D-amino Acid Market to Reach US$ 277.4 Mn Amid Rising Demand in Pharmaceuticals and Biotechnology

Other |

2026-06-18 10:12:33

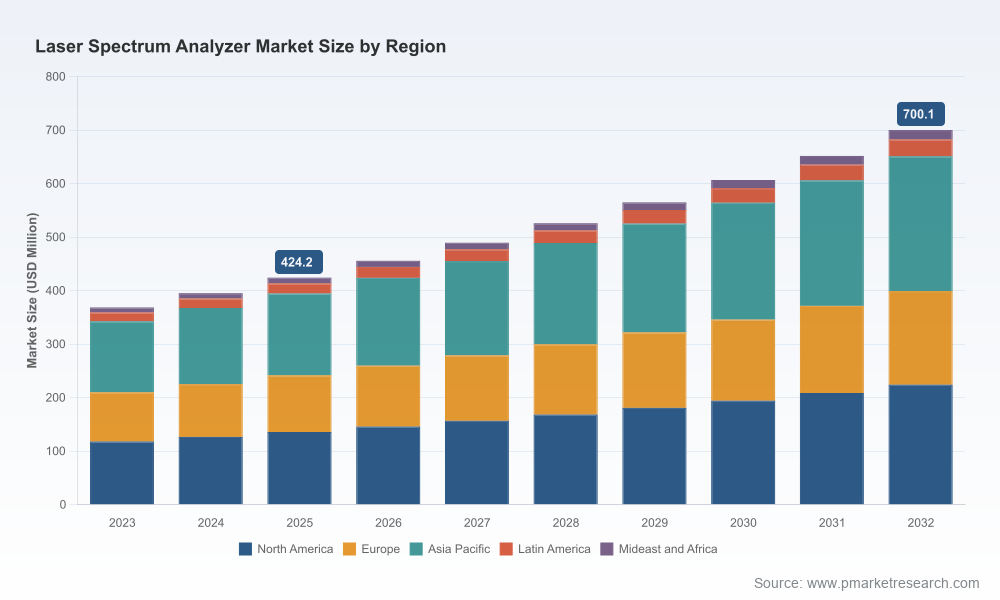

As organizations recalibrate laser and photonics strategies for 2026, PW Consulting’s new Laser Spectrum Analyzer Market report delivers the actionable intelligence that decision-makers require. Built on a 2025 base year and a granular historical series (2020–2025), the study projects the market through 2032. At the macro level, the market size is tracked from an estimated USD 424.2 Million in 2025 to USD 700.1 Million by 2032, reflecting a compound annual growth rate (CAGR) of 7.42% during the forecast interval. The competitive structure is moderately concentrated (CR3 ≈ 54.3%, CR5 ≈ 69.9%), a profile that affects procurement dynamics, innovation pathways, and M&A activity.

Laser Spectrum Analyzer Market

Time-sensitive investment choices — Capital equipment cycles for test & measurement are long and procurement windows are tightening. Our forecast and scenario modules translate macro growth into likely equipment refresh and lab-expansion windows for 2026–2028, allowing procurement teams to optimize CAPEX timing and depreciation planning.

Laser Spectrum Analyzer Market

Supplier selection under geopolitical stress — With export controls and supply constraints shaping availability, the report maps supplier capabilities against regulatory and logistics risk. This enables technology purchasers to build resilient dual-sourcing and substitution strategies without sacrificing technical specs.

Laser Spectrum Analyzer Market

R&D prioritization — For product teams in laser OEMs and component vendors, the research isolates the technology inflection points that will create competitive advantage in the next three years, helping allocate R&D funding where it accelerates market access or creates defensible IP.

M&A and partnership playbook — The combination of moderate concentration and ongoing product innovation suggests fertile ground for tuck-ins and capability buys. The report includes candidate profiling and valuation posture guidance calibrated to 2026 market dynamics.

Our analysis synthesizes adoption drivers across telecommunications upgrade cycles, advanced manufacturing metrology demand, and growth in laser R&D for semiconductor, biomedical, and defense applications. Technological differentiation remains the principal determinant of product premium: high-resolution interferometric solutions, grating-based spectrometers with extended wavelength coverage, and modular, PXIe-compatible analyzers are creating distinct customer segments. Meanwhile, instrument convergence — combining wavelength metering, power metrology, and spectral analysis in compact footprints — is accelerating adoption in test labs and manufacturing lines.

For 2026 planning, three technology themes stand out:

Resolution vs. throughput trade-offs — High-resolution interferometric approaches continue to dominate laser characterization tasks, but there is rising demand for faster acquisition speeds in inline manufacturing testing.

Form-factor and integration — Benchtop, PXIe, and embedded test modules enable new OEM and system-level testing applications; firms that can translate lab-grade performance into manufacturable modules will capture adjacent demand.

Software and analytics — Built-in signal processing, automated calibration flows, and analytics for spectral purity and linewidth are becoming decisive features for buyers focused on throughput and repeatability.

The market is served by a mix of longstanding test & measurement incumbents, specialist photonics instrument makers, and agile startups. Below is a synthesized strategic read on core players and the implications for buyers and partners.

Bristol Instruments (Victor, NY) — Strength: interferometer-based laser spectrum analyzers and wavelength meters combined with FFT analysis for high-resolution measurement. Strategic implication: well positioned for advanced laser R&D and frequency-stabilization applications; attractive partner for OEMs seeking tight wavelength control subsystems.

Thorlabs Inc. (Newton, NJ) — Strength: broad optical product platform with OSAs offering high resolution and dual-detector configurations for fiber-coupled and free-space sources. Strategic implication: leverages channel breadth to serve research labs and small-to-mid scale manufacturing; watch for pricing pressure in the lower-end benchtop segment.

Yokogawa Test & Measurement (Tokyo) — Strength: deep product line spanning visible to long-wavelength ranges and a multi-decade reputation in telecom instrumentation. Strategic implication: incumbent advantage in large enterprise and telco labs; potential lead partner for multi-instrument validation suites.

Anritsu Corporation (Atsugi-shi) — Strength: telecom and sensing-focused analyzers with lab-grade performance. Strategic implication: preferred vendor in network-equipment testing environments and optical sensing validation; synergy opportunities with waveform and network analyzers.

EXFO Inc. (Quebec City) — Strength: intelligent OSAs tailored to manufacturing and lab environments emphasizing OSNR, channel power and central wavelength metrics. Strategic implication: high relevance for manufacturers in DWDM/CWDM ecosystems; a supplier that simplifies integration into production test cells.

Keysight Technologies (Santa Rosa) — Strength: cross-domain measurement platforms and strong systems integration capabilities. Strategic implication: enterprise-scale T&M upgrades often route through Keysight, making them a key strategic partner for large capex programs.

Shimadzu Corporation (Kyoto) — Strength: recently announced SPG-V500 (InGaAs), aimed at expanded optical communications coverage and high-speed spectrum measurement. Strategic implication: new model introductions are a signpost for suppliers focusing on communications-band expansion; OEMs and integrators should assess compatibility with existing test suites.

Quantifi Photonics (NZ) — Strength: compact benchtop and PXIe solutions targeting component testing. Strategic implication: appeals to modular test strategies and organizations moving toward PXIe-based manufacturing test cells.

APEX Technologies, Optoplex, O/E Land, HighFinesse, CNI Laser — Strengths: niche specializations in high-resolution analyzers, photonic subsystems, and extended-wavelength instruments. Strategic implication: these suppliers are valuable for targeted capabilities and often represent the best M&A targets or engineering partners for highly specific measurement needs.

Recent product activity—such as Shimadzu’s upcoming SPG-V500 launch, Bristol Instruments’ multi-laser control systems, and Quantifi Photonics’ showcase at industry events—illustrates continued investment in performance and integration. However, strategic decision-making must be informed by policy and supply-side realities:

Export controls: U.S. export restrictions on certain advanced semiconductor manufacturing equipment (with updates effective through early 2026) impact access to critical photonics components used in analyzers. Buyers should anticipate lead-time risk and compliance costs when sourcing equipment with sensitive subsystems.

Supply chain pressure: Geopolitical tensions are lengthening lead times for key semiconductor and optical components. Our supplier-risk heatmaps identify single-sourced BOM items and propose mitigation options including redesign pathways and alternative vendor lists.

Raw material and gas availability: Disruptions affecting helium and specialty gases used in component manufacturing can translate to episodic capacity constraints. PW Consulting’s operational playbook recommends contract clauses and inventory buffers for buyers in 2026 procurement cycles.

PW Consulting’s Laser Spectrum Analyzer Market report is structured to move executives from insight to action. Key deliverables include:

Market sizing and probabilistic forecasts (2026–2032) with scenario analysis that quantifies implications for CAPEX timing, spare-parts provisioning, and warranty exposure.

Technology deep dives comparing interferometric, grating, and hybrid architectures across resolution, throughput, size, and modularity axes.

Supplier benchmarking and procurement playbook — a decision matrix for sourcing based on product fit, regulatory risk, and total cost of ownership.

Commercial models and pricing sensitivity analyses to support contract negotiation and leasing vs. purchase deliberations.

Operational risk matrix covering export-control exposure, component lead-time stress tests, and contingency routes for critical subsystems.

M&A and partnership heatmap highlighting high-opportunity targets and integration pathways for 2026 acquisition strategies.

Adopt a segmented procurement cadence: Match instrument acquisition to the expected productization or production ramp of laser-enabled systems to maximize utilization and avoid stranded assets.

Prioritize modular, PXIe-compatible or software-defined analyzers where possible — this reduces risk of obsolescence and eases multi-vendor integration.

Establish compliance-first sourcing: Incorporate export-control screening early in supplier selection and define fallback suppliers for regulated components.

Pursue selective partnerships or tuck-ins with specialty analyzer makers to secure narrow but high-value measurement capabilities without heavy internal R&D spending.

Build a three-tier inventory and service model to offset episodic supply constraints while controlling working capital.

Technical leaders will find the instrument-level comparisons and calibration protocols immediately actionable; procurement and supply-chain teams should use the supplier benchmarking and risk matrices to re-run current sourcing scenarios; and corporate strategists should leverage the M&A heatmaps and concentration analysis to identify consolidation and partnership plays. For clients launching new laser products in 2026, the forecasting scenarios provide a playbook to align measurement capabilities with product milestones and regulatory-compliant supply chains.

The narrative above is a curated synthesis designed to surface the strategic implications of the Laser Spectrum Analyzer market trajectory. For access to the full dataset, subsegment tables, market-share breakdowns, and the actionable annexes (including supplier scorecards, full scenario-model workbooks, and ready-to-deploy RFP templates), please consult the PW Consulting report landing page. The report preserves detailed segment economics and company market shares behind the full-access gate to ensure users receive the depth required for confident 2026 decision-making.

For detailed analysis of this topic, please visit the official page:Laser Spectrum Analyzer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com