Biomarker Translation Services Market Size, Share, Technological Trends, and Forecast by 2032

Other |

2026-07-01 07:34:57

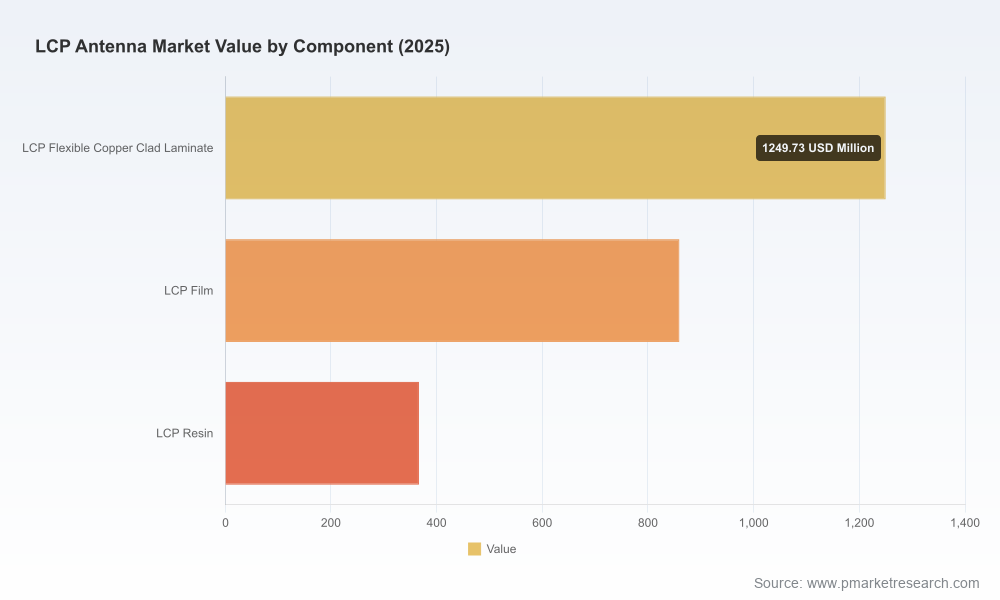

PW Consulting’s latest flagship study on the LCP (Liquid Crystal Polymer) antenna market delivers a concise, practice-oriented brief for executives planning capital, sourcing, and product strategies in 2026 and beyond. The market is at an inflection point driven by the convergence of 5G millimeter-wave deployments, aggressive handset miniaturization, and expanding high-frequency needs across automotive and IoT segments. Our model indicates robust expansion from an industry value of USD 2,475.5 Million in 2025 to an expected USD 7,876.3 Million by 2032, representing a compound annual growth rate (CAGR) of 17.98% over the forecast window. This release highlights why that trajectory matters for boardrooms, procurement, and R&D planners — and what to prioritize this year.

Lcp Antenna Market

LCP has transitioned from a niche polymer to a core enabling material for high-frequency antenna modules. Its electrical stability at mmWave frequencies, low dielectric loss, and form-factor flexibility have made it the material of choice for compact antenna-in-package (AiP) solutions and flexible antenna substrates. As devices demand higher bandwidth and more spatial diversity (e.g., more antenna elements per handset and denser small‑cell infrastructure), the value proposition of LCP-based assemblies increases not only in consumer handsets but also in automotive radar/communications and industrial IoT endpoints.

Lcp Antenna Market

Two structural signals underpin the optimism embedded in our forecast. First, market concentration is meaningful: the top three vendors together control a dominant portion of industry revenues, and the top five account for a substantial share of supply — a topology that favors rapid technology diffusion but also raises competitive pressure on smaller fabricators. Second, the upstream supply base for LCP resin and film exhibits limited but intensifying capacity expansion; a handful of chemical producers remain pivotal to global supply security. Both signals inform near-term procurement and investment choices.

Lcp Antenna Market

PW Consulting’s LCP Antenna Market report is designed to be operational for 2026 planning cycles. It does not merely diagnose trends; it equips decision-makers with pragmatic tools and templates they can apply immediately. Key deliverables include:

The competitive field comprises well‑established electronic components giants and nimble specialized suppliers. Our qualitative analysis distills each major player’s strategic posture and near-term implications for customers and partners.

Collectively, the vendor landscape creates both opportunities and risks for customers: the concentration among top suppliers offers performance consistency and scale, while a vibrant mid‑tier creates competitive pricing and innovation. For procurement leaders, the tactical question is how to balance single‑vendor performance benefits against resilience through multi‑sourcing.

Raw material dynamics are a critical lever: LCP resin and high‑grade LCP film production remain concentrated in a limited set of chemical players. New entrants and localized film-grade production in certain regions are beginning to alleviate constraints, but the industry should expect periodic lead‑time and price volatility tied to specialty monomer availability. Geopolitical measures — including additional tariffs on polymeric electronic components and existing trade policy layers — introduce cost and sourcing considerations that are already influencing near-term supplier decisions.

For executives preparing 2026 budgets and product roadmaps, PW Consulting recommends prioritizing five actions:

This report functions as both a strategic compass and an operational toolkit. It converts macro forecasts into supplier-level implications, risk heatmaps, and commercial templates that can be inserted directly into sourcing RFQs, R&D portfolio reviews, and investor due diligence. Importantly, the document balances transparency with commercial discretion — providing enough empirical rigor to justify capital decisions while shielding granular competitive splits to protect client interests and proprietary vendor positions.

For boards and executive teams initiating 2026 planning cycles: begin with supplier resilience audits, update certification timelines in product development plans, and re-run portfolio economics using the LCP scenarios detailed in our report. For investors and M&A teams: prioritize targets that bring either differentiated high-frequency know-how or tangible capacity that can be quickly integrated into existing manufacturing networks.

PW Consulting’s LCP Antenna Market report is available now. For full access to the segmented revenue tables, supplier heatmaps, and our primary‑research appendices, visit the report landing page or contact our industry desk to schedule a briefing with the authors.

For detailed analysis of this topic, please visit the official page:Lcp Antenna Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com