Corrugating Grease Market — Strategic 2026 Outlook and Executive Briefing

PW Consulting’s new Corrugating Grease Market report delivers a focused, decision-grade view for industrial managers, procurement leaders, R&D heads, and corporate strategists preparing for 2026. Our analysis shows the global corrugating grease market reached USD 215.45 Million in 2025 and, under a baseline scenario, is projected to expand at a 4.62% CAGR across the 2026–2032 forecast window, reaching roughly USD 295.56 Million by 2032. Behind these headline numbers lie operational risks, raw-material constraints, regulatory inflection points, and competitive moves that will determine winners and laggards in the next 12–18 months.

Corrugating Grease Market

Why this report matters for 2026 decision cycles

- Translate market momentum into procurement strategy: quantify when and where long-term supply commitments and hedging are warranted versus spot-market flexibility.

- Align R&D and formulation priorities with tightening regulatory expectations and evolving lubricant thickener supply dynamics.

- Prioritize CAPEX and maintenance planning with validated forecast scenarios for corrugator uptime, bearing life, and lubrication consumption trends.

- Identify strategic M&A and partnership targets within a market showing moderate concentration and clear technology leaders.

What’s inside — pragmatic, applied intelligence

The report is structured for immediate operational use, with modular deliverables that teams can deploy without rework:

Corrugating Grease Market

- Market sizing and forecast methodology — transparent assumptions, sensitivity tests, and three demand scenarios (base, upside, downside) to support budgeting and contingency planning.

- Consumption and demand drivers — granular coverage of corrugated packaging recovery, production throughput, maintenance cadence, and bearings service-life drivers.

- Raw-material and input-cost modeling — forward-looking price curves for core base fluids and thickeners, plus supply-risk heatmaps for critical inputs.

- Regulatory and certification playbook — implications of NSF H1 expectations, EU regulatory trajectories, and practical compliance pathways for manufacturers and converters.

- Competitive landscape and supplier dossiers — profiles, capability matrices, and strategic positioning assessments for the market’s leading suppliers.

- Practical toolkits — procurement scorecards, supplier negotiation scripts, an R&D formulation check-list, and a maintenance optimization calculator to quantify TCO impacts of grease selection.

- Appendices — primary interview excerpts with industry buyers and OEM maintenance engineers, raw data tables, and model templates for internal use.

Data-driven insights and implications

Three themes dominate the near-term environment and should shape 2026 actions.

Corrugating Grease Market

- Demand resilience tied to corrugated packaging recovery. The broader corrugated packaging market has rebounded—supporting steady baseline demand for maintenance lubricants. That macro tailwind underpins our base-case growth but masks important variance by plant type, throughput and geography; the report’s scenario layers quantify these variances so teams can stress-test volume assumptions.

- Raw-material pressure and formulation shifts. Grease thickener markets are in flux. Industry data show lithium-based thickeners remain material to global grease production, while alternatives are gaining attention amid competing demand (notably from EV battery sectors) and supply-side pressures. Tightening environmental scrutiny—particularly around extraction impacts and potential EU REACH dynamics—is accelerating reformulation conversations for high-temperature and food-contact applications. For procurement and R&D teams, this means preparing parallel formulation roadmaps and alternative-sourcing strategies now, not later.

- Certification and incidental-food-contact compliance as a market differentiator. NSF H1 registration is increasingly table stakes for greases used on lines that contact food-package substrates. Suppliers with established H1-compliant grades and documented conversion programs have a measurable commercial advantage when lines require certification-backed lubricants or when converters pursue supplier consolidation.

Competitive landscape — who matters and why

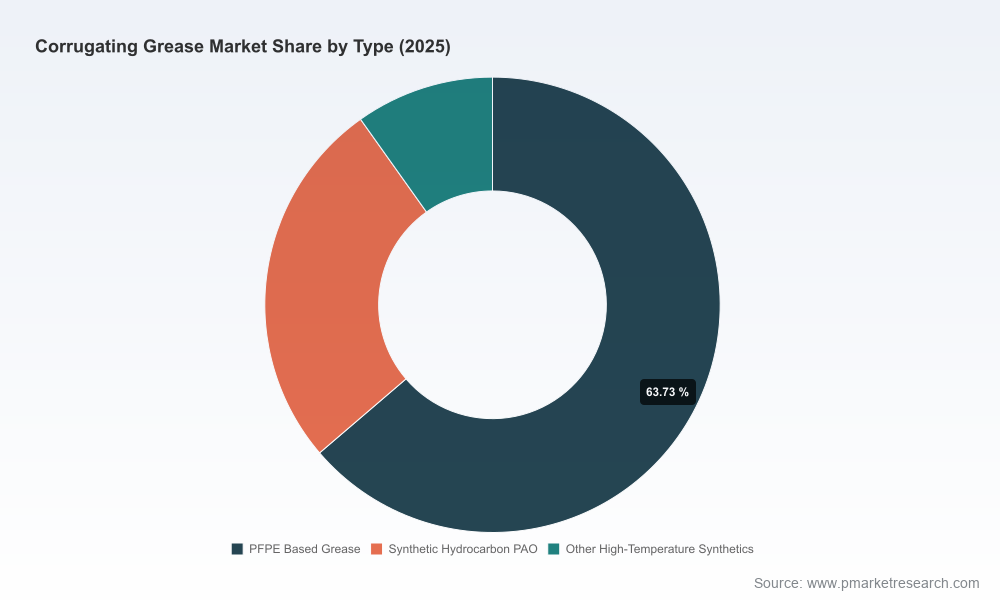

The corrugating grease segment displays moderate concentration: the leading three and five suppliers command meaningful share of the market, creating both stability and barriers to entry. That concentration profile implies differentiated supplier power—particularly in PFPE technologies and food-grade product portfolios.

- Chemours (Krytox) — A benchmark technology provider with PFPE/PTFE-based corrugator greases engineered for extreme thermal stability and film strength. Their corrugator-specific grades are widely regarded as industry references for long-life heated-roll bearing applications and reduced maintenance cycles. Strategic buyers should view Krytox as a technology and service partner when evaluating high-temperature, low-loss lubrication strategies.

- FUCHS Lubricants (including Nye Lubricants) — Combines global manufacturing scale with specialized, NSF H1-capable formulations. Their approach emphasizes conversion services and total plant lubrication programs that demonstrate measurable maintenance-cost reduction. For converters seeking a structured plant-conversion trajectory and documented ROI, FUCHS/Nye-style service offerings are highly relevant.

- LUBCON — European-focused specialist solutions that address the corrugating industry’s high-temperature needs. Their product set and technical support capabilities make them attractive for OEM partnerships and regionally focused consolidation plays.

- IKV Tribologie — Niche provider with NSF H1-registered grades targeted at incidental food-contact environments. Their product focus is well-aligned with converters prioritizing certified, lower-risk formulations across mixed-production lines.

Adjacent supplier activity also matters. For example, developments in water-based inks with improved grease resistance showcased by packaging materials suppliers signal opportunities for integrated value propositions—where lubricant selection, coating chemistry and substrate engineering combine to reduce contamination and maintenance events.

Strategic recommendations for 2026 planning

PW Consulting translates our findings into actionable priorities for management teams:

- Procurement: diversify vs. consolidate strategically. Negotiate layered supply agreements that protect against PFPE supply-chain shocks while retaining premium-grade access for critical lines. Use supplier scorecards that weight certification, service-conversion capability, and proven thermal performance—not only price per litre.

- R&D and product strategy: dual-track formulation roadmaps. Invest in reformulation pilots that reduce reliance on single thickener families and that can meet NSF H1 or equivalent certifications. Build laboratory-to-plant conversion templates to accelerate commercialization if regulatory or supply pressures force switches.

- Operations: convert maintenance programs into value levers. Quantify the TCO of grease selection across bearing types and temperature profiles. Implement bearing-sensor pilots and targeted lubrication audits to capture maintenance savings and validate supplier claims in-situ.

- Commercial: sell maintenance outcomes, not just SKU price. For aftermarket and service teams, craft value propositions that monetize extended maintenance intervals, reduced downtime, and lower scrap. This helps protect margin even when raw-material inflation persists.

- M&A and partnerships: focus on technology and channel access. Targets that either add PFPE expertise, H1-certified portfolios, or converter-service capabilities are highest priority in 2026. Smaller independents with regional OEM ties can be attractive to global players seeking market access without heavy CAPEX.

How to deploy the full intelligence set

This briefing demonstrates the strategic contours you need for 2026 planning. The full PW Consulting report contains the operational detail that converts insight into executable plans: interactive models that let you test procurement scenarios and demand shocks, supplier scorecards with quantified positioning, plant-level consumption estimates, and downloadable procurement and R&D playbooks.

We intentionally present this as a “trailer”: the high-confidence, model-backed conclusions are shown here to guide immediate strategy, while the full dataset and segmentation matrices—covering regional and application-level volumes, supplier share tables, and unit-cost curves—are available in the report package to support execution.

Next steps

- Contact PW Consulting for an executive briefing and customized scenario run for your asset base.

- Commission a supplier risk audit or a formulation readiness assessment to de-risk 2026 supply strategies.

- Schedule a technical workshop to align procurement, maintenance, and R&D teams around a six-month implementation roadmap.

PW Consulting’s corrugating grease market analysis is engineered to reduce ambiguity and accelerate decision cycles. For teams evaluating supplier contracts, planning reformulation, or sizing M&A targets in 2026, this report converts market-level signals into operational action. Reach out to our industry lead to book a tailored walkthrough of the report and the interactive models.

For detailed analysis of this topic, please visit the official page:Corrugating Grease Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com