Hdi Biuret Market 2026: Strategic Imperatives from PW Consulting’s New Market Study

As corporations prepare strategic investments and product roadmaps for 2026, an empirically grounded understanding of the HDI biuret market has moved from nice-to-have to mission‑critical. PW Consulting’s latest Hdi Biuret Market report (base year 2025; forecast 2026–2032) synthesizes five years of historical trends, near-term supply developments, regulatory pressure points, and scenario-based demand outlooks. The headline: the market is on a sustained growth trajectory — expanding from roughly USD 410 million in 2020 to about USD 540 million in 2025 and projected to approach USD 800+ million by 2032 at a compound annual growth rate near 5.85% — but strategic winners will be those who translate this macro momentum into differentiated supply chain, product and regulatory advantage.

Hdi Biuret Market

Why the 2026 Planning Cycle Makes This Report Essential

- Investment timing and scale: The converging dynamics of capacity build-outs, raw-material price spreads, and regulatory tightening create asymmetric risks that can materially affect capital projects and contract negotiations initiated in 2026.

- Product portfolio prioritization: Advances in bio‑content, low‑viscosity chemistries and hydrophilic modifications are changing performance/cost trade-offs. Companies that align R&D and commercialization timelines with market windows captured in our forecast will reduce time-to-value while protecting margins.

- Procurement and sourcing strategy: Reported regional feedstock arbitrage and recent capacity announcements make geographic sourcing optimization and hedging strategies essential to avoid spot-market shocks.

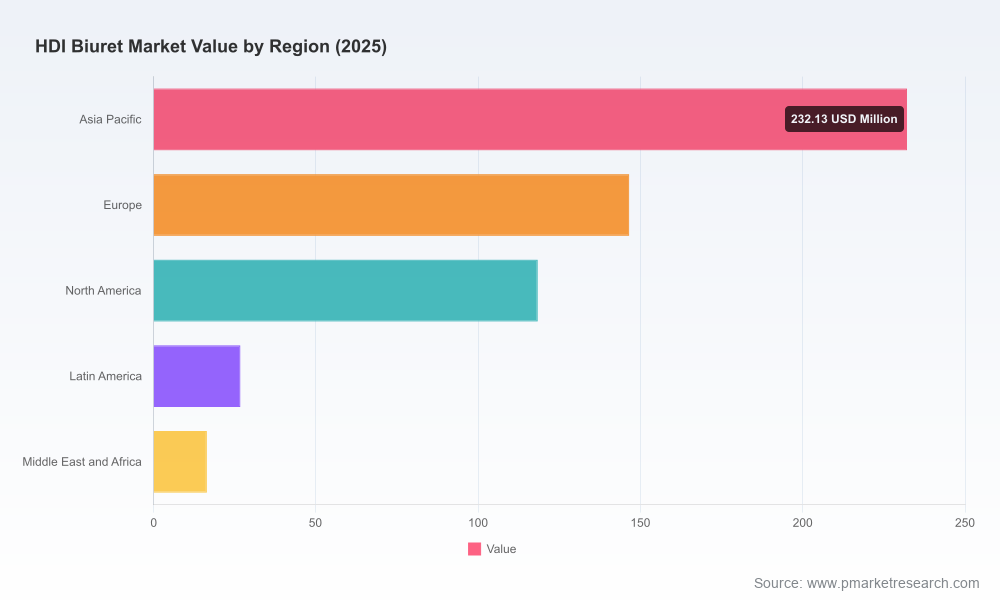

Market Snapshot — Growth Drivers and Structural Dynamics

HDI biuret remains the preferred aliphatic polyisocyanate for high-performance polyurethane coatings owing to weathering resistance, non-yellowing characteristics, and suitability for high‑solids and waterborne 2K systems. Demand growth is being driven by three persistent vectors: transportation and refinish markets pushing for superior aesthetics and durability; industrial maintenance and infrastructure coatings seeking longer asset lifecycles and reduced VOC emissions; and an uptick in high-value specialty applications where performance justifies premium formulations.

Hdi Biuret Market

On the supply side, incumbents and regional players alike are adjusting capacities and product portfolios. Several recent commercial moves — from strategic capacity additions to product launches that embed sustainability features — signal an industry in transition from volume-led expansion toward portfolio differentiation.

Hdi Biuret Market

Raw-material economics also matter: HDI feedstock pricing exhibits geographic spreads that materially affect incremental margins and export flows. For planning purposes, stakeholders should assume a persistent premium in certain Western markets relative to Asia, reflecting feedstock availability, logistics, and historical production footprints. Regulatory frameworks — including EU REACH, VOC limits and increasingly granular residual monomer controls — add a layer of compliance-driven product design imperatives.

What the Report Contains — Practical, Actionable Deliverables

PW Consulting’s study is structured to be a working tool for commercial, technical and corporate development teams. The report blends quantitative forecasting with qualitative playbooks and includes:

- Top‑line market sizing (historical 2020–2025 and forecast 2026–2032) with scenario strips reflecting alternative demand and feedstock-price paths.

- Supply‑side mapping: capacity-by-technology, planned expansions, and a near-term production pipeline assessment (with likely timing and scale of nameplate vs. effective capacity).

- Commercial benchmarking: price‑to‑value matrices, channel economics, and buyer-supplier negotiation levers for coating formulators and OEMs.

- Regulatory risk matrix: country- and region-specific compliance levers, residual monomer thresholds, and practical mitigation strategies for formulations and downstream communications.

- Technology and product deep-dive: performance comparisons across standard and low‑viscosity grades, waterborne adaptation paths, and bio‑content integration options.

- Supply‑chain stress tests and contingency playbooks for procurement, logistics, and tariff exposure, including sensitivity to proposed trade actions affecting aliphatic isocyanates.

- M&A and partnership scouting: private‑company profiles, value-creation archetypes and a shortlist of potential bolt-on targets consistent with different growth strategies.

Each of these modules includes actionable templates (e.g., cost-of-goods scenarios, capex payback calculators, regulatory compliance checklists) that executive teams can adapt directly into 2026 budgeting exercises.

Competitive Landscape — Who’s Moving and What It Means

The HDI biuret market remains moderately concentrated, with the top three players accounting for a significant share of global supply and the top five controlling an even larger share. This concentration creates a market environment where strategic decisions by a handful of majors reverberate across pricing and availability.

- Covestro AG (Leverkusen, Germany): A leader in weather‑stable, non‑yellowing biuret crosslinkers, Covestro has recently commercialized a higher‑bio‑content line targeted at refinish and architectural applications. For downstream buyers, this signals a push to capture sustainability-oriented premiums while maintaining performance parity.

- BASF SE (Ludwigshafen, Germany): BASF’s strategic capacity additions in Europe underscore the company’s intent to shore up supply for transportation and industrial coatings, reducing reliance on spot imports and strengthening contract leverage for long-term customers.

- Wanhua Chemical (Yantai, China): Rapid capacity expansion in China is positioning Wanhua to be a global supply anchor — particularly on cost-competitive product variants — and to shape export flows into adjacent regions.

- Vencorex, Asahi Kasei, Tosoh, Evonik, Kowa, Mitsui, Huntsman and other established suppliers: These firms continue to compete on niche performance attributes (e.g., hydrophilicity, low viscosity, high solids compatibility) and strategic supply contracts. Recent product launches and long‑term supply agreements indicate a market that values reliability and technical support as much as price.

Notable recent developments that should influence 2026 planning include several new product introductions targeting waterborne, high‑solids systems; large-capacity commissioning in Asia; and multi-year supply agreements securing minimum volumes for waterborne applications. Collectively, these moves compress the window for late entrants to secure reliable access to feedstock-grade volumes without paying a premium for spot-market risk.

Strategic Implications and Decision Triggers for 2026

For executives translating the report into concrete decisions in 2026, we recommend focusing on four parallel tracks:

- Secure supply proactively: Shift from transactional sourcing to strategic offtake agreements or joint investments. The report’s supply‑side stress tests identify the point at which spot premiums materially erode product‑level margins.

- De-risk regulatory exposure: Update product specifications and supplier qualifications to meet evolving REACH and VOC-driven constraints. Practical tactics include tightening residual monomer specifications, validating alternative chemistries, and pre‑registering formulation changes with regulators.

- Prioritize differentiated product launches: Allocate R&D and commercialization budget to low‑viscosity and high‑bio‑content variants aligned with OEM and refinish customer roadmaps. Our market adoption timing models help identify the earliest commercially attractive windows that also avoid commoditization risk.

- Explore selective M&A and partnerships: The market concentration means well‑timed bolt‑ons can create immediate access to technology or capacity. Use the report’s valuation templates and synergy case studies to screen targets and structure earnouts tied to technology milestones.

Scenario Planning: Three Plausible 2026 Market Conditions

PW Consulting’s scenario framework helps executives stress-test plans under divergent conditions. Three plausible 2026 states are particularly instructive:

- Policy‑tightening scenario: Accelerated VOC/regulatory alignment pushes formulators toward high‑solids and waterborne systems faster than anticipated, increasing demand for high‑performance biuret grades — advantaging companies with validated low‑VOC formulations and pre‑approved supply chains.

- Feedstock‑shock scenario: Temporary disruptions or tariff shifts widen regional price spreads, favoring vertically integrated players and firms with flexible sourcing contracts.

- Market‑softening scenario: Slower industrial capex reduces demand for higher‑end maintenance coatings, pressuring producers to push into adjacent end‑use segments or pursue price competition — a situation where product differentiation and technical service track records become decisive.

How to Use This Report in 2026 Decision Cycles

- Board and investor briefings: Use the market sizing and scenario outputs to justify capex and M&A decisions with quantified upside/downside ranges.

- Commercial negotiation toolkits: Leverage our price-to-value and COGS models when negotiating long‑term supply or off‑take contracts.

- R&D prioritization: Align formulations and scale‑up timelines to the adoption windows detailed in the report’s diffusion models.

- Regulatory compliance roadmaps: Incorporate the report’s practical checklists and timeline estimates into compliance budgets and labeling plans.

Conclusion — The Strategic Edge Is Execution, Not Forecasting Alone

The 2026 imperative is clear: the HDI biuret market offers predictable growth, but value accrues to organizations that pair market insight with decisive execution across procurement, product, regulatory and corporate development functions. PW Consulting’s Hdi Biuret Market report delivers the quantitative backbone and practical playbooks necessary to convert the underlying market expansion into sustainable competitive advantage.

For teams preparing budgets, negotiating strategic supply, or considering technology investments in 2026, the report provides the granular, operationally oriented analysis that senior decision‑makers need — while preserving the granular commercial datasets that are central to transaction-level planning. To access the full dataset, scenario files, and supplier scorecards that support these recommendations, visit our official report page and download the executive package.

For detailed analysis of this topic, please visit the official page:Hdi Biuret Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com