Glass Fiber Composites Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

PW Consulting’s new Glass Fiber Composites Market study (base year 2025; historical coverage 2020–2025; forecast 2026–2032) synthesizes multi-year primary research, plant-level capacity mapping and proprietary demand modeling to deliver the decision-grade intelligence executives need for 2026. The global market — estimated at USD 66,450 Million in 2025 and modeled to grow at a compound annual growth rate (CAGR) of 5.24% through the 2026–2032 forecast window — is entering a phase where capital allocation, supply resilience and product-positioning choices made this year will determine competitive advantage for the next decade.

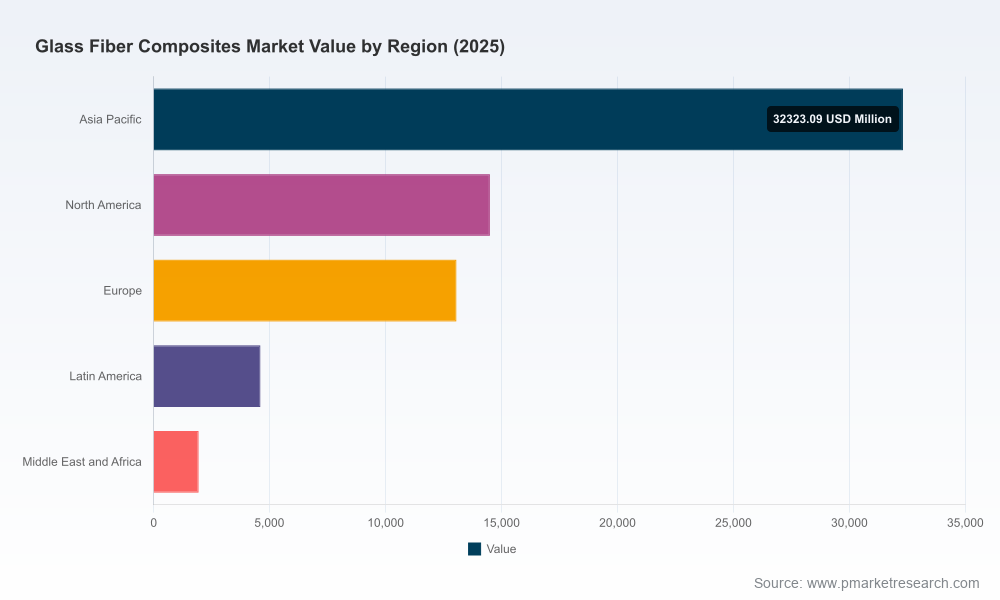

Glass Fiber Composites Market

Executive snapshot: why 2026 is a pivot year

Market momentum entering 2026 is driven by the intersection of decarbonization-led demand (notably in wind and transportation applications), steady growth in infrastructure and construction, and selective high-value opportunities in electronics and aerospace. At the same time, structural dynamics — including a mid-level industry concentration (CR3 ~38.5%; CR5 ~45.2%), emerging specialty glass grades, and localized policy intervention — are reshaping supplier economics and route-to-market strategies. For leaders, 2026 will be the year to translate market visibility into tactical moves: targeted capacity, differentiated downstream solutions, and supply-chain orchestration that secures margin while maintaining flexibility.

Glass Fiber Composites Market

What the report contains — practical, transaction-ready intelligence

- Macro demand forecast and scenario suite (base case plus two alternate scenarios) covering 2026–2032, with sensitivity analyses to input-cost shocks, tariff regimes and renewable-energy deployment scenarios.

- Supply-side mapping at plant level for all major producers, including technology mixes (E-glass, specialty S/SE/DS series, thermoplastic-compatible rovings), lead times, and utilization trends derived from proprietary satellite and customs triangulation.

- Comprehensive competitor dossiers with strategic capabilities, recent capacity movements and implied strategic intent—designed to support M&A target screening and JV diligence.

- Commercial playbooks: pricing levers, indexation strategies, and a supplier-scorecard framework for negotiation and supplier development.

- CapEx prioritization toolkit: NPV/IRR templates tailored for pultrusion, roving lines and specialty glass investments, including break-even windows under alternate raw-material and energy-price paths.

- Application-level prioritization matrix and go-to-market roadmaps that convert macro demand direction into product mix and channel emphasis—optimized for margin, revenue-at-risk and strategic fit.

- Regulatory & trade-impact analysis, including modeled outcomes for common duty and anti-dumping scenarios, and practical mitigations for European and North American market access restrictions.

- Digital transformation & automation maturity assessment with ROI cases for smart manufacturing upgrades and predictive quality control in fiber production.

Competitive landscape: who matters and why

The market remains anchored by large, vertically integrated players and a broad set of specialized manufacturers. Strategic posture across these actors varies from broad-volume plays to differentiated specialty-fiber strategies—each with distinct implications for customers and investors.

Glass Fiber Composites Market

- Owens Corning — A global incumbent with deep exposure to construction and wind markets. Its integrated offering and channel reach make it a primary partner for large OEMs and infrastructure specifiers.

- Jushi Group — One of the highest-capacity producers globally. Its expansion programs signal persistent global demand for commoditized E-glass while also indicating Chinese producers’ increasing capability to serve high-volume wind and transport programs.

- PPG Industries — Positioned to serve higher-value industrial and aerospace-adjacent applications, with a supply strategy that bridges traditional reinforcing fibers and downstream coatings/finish systems.

- Johns Manville — Focused on construction and filtration applications, with recent moves expanding microfiberglass capabilities that cater to high-performance filtration and insulation segments.

- Nippon Electric Glass (NEG) — Plays in electronics and high-performance composites, where tight process control and specialty chemistries command premium pricing.

- CPIC, Taishan Fiberglass, 3B, Saint-Gobain Vetrotex, AGY — These firms collectively represent the spectrum from mass-market reinforcement producers to specialty glass innovators; their activities shape capacity backstops, price floors and technology availability for OEMs.

- Pultruders and component specialists (Exel Composites, Strongwell) — While not glass-fiber producers per se, their downstream roles in prefabricated composite systems create proximate demand drivers and valuable partnership opportunities for material suppliers.

Recent industry developments show capacity additions and product-line upgrades across the value chain. Several major producers have announced expansions and new lines focused on electronic-grade and specialty fibers, while others are investing in filtration-grade and microfiberglass capabilities—moves that reflect an industry balancing volume growth with higher-margin specialty opportunities. PW Consulting’s plant-level mapping translates these announcements into likelihoods for region-specific supply pressure and timing—information included in the full study.

Supply chain, raw materials and policy: the operational cold realities

Two supply-side realities will dominate procurement and margin management in 2026. First, feedstock and energy cost volatility continues to create short-run margin stress; companies with active hedging programs and flexible tolling arrangements will outperform peers in operating leverage. Second, trade policy and regional measures (including existing anti-dumping duties affecting imports into Europe and tariff instruments in North America) remain meaningful constraints on cross-border sourcing strategies. These dynamics force a dual response: shorter, more resilient supply chains for core volumes and selective long-cycle sourcing for specialty grades where concentrated suppliers remain indispensable.

Strategic recommendations for corporate leaders (actionable in 2026)

- Adopt a bifurcated portfolio approach: protect commodity-volume channels through scale and cost optimization, while allocating a portion of R&D and commercial resources to differentiated thermoplastic-compatible and specialty-sglass offerings where value capture is higher.

- Prioritize supply resilience: implement a three-tier supplier strategy (primary, strategic backup, tactical spot) and accelerate qualification of regional second sources to reduce single-point-of-failure exposure.

- Use scenario-driven capex gating: stage greenfield or brownfield investments behind milestone-based triggers tied to signed offtake, indexed feedstock thresholds and policy outcomes to avoid stranded capacity.

- Operationalize pricing sophistication: replace ad-hoc adjustments with index-linked contracts and transparent pass-through mechanisms that preserve OEM relationships while protecting margin through cost cycles.

- Explore downstream integration selectively: partnerships or minority investments with pultruders, blade manufacturers or composite part suppliers can secure demand visibility and accelerate co-development of application-specific fiber formats.

- Embed circularity and alternative feedstocks into product roadmaps to align with procurement mandates from large OEMs and public-sector infrastructure programs; even incremental recycled-content claims can open doors in regulated markets.

- Systematize M&A screening around three criteria: technology adjacency, geographic supply resilience, and customer access. Use our scorecard to prioritize targets that accelerate high-margin specialty growth or remove logistical bottlenecks.

- Invest in digital quality-control: automated inspection and process-control upgrades can materially reduce rework and scrap costs in fiber and pultrusion lines.

How PW Consulting’s study supports 2026 decision-making

Executives tell us the most valuable outputs are not raw tables but decision-ready tools: scenario templates for budget committees, capex gate models for boards, and supplier-engagement playbooks for procurement. Our study delivers all three, plus a web-accessible dashboard where teams can interactively view model outcomes for specified input assumptions. For board-level approval processes, the report provides an executive packet with summarized scenario outcomes, friction points, and recommended motion items prioritized by expected NPV and strategic fit.

Where this preview stops — and why you should download the full intelligence

This preview highlights the structural insights and strategic options that PW Consulting uses to guide executive decisions in 2026. To preserve the competitive value of the report’s proprietary segmentation, plant-level capacity schedules, and transactional playbooks, detailed regional/application breakouts and per-company capacity numbers are reserved for report subscribers. Those granular datasets—coupled with the interactive forecast engine and downloadable capex templates—are the tools that enable teams to execute with confidence.

If your 2026 planning cycle includes capital allocation, supplier strategy, new product development or M&A in glass fiber composites, the full PW Consulting study is built to be the single source of truth for those decisions. Visit the report page to preview the interactive dashboards, download the sample executive packet, or contact our team for a tailored briefing and scenario walk-through.

For detailed analysis of this topic, please visit the official page:Glass Fiber Composites Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com