PW Consulting TDI 80/20 Market Report: Strategic Preview for 2026 Decision-Makers

PW Consulting's latest TDI 80/20 Market report (base year 2025) delivers an executive-grade, actionable intelligence package designed to orient corporate strategy, capital allocation, procurement and regulatory planning through 2026 and beyond. This preview highlights the report's macro trajectory, competitive dynamics and the pragmatic tools buyers, producers and investors need to convert market insight into defensible decisions — while preserving the detailed segment and plant-level datasets for subscribers who access the full report.

TDI 80/20 Market

Macro trajectory you cannot ignore

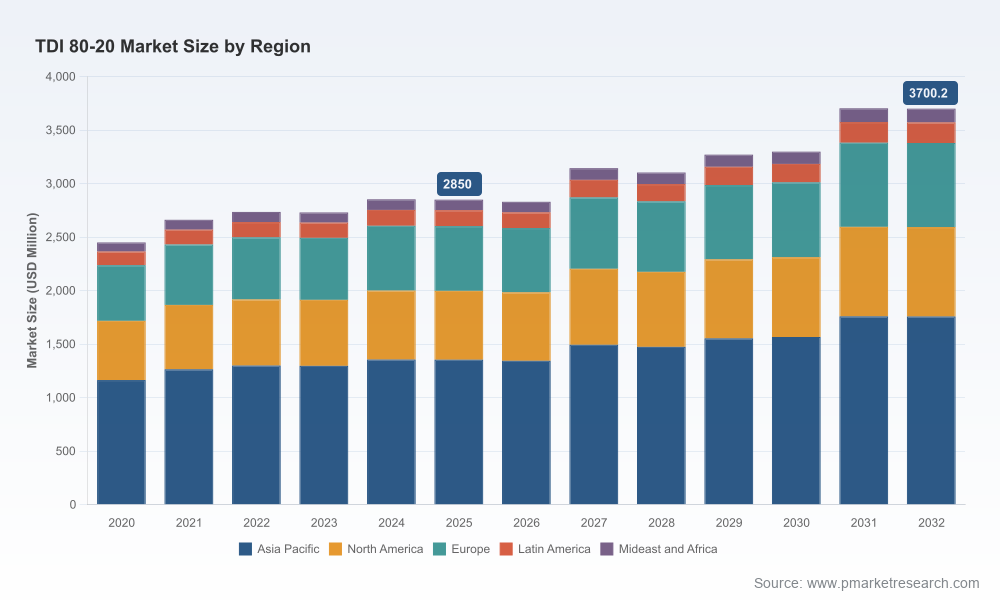

The TDI 80/20 market has demonstrated resilience through uneven cycles. Our historical model shows the global market expanding from USD 2,450 Million in 2020 to USD 2,850 Million in 2025. The 2026–2032 forecast (base year 2025) projects a compound annual growth rate (CAGR) of 3.8%, taking the market toward roughly USD 3,700 Million by 2032 under the base case. Short-term year-to-year dynamics in 2026–2028 reflect inventory adjustments and capacity realignments; medium-term upside is driven by packaging of specialty high-purity grades into premium foam and CASE (coatings, adhesives, sealants, elastomers) segments.

TDI 80/20 Market

Two macro signals are particularly material for near-term decisions:

TDI 80/20 Market

- Consolidation and scale: headline concentration metrics (CR3 ~62.5%; CR5 ~78.2%) indicate the market remains capital- and technology-intensive, with leading producers able to influence availability, pricing and technical supply specifications.

- Input cost and regulatory pressure: a sharp rise in upstream toluene pricing and tightening safety/compliance requirements materially shift cost curves and make feedstock integration and energy efficiency non-negotiable strategic levers.

Why this matters for 2026 corporate choices

If you are setting 12–36 month priorities, this market outlook reframes three classic decisions:

- Capacity vs. flexibility. With renewed project activity and selective large-scale starts, producers must determine whether to pursue greenfield expansions, debottlenecking projects or flexible contract manufacturing to capture cyclical premiums without overcommitting capital.

- Feedstock and energy strategy. A notable input shock — toluene prices in Northeast Asia reached USD 1.08/kg in April 2026 (a step-change increase of ~31.7% in the referenced period) — underlines the value of backward integration, long-term offtake contracts and energy-efficiency retrofits to protect margins.

- Regulatory and trade risk management. With persistent worker-safety thresholds and regional trade protectionism, commercial teams must integrate regulatory scenarios into sourcing and market-entry playbooks to avoid margin erosion or sudden market exclusion.

Competitive landscape — what the leaders are doing

The TDI 80/20 grade remains dominated by a mix of global multinationals and large regional players. Leading strategies observed in the market include scale-driven supply assurance, technology-led efficiency gains and localized regulatory risk mitigation.

- Wanhua Chemical Group — scale and rapid capacity deployment: Wanhua completed a significant Phase II TDI expansion in 2025, adding substantial annualized capacity. The company’s integrated approach in China positions it to service global flexible foam converters while exerting pricing influence on spot markets.

- Covestro AG — technology and decarbonization: Covestro’s modernization at Dormagen illustrates a different playbook: improving energy economics through advanced gas‑phase phosgenation and process-integrated energy recovery. Reported improvements include dramatic reductions in energy intensity and tens of thousands of tonnes of CO2 abated annually — a structural advantage as downstream customers prioritize sustainable supply chains.

- BASF SE — feedstock integration and global reach: BASF’s vertically integrated model provides resilience to feedstock shocks and consistent supply for global customers of flexible polyurethane foam.

- Regional champions (selected examples) — producers across China, India, Korea, Japan and Europe continue to secure domestic demand and selectively pursue export markets. National policy, local cost structures and proximity to converters determine their strategic footprints.

Recent policy events are reshaping trade flows: in early 2026 the Government of India extended anti‑dumping duties on certain imports of TDI 80:20 from Europe and Saudi suppliers, with producer-specific measures in place. This kind of trade protection creates both near-term arbitrage opportunities and longer-term incentives for localized production and backward integration.

Cost, compliance and operational risks

Two non-market drivers deserve explicit operational attention:

- Worker safety and product handling. TDI is a respiratory sensitizer subject to strict occupational exposure limits; regulators and industry bodies publish low threshold values (for example, established 8‑hour TWA levels). Compliance programs that go beyond minimum requirements reduce incident risk and insurance costs, and are increasingly required by downstream buyers.

- Input volatility and energy efficiency. The toluene cost shock of 2026 exposed vulnerabilities in producers operating with thin margins. Capital projects that lower feedstock intensity or capture reaction heat for steam generation materially alter long-run unit costs — an advantage demonstrated by recent plant modernizations.

What PW Consulting’s TDI 80/20 Market report delivers

Our full report is intentionally structured as a decision-ready toolkit rather than a descriptive narrative. Key deliverables:

- Granular market model (historical 2020–2025; forecast 2026–2032) in editable spreadsheets, with scenario toggles to stress-test demand, feedstock cost and capacity supply shocks.

- Supply‑demand balance and price-sensitivity analysis, including short-, medium- and long-term price paths under alternative capacity and feedstock scenarios.

- Plant-level capacity and utilization database with commissioning timelines and technology maps (phosgenation variants, reactor types). Note: detailed plant and segment datasets are accessible in the full report portal.

- Cost-of-production curves by technology and region, with an integrated toluene sensitivity module that models margin impacts across likely price bands.

- Regulatory and trade matrix (REACH, national occupational exposure standards, antidumping measures), with practical compliance checklists and a map of jurisdictional trade barriers and timelines.

- Commercial playbooks tailored to producers, converters and traders: go-to-market scenarios, contract design options, hedging templates and procurement negotiation levers.

- M&A and partnership screen: a prioritized shortlist of bolt-on, consolidation and technology-acquisition targets derived from an accepted valuation framework (EV/EBITDA, replacement cost, strategic fit), plus integration risk scoring.

- ESG and decarbonization roadmap tied to capital planning: retrofits, energy recuperation opportunities and the expected CAPEX payback under multiple carbon-pricing assumptions.

How to translate insight into 90‑day priorities

For executives formulating immediate actions, the report translates analysis into an operational checklist:

- Run a rapid feedstock stress-test on existing contracts and inventory policies; consider layering long-term fixed offtakes or index-linked collars for partial protection.

- Accelerate energy-efficiency projects with the shortest payback and highest CO2 abatement — the Dormagen example shows the magnitude of potential savings when modern technologies and energy integration are applied.

- Revisit commercial terms with key customers and suppliers to account for shifting trade barriers; where anti‑dumping duties apply, quantify landed cost impacts and potential near-sourcing alternatives.

- Prioritize low‑complexity operational safety upgrades and monitoring systems to stay ahead of tightening occupational exposure expectations and customer compliance demands.

Methodology and limitations (preview)

The report uses PW Consulting’s blended methodology combining bottom‑up plant-level capacity data, top‑down demand drivers for polyurethane systems, commodity cost pass-through modeling and qualitative interviews with converters and producers. Base year is 2025; historical coverage spans 2020–2025 and the quantitative forecast covers 2026–2032 at a 3.8% CAGR in the base case. Subscribers receive the full audit trail, including assumptions and sensitivity bounds. To preserve competitive discretion and adhere to client confidentiality commitments, certain granular segmentation tables and plant-level proprietary metrics are reserved for full-report access.

Next steps — where to get the full intelligence

This preview is designed to show the strategic value and practical orientation of PW Consulting’s TDI 80/20 Market report. Organizations preparing capital plans, procurement strategies or M&A pipelines for 2026 should treat the report as an operational playbook rather than a descriptive market snapshot. For the full datasets, interactive dashboards, plant-by-plant capacity maps and downloadable models that underpin our conclusions, please visit the PW Consulting report portal (subscription required). The full package includes the unlock codes for scenario add-ins and a one-hour advisory session with our lead industry analyst to review implications for your business.

PW Consulting’s TDI 80/20 Market report equips executives to move from reactive to anticipatory posture in a market where scale, technology and regulatory positioning increasingly determine winners. The next 12 months will reward organizations that pair disciplined cost management with targeted investments in efficiency, compliance and selective capacity options.

For detailed analysis of this topic, please visit the official page:TDI 80/20 Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com