Global Virtual Restaurant & Ghost Kitchens Market Growing at 5.2% CAGR Through 2034

Other |

2026-06-20 09:22:39

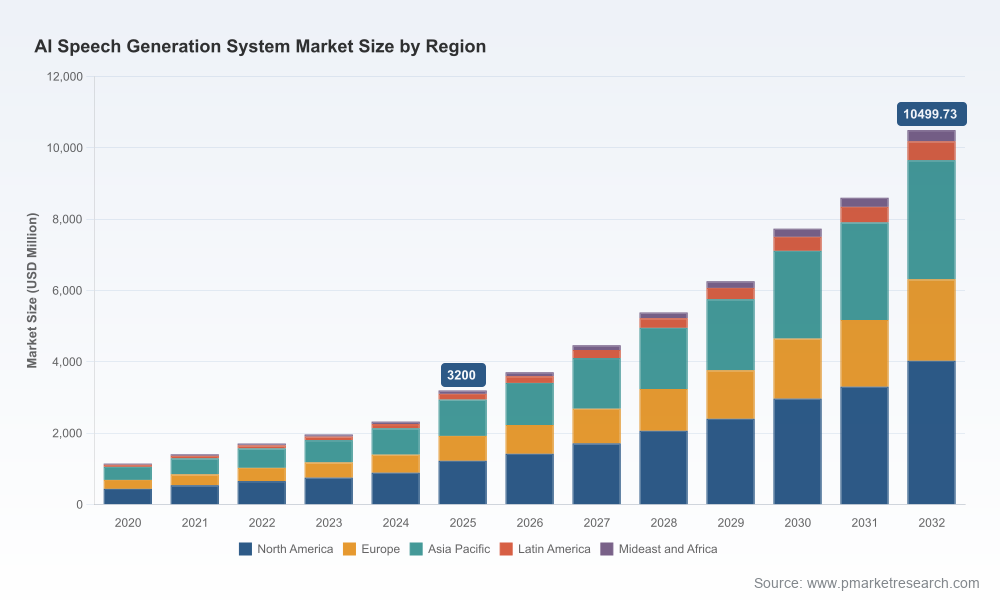

As enterprises move from experiment to production, 2026 marks a decisive inflection point for organizations evaluating AI speech generation. PW Consulting’s latest market study (base year 2025, forecast 2026–2032) quantifies a rapidly maturing market that expands from roughly USD 3.2 billion in 2025 at a compound annual growth rate of 18.5%, reaching the low double-digit billions by the end of the forecast window. That trajectory reflects accelerating adoption across customer experience, learning and development, accessibility, media production, and embedded voice agents — even as regulatory and operational constraints reshape vendor selection and deployment approaches.

Ai Speech Generation System Market

Regulatory pressure and compliance needs have become operational drivers. With the EU AI Act provisions coming into force in the latter half of 2026 and heightened scrutiny around transparency and risk assessments for voice-generating systems, buyers must bake compliance into procurement and architecture decisions rather than treat it as an afterthought.

Ai Speech Generation System Market

Cost economics now favor scale and automation. PW Consulting’s analysis underscores that enterprises can achieve substantial reductions in traditional audio production costs — industry sources cite up to 70% savings in voiceover budgets when workflows are rearchitected around high-quality TTS pipelines — yet those savings are sensitive to per-minute TTS pricing, secondary processing costs, and end-to-end operational overhead.

Ai Speech Generation System Market

Technology performance and product differentiation have moved beyond raw naturalness. Innovations such as fine-grained expressive control, watermarking and SynthID approaches, open-weight frontier models, and native multilingual support are now decisive features that shape vendor fit for purpose across use cases from call centers to media localization.

Executive brief and decision playbook: concise guidance targeted at CIOs, heads of CX, and procurement leaders that translates market dynamics into year-one and three-year priorities.

Robust market sizing and scenario forecasts: baseline and sensitivity models (base year 2025, horizon 2026–2032) that reflect demand elasticity to regulation, pricing, and enterprise adoption curves.

Vendor architecture and capability atlas: qualitative and comparative profiles for major cloud providers and specialist vendors, highlighting technology differentiators, security postures, and go-to-market fit for key enterprise archetypes.

Operational playbooks and TCO modeling templates: downloadable calculators and step-by-step methodologies to estimate end-to-end costs (including TTS per-minute tiers, post-processing, integration, and human-in-the-loop expenses) for proof-of-concept, scaled production, and hybrid deployments.

Compliance and risk checklist: practical controls and contractual clauses to satisfy SOC 2, GDPR, data residency, and AI Act-aligned obligations, plus recommended audit trails and watermarking strategies for provenance and misuse mitigation.

Procurement scorecards and RFP artifacts: vendor selection templates and scoring frameworks calibrated for voice quality, latency, integration effort, security, cost, and vendor roadmaps—designed to be used out of the box or adapted to enterprise weighting.

Deployment playbooks and migration journeys: validated patterns for cloud-first, on-prem, and hybrid topologies, plus a phased operationalization plan for MLOps, voice asset libraries, and consent/IP management.

The market exhibits a two-tier dynamic: hyperscalers provide scale, enterprise integration and broad language/regulatory support; nimble specialists push voice quality, cloning capabilities, and creative tooling. PW Consulting groups providers into pragmatic archetypes to help buyers map capability to use case.

Hyperscaler platforms (e.g., Google, Amazon Web Services, Microsoft, OpenAI): offer broad multilingual coverage, integrated ML platforms, operational SLAs and enterprise-grade compliance features. These vendors are compelling for organizations prioritizing scale, unified cloud ecosystems, and managed services that simplify governance across large estates.

High-fidelity specialists (e.g., ElevenLabs, WellSaid Labs, Resemble AI): differentiate on voice realism, cloning fidelity, expressive control and specialized workflows for media, e-learning and marketing. Their product roadmaps focus on studio-quality outputs, licensing models suitable for creative production, and nuanced controls for prosody and timbre.

Creator- and SMB-focused platforms (e.g., Murf.ai, PlayAI/Play.ht): prioritize usability, rapid content production, and cost-effective options for marketing, explainer videos and social content. These vendors often provide integrated editor experiences and productized templates aimed at non-technical teams.

Recent market moves reinforce these archetypes and the pace of innovation. In early 2026 a frontier open-weight TTS from a European model developer broadened options for high-quality multilingual models; a strategic partnership integrated a specialist’s TTS into a major enterprise orchestration platform to enable agentic voice experiences; and a hyperscaler released advances in expressive control and watermarking—each development underscores how product depth, integration, and provenance technologies are becoming procurement differentiators.

Adopt a vendor-agnostic integration layer: design real-time and batch TTS with abstraction layers that permit swapping backends as voice models and pricing evolve. Doing so preserves negotiating leverage and mitigates lock-in risk from proprietary formats or closed-weight models.

Prioritize compliance-by-design: require transparent documentation of training data practices, watermarking or provenance features, and contractual commitments for auditability and remediation aligned to AI Act expectations and existing data protection regimes.

Run comparative pilots that reflect production complexity: pilot projects should include typical pipeline stages (SSML/voice tagging, post-processing, localization, content scheduling) and be evaluated on end-to-end latency, scalability, cost-per-minute totalized across all pipeline steps, and subjective human assessments of naturalness and brand fit.

Balance cost and voice IP risk: negotiate licensing terms that explicitly address synthesized voice ownership, consent for cloned voices, and permitted uses in downstream monetization so that creative freedom does not translate into legal exposure.

Operationalize detection and provenance: integrate watermarking/SynthID where available, and plan for deepfake detection capabilities in customer-facing deployments to preserve trust and meet emergent regulatory expectations.

Define the primary business outcomes (e.g., first-contact resolution uplift, training throughput, localization velocity) and map required voice quality and latency to each outcome.

Assess regulatory exposure and specify required certifications and data residency constraints in RFPs.

Include total cost of ownership scenarios that account for TTS per-minute tiers, post-processing, storage of voice assets, and compliance auditing.

Require transparent model provenance and roadmap commitments; prefer vendors that publish explainability artifacts and support watermarking/provenance controls.

Plan for hybrid architectures where appropriate—retain on-prem or private cloud options for high-risk content while leveraging cloud scale for lower-sensitivity workloads.

For 2026 decision-makers the question is no longer whether voice AI can add value; it is how to capture that value safely, scalably and cost-effectively. PW Consulting’s report translates market momentum (base year 2025 sizing and an 18.5% CAGR through 2032) into concrete procurement tools, risk frameworks and technical playbooks that reduce the time from pilot to production while preserving compliance and brand safety. Our analysis exposes where margin and risk accrue in the speech stack and prescribes mitigations and negotiation levers tailored to large enterprise environments.

If your organization is preparing an enterprise roadmap, procurement process, or technical architecture for speech AI in 2026, the report provides the templates, scoring frameworks, and scenario-testing tools to convert market intelligence into measurable decisions. For access to the full dataset, vendor scorecards, downloadable TCO calculators and the proprietary scenario workbook, consult the PW Consulting source page and request the actionable appendices designed for immediate deployment.

For detailed analysis of this topic, please visit the official page:Ai Speech Generation System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com