored to different firm sizes and risk appetites.

Investment and M&A playbooks with valuation heuristics, integration checklists, and case studies of successful and challenged transactions in adjacent electrification markets.

Actionable 18‑month roadmaps for OEMs, integrators, and operators that translate macro trends into prioritized initiatives for product development, pilot deployment, and commercial partnerships.

Prioritise payer economics: align product specifications to the total cost of ownership drivers most salient to target buyers — whether fuel avoidance, maintenance savings, or regulatory compliance.

Lock down material paths now: secure diversified suppliers, consider long‑term contracts for magnet and copper supplies, and invest in design changes that reduce exposure to high‑volatility inputs.

Invest in service and software: monetize diagnostics, predictive maintenance, and energy optimisation — these revenue streams will underpin sustainable margins as hardware margins compress.

Match proof‑points to markets: use demonstrator projects in predictable operating environments (harbour crafts, ferries, and short‑range coastal workboats) to build references before scaling into deep‑sea and heavy‑duty markets.

Adopt an adaptive portfolio strategy: maintain a pipeline of hybrid and fully electric systems and specify modular architectures that allow upgrades as energy storage and charging ecosystems evolve.

This preview articulates the strategic contours that will shape procurement, development, and capital allocation decisions in 2026. PW Consulting’s full Marine Electric Motor Market report provides the data, models, and playbooks that translate these contours into executable plans. We deliberately refrain here from publishing our detailed segment tables and company scorecards in order to protect the actionable intelligence reserved for report subscribers and clients.

To evaluate how these insights apply to your organisation — whether you are an OEM, shipowner, system integrator, investor, or supplier — contact PW Consulting to access the full report, the downloadable financial models, and bespoke advisory engagements to support 2026 decision cycles.

For detailed analysis of this topic, please visit the official page:Marine Electric Motor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com