How a Full Blood Test Helps Track Your Health Progress?

Health |

2026-06-23 12:39:25

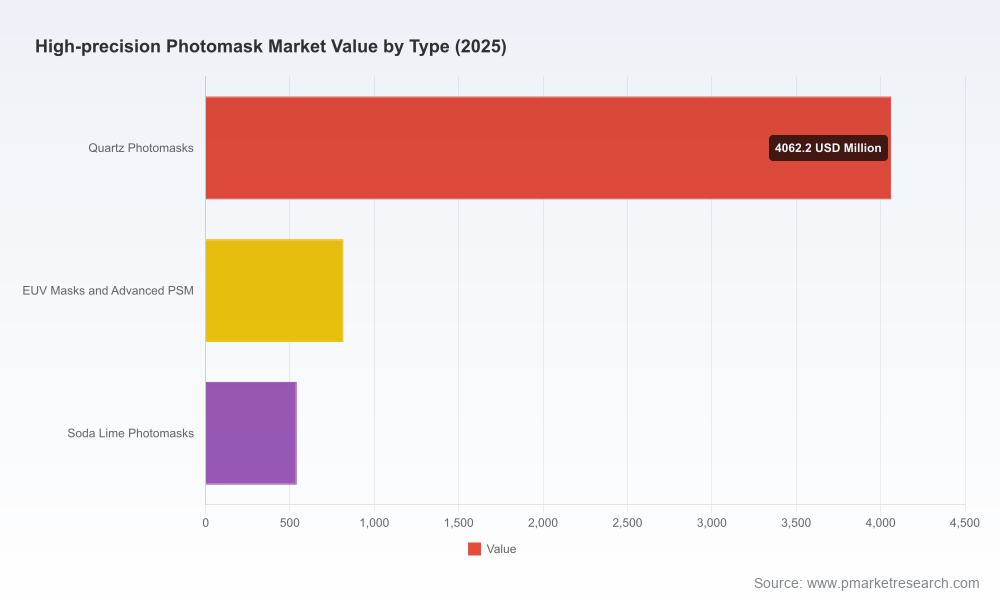

The High Precision Photomask market is entering a period of steady expansion and strategic consolidation that will materially shape capital allocation, supply-chain strategy, and technology roadmaps for semiconductor stakeholders through the remainder of this decade. Our PW Consulting market model shows the industry growing from approximately USD 4.02 billion in 2020 to USD 5.42 billion in 2025, with a forecast that reaches roughly USD 5.87 billion in 2026 and USD 7.87 billion by 2032 — implying a compound annual growth rate (CAGR) of about 5.48% across the 2026–2032 forecast window. While headline growth is attractive, the market’s structural dynamics — concentrated supply, material bottlenecks, and geopolitically driven controls — create both risk and opportunity for buyers, suppliers, and investors planning decisions in 2026.

High Precision Photomask Market

Timing of capacity and capability investments: suppliers’ near-term capacity additions, combined with multi-year technology development cycles for advanced-node masks, mean 2026 is a critical inflection point to lock supply and secure technology roadmaps.

High Precision Photomask Market

Supplier selection under concentration pressure: the market exhibits meaningful concentration — the top three suppliers account for roughly 58% of merchant photomask revenue and the top five about 76% — making counterparty risk, contractual terms, and contingency planning top-tier strategic considerations.

High Precision Photomask Market

Cost and procurement sensitivity to material dynamics: ultra-low-expansion quartz substrates and EUV blank availability, now operating at very high utilization, are driving longer lead times and material premiums that materially affect unit economics of advanced lithography projects.

Regulatory and geopolitical risk shaping access: export controls and allied country policy decisions already influence where advanced photomask equipment and processes can be deployed, forcing firms to rethink sourcing, localized capabilities, and compliance programs.

Robust market sizing and multi-scenario forecasts: adjusted top-down and bottoms-up models that reconcile historical shipment data (2020–2025) with a 2026–2032 forecast under base, upside, and downside scenarios driven by node adoption curves and display demand trajectories.

Supplier capability mapping: an operational view of merchant and captive suppliers across technology tiers (conventional optical masks, advanced PSM/eBeam, and EUV/blank ecosystems) including capacity, lead-time benchmarking, and upgrade paths.

Supply-chain stress-testing: detailed stress tests that measure the impact of blank lead-time shocks, substrate bottlenecks, and export-control scenarios on delivery schedules, cost per mask, and fab ramp timelines.

Procurement playbook: template RFx language, contractual clauses for lead-time protection and price escalation, buffer inventory strategies, and vendor diversification tactics tailored to mask buyers and IDMs.

CapEx and ROI frameworks: stepwise investment calculators to evaluate expansion versus third-party sourcing for mask capacity, with sensitivity to blank pricing and capital lead times.

Technology roadmaps and node readiness: gap analyses showing where merchant providers are positioned relative to sub-7nm/eBeams and EUV mask readiness, and where partners or M&A could accelerate capability access.

Compliance and geopolitical briefings: country-level regulatory impact summaries and mitigation checklists for procurement, IP transfer, and local-content requirements.

M&A and strategic partnership playbook: priority target archetypes, valuation drivers, and integration checklists for companies seeking to secure downstream mask supply or upstream blank control.

Tekscend Photomask Corp. (formerly Toppan Photomasks): a global leading merchant provider with a deep installed base across advanced nodes and broad geographic manufacturing. Recent strategic moves — multiple investments and capacity expansions, including a new plant agreement in South Korea (March 2026), a major multi-phase expansion in Texas supported by public grant funding (January 2026), and targeted equipment upgrades in Europe (2024–2025) — signal a clear push to reinforce global supply resilience and extend coverage into lower-nanometer nodes. Tekscend’s investments have immediate implications for customers seeking predictable, diversified supply chains.

Photronics, Inc.: a global player with a geographically distributed manufacturing footprint and capabilities spanning reduction reticles, binary masks, and advancing EUV development. Photronics’ diversified facility network and service model make it an attractive partner for large-volume fabs seeking flexibility and redundancy.

Dai Nippon Printing (DNP): focused technology development for next-generation EUV masks, including multi-eBeam approaches targeted at 2nm-generation logic. DNP’s R&D posture highlights an industry bifurcation: incumbent merchant specialists upgrading processes versus new entrants and captive programs targeting extreme-node readiness.

HOYA Corporation: a critical node in the blank-to-mask value chain given its position in mask blank supply as well as finished masks for FPD. HOYA’s role underscores how blank producers influence mask economics — particularly for EUV products where multilayer coatings and defect control materially raise pricing.

Regional and specialist players (selected): suppliers across Taiwan, Korea, China, the U.S., and Europe provide breadth and niche capabilities — from high-volume Gen6 display masks to specialized reticles for prototyping. Their strategic relevance depends on customer priorities: cost, lead time, node capability, or geographic proximity.

Capacity and capability expansion by market leaders: deliveries of advanced multi-beam mask writers and installation of new laser writing systems in 2024–2025 materially increase throughput for high-precision masks but require complementary blank supply and skilled operators to realize throughput gains.

Public-private incentives and grants: selective local authority grants and incentives (e.g., U.S. state-level funding for plant expansion) are altering the economics of regional capacity buildouts and should be factored into location and CAPEX decisions.

Accelerated process development for 2nm and advanced EUV masks: ongoing investments in multi-electron-beam and NIL (nanoimprint lithography) capabilities suggest that suppliers are positioning to capture premium advanced-node demand, while buyers must evaluate long lead times for adoption and qualification.

Blank and substrate bottlenecks: benchmark industry data shows leading blank suppliers operating above 95% utilization with high-demand lead times (commonly measured in many weeks). For EUV blanks in particular, specialized multilayer coatings and defect-control requirements command a material pricing premium (industry multiples well into several times the cost of conventional DUV blanks), increasing the pass-through risk to mask buyers and downstream fabs.

Geopolitical and regulatory overlays: export controls from multiple advanced economies have introduced constraints around where certain tools and processes can be exported or applied; these regulations materially affect where advanced-node mask production and equipment can be deployed, and they increase the strategic value of licensed, domestically located capacity.

Concentration risk: with the market heavily weighted toward a small set of large suppliers, buyers face limited options for rapid capacity lift and may need to employ multi-year agreements, pre-booking, or co-investment to secure supply continuity.

Immediate supplier stress-test: run a 12–24 month delivery simulation under conservative blank availability and export-control scenarios; prioritize suppliers with geographic diversification and recent demonstrated capacity investments.

Negotiate layered contracts: blend fixed-volume commitments with flexible call-offs, include force-majeure clarity around regulatory events, and secure price collars to manage EUV blank-driven volatility.

Evaluate co-investment or strategic partnerships: for fabs with critical timing, consider minority investments or long-term capacity commitments with merchant mask suppliers to shorten qualification timelines and prioritize capacity.

Portfolio prioritization: align mask procurement strategy with node prioritization — test volumes and prototyping should be concentrated with partners demonstrating multi-beam or EUV readiness; high-volume mature-node production can leverage lower-cost regional providers.

M&A scouting: target acquisition candidates that provide rapid access to advanced mask-writing technologies or to upstream blank control, especially where regulatory frameworks favor localized capability.

For executives making 2026 investment, sourcing, or M&A decisions, this report is designed as a tactical compass: it synthesizes robust market sizing and scenario forecasts with operational supplier mappings, risk-tested procurement tools, and a practical M&A playbook. The interplay of moderate-to-strong market growth (CAGR ~5.48% through 2032), concentrated supplier dynamics, material supply constraints, and evolving export-control regimes means that winning requires both near-term operational fixes and longer-term strategic positioning. Our analysis provides the actionable layers executives need to translate market forecasts into defensible, time-sensitive decisions.

To access the full dataset, supplier scorecards, scenario model, and executable contract templates referenced in this briefing — including the vendor-by-vendor capability matrices and the detailed stress-test outputs that underpin our recommendations — please visit the PW Consulting High Precision Photomask Market report landing page for subscription access to the complete report and supporting tools.

For detailed analysis of this topic, please visit the official page:High Precision Photomask Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com