Mahadev Book - Play Exciting Cricket Matches, Secure Payments, And Amazing Daily Bonuses

Games |

2026-05-25 18:04:21

PW Consulting’s latest market study on Turbine Discs Broaching Machines (base year 2025, forecast 2026–2032) delivers a practical, decision-ready framework for executives preparing capital plans and supply-chain strategies for 2026. The market has demonstrated a steady recovery and expansion through the first half of the decade and is projected to sustain mid-single-digit compound annual growth. This briefing highlights the strategic takeaways — what matters to procurement, production, engineering and aftermarket leaders — while reserving the granular segment-level tables and vendor scorecards for the full report.

Turbine Discs Broaching Machines Market

Precision broaching for turbine discs remains a critical bottleneck in aero engine and power-generation supply chains. Broaching equipment determines throughput, part accuracy and rework rates for fir‑tree and dovetail geometries that directly affect engine performance and life-cycle costs.

Turbine Discs Broaching Machines Market

As OEMs and tier suppliers accelerate modernization and capacity expansion in response to fleet growth and power-generation projects, equipment selection and process control have become primary levers for capex efficiency.

Turbine Discs Broaching Machines Market

Regulatory and quality regimes, notably NADCAP accreditation expectations in aero engine supply chains, make equipment and process compliance non-negotiable — increasing the strategic value of validated machine-tool vendors and service partners.

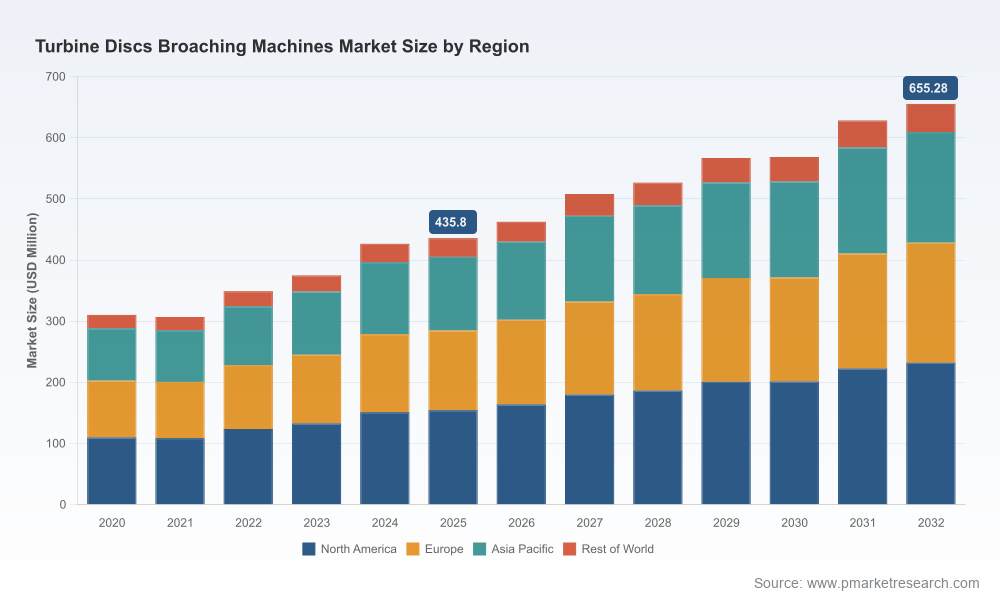

From 2020 to 2025 the total market for turbine discs broaching machines rebounded from pandemic disruption to a stronger baseline as aerospace and gas-turbine activity recovered. PW Consulting projects continued expansion through the 2026–2032 forecast window at approximately a mid-single-digit CAGR. By 2025 the market had re‑established a solid revenue base and by the end of the forecast horizon the market is expected to be materially larger, reflecting both replacement demand and incremental production capacity funded by engine and power programs globally.

The vendor landscape is characterized by a small core of specialist OEMs and several regional or niche suppliers. Market concentration is meaningful: the three largest players control a majority share and the top five capture more than three‑quarters of market revenues. That structure creates two important strategic implications:

Price and lead‑time dynamics can be asymmetric. Tier‑one buyers with volume commitments can secure preferential delivery windows and customization, while smaller buyers risk longer lead times and higher TCO.

Secondary markets for used and remanufactured machines — and specialized service providers — play an outsized role in balancing capacity and cost for smaller producers or those seeking quick scale-up.

PW Consulting’s vendor review highlights several categories of capability that should guide 2026 procurement decisions: machine rigidity and accuracy for high‑alloy work, process monitoring and closed‑loop control, automation and integration with cell‑level robotics, aftermarket and calibration support, and NADCAP/quality credentials for aero supply chains. Representative vendors in the competitive set exemplify these attributes:

Specialist European builders offering compact, high‑rigidity vertical and horizontal solutions with integrated process monitoring and automation options — suited to high-precision fir‑tree and dovetail profiles on large discs.

North American firms supplying large-stroke horizontal machines (new, used and remanufactured) that address heavy‑duty industrial disc broaching and rapid capacity expansion needs.

Japanese and other OEMs producing heavy cutting vertical broaching platforms and purpose-built broaches for heavy‑section superalloys.

Regional Chinese and emerging-market suppliers offering targeted groove-broaching systems with competitive pricing and shorter lead times for non‑critical production streams.

PW Consulting’s full company scorecards benchmark these providers across airborne-critical criteria such as tolerancing capability, automation readiness, service network density, and NADCAP experience; the detailed rankings are included in the full report for procurement review boards.

Turbine discs are increasingly produced from high‑strength, heat‑resistant nickel‑based superalloys. These alloys demand broaching systems capable of high force, thermal stability and precise tool control. Process monitoring — from spindle load tracing to acoustic emission sensing — is transitioning from “nice to have” to “essential” as manufacturers seek to reduce scrap and ensure traceability for certifications.

On the regulatory front, NADCAP accreditation for broaching processes remains a gating factor for suppliers in the aero market; buyers should verify supplier process approvals and traceability capabilities during RFQs. This is especially important for firms planning to re‑qualify or relocate broaching operations as part of capacity strategy.

CapEx sequencing: Balance new-build purchases with strategic acquisition of certified used/remanufactured machines to meet short-term ramp needs without compromising process validation timelines.

Process modernization: Prioritize machines with native digital I/O, inline process monitoring and deterministic control to shorten qualification cycles and enable predictive maintenance.

Supply resilience: Mitigate single-vendor risk through dual-sourcing strategies and service agreements that include spare‑parts pooling and emergency on‑site support.

NADCAP readiness: Incorporate supplier accreditation status and historical audit performance into vendor selection checklists; expect longer lead times for first-time qualified suppliers.

Aftermarket economics: Model total cost of ownership (TCO) including broach tool lifecycle, coolant management, abrasive disposal costs and machine downtime; these often outweigh purchase price over a 5–7 year horizon.

Automation integration: Broaching machines that integrate with robotic disc handling and cell-level automation unlock higher throughput and lower indirect labor exposure. Buyers should specify standard interfaces and safety architectures in tenders.

Digital twins and predictive maintenance: Vendors offering digital simulation of cutting forces and lifecycle predictions for broach tooling reduce risk during qualification and improve uptime forecasting.

Service ecosystems: NADCAP‑aware vendors and service providers with accredited broaching services, tool reprofiling and fine‑tuning capabilities reduce lead‑time risk and support continuous improvement programs.

PW Consulting recommends three pragmatic scenarios for equipment planners and procurement leaders, keyed to capacity needs, risk tolerance and certification timelines:

“Certified Growth” — For OEMs and tier suppliers with long-term contracts: prioritize new, accredited machines with robust automation and a validated vendor roadmap. Expect higher initial capex but faster qualification and lower lifecycle disruptions.

“Rapid Ramp” — For producers needing immediate capacity: combine remanufactured or validated used machines from reputable brokers with fast-track NADCAP process alignment. This reduces time-to-volume while maintaining traceability.

“Cost-Optimized” — For non‑critical or industrial gas-turbine streams: evaluate competitive regional suppliers and service-driven maintenance contracts, but embed strict quality gate requirements to avoid hidden rework costs.

Heightened OEM focus on supplier resilience and nearshoring of critical process steps, which may change lead-time expectations for specialized equipment procurement.

Trade‑show product introductions and recognition events by specialist builders underscore ongoing product innovation and marketing momentum in broaching technologies.

Continuing emphasis on alloy‑specific broaching solutions — a sign that machine‑tool suppliers investing in tooling R&D and process monitoring will gain procurement preference.

The full Turbine Discs Broaching Machines Market report is built for procurement committees, plant managers and strategic planners. It includes:

Validated market sizing and a 2026–2032 forecast model with scenario analysis for demand by end‑use and machine type.

Actionable buyer’s checklists for RFQs covering qualification timelines, NADCAP considerations, digital integration and service-level agreements.

Vendor scorecards and shortlists calibrated against production scale, geographic service footprint and accreditation status.

CapEx planning tools and TCO models to compare new versus remanufactured acquisitions across 5–7 year horizons.

Supply-chain risk maps that highlight lead‑time chokepoints, spare‑parts bottlenecks and mitigations aligned to sourcing strategies.

To protect competitive value for subscribers, this release intentionally omits the granular regional splits, application-level percentages and the proprietary vendor ranking matrix — all of which are available in the full report.

Embed process qualification timelines into procurement cycles now. Lead times for NADCAP‑aligned process validation will materially affect when new capacity enters production.

Approach equipment procurement as a systems decision — judge offers by integration capability, digital readiness and aftermarket support rather than headline price alone.

Use a blended strategy for near-term capacity (select certified used/remanufactured units) while investing in new, automated platforms aligned to long-term programs.

Monitor vendor concentration and maintain contingency plans with service partners to avoid single‑point failures in spare‑parts or calibration services.

PW Consulting’s full report provides the detailed modeling, vendor scorecards and downloadable TCO tools needed to convert the insights above into procurement specifications and board‑level capital plans. For executives preparing equipment investments or supplier negotiations in 2026, this intelligence will shorten decision cycles and reduce qualification risk.

Visit our report page to access sample datasets, executive slides and to arrange a briefing with PW Consulting’s Turbine Discs broaching specialists. The full dataset includes the regional and application breakdowns, as well as the vendor rankings and appendices that are intentionally excluded from this public summary.

For detailed analysis of this topic, please visit the official page:Turbine Discs Broaching Machines Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com