Microbial Fermentation Technology for Food: A Strategic Preview for 2026 Decision‑Makers

As firms plan budgets, M&A, and product roadmaps for 2026, microbial fermentation has moved from “emerging” to “must have” status across food value chains. PW Consulting’s new market study — base year 2025, forecasting through 2032 — provides the practical market intelligence senior executives need to convert scientific opportunity into durable commercial advantage. This press briefing summarizes the report’s strategic value, highlights the competitive dynamics shaping the next wave of investments, and outlines the pragmatic modules that will inform board‑level decisions while intentionally reserving the granular segment tables and company scorecards for the full report.

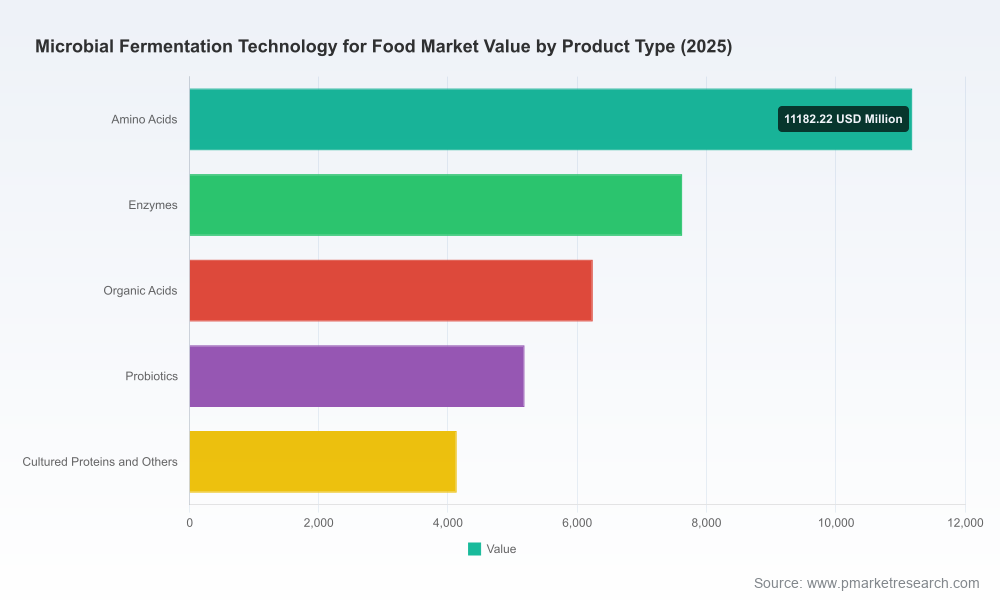

Microbial Fermentation Technology For Food Market

Market Snapshot: Momentum and Scale

After steady expansion through the early 2020s, the global microbial fermentation technology for food market reached approximately USD 34,362.5 Million in 2025 (base year). The market is forecast to grow at a compound annual growth rate (CAGR) of 7.12% over our 2026–2032 horizon, reaching an anticipated market scale in excess of USD 55 billion by 2032. That trajectory underscores both the maturation of precision fermentation and the broadening adoption of traditional fermentation across ingredients, fermented foods, and food‑tech platforms.

Microbial Fermentation Technology For Food Market

Two implications are immediate for corporate leaders: first, the addressable opportunity is now material for mid‑cap and large food companies; second, the growth profile supports multi‑year, staged investments in capacity, IP, and downstream commercialization rather than one‑time pilot grants.

Microbial Fermentation Technology For Food Market

Why 2026 Is Pivotal

- Scaling inflection: Capacity buildouts and facility expansions announced over 2023–2024 are moving from planning to commissioning in 2026, meaning firms that secure supply agreements or strategic partnerships now will be first to market as commercial volumes become available.

- Regulatory convergence: Regulatory frameworks (GRAS/US, Novel Food/EU, health‑claim substantiation guidelines) are crystallizing. Firms that align technical dossiers and labeling strategies before the next wave of product launches will avoid costly reformulations and market delays.

- Value chain choices: The market is bifurcating into ingredient suppliers, equipment and bioprocess providers, and precision fermentation IP houses — each requires a different commercial playbook. 2026 is the decision year to commit to one or more of these roles.

What PW Consulting’s Report Delivers (Practical, Actionable Modules)

The report is structured to be a decision‑support toolkit for 2026 planning cycles. Key deliverables include:

- Macro to micro market model: A transparent global demand model with scenario outputs (central, upside, downside) and clear assumptions so teams can stress‑test capex and revenue plans.

- Technology adoption and ROI matrices: Benchmarks for fermentation approaches (classical cultures, precision fermentation, hybrid fermentation) mapped to time‑to‑market, scale economics, and typical engineering constraints.

- Regulatory playbook: Step‑by‑step filing templates and evidence packages for GRAS/novel food pathways, plus guidance on probiotic health‑claim substantiation to minimize EFSA/FDA rejection risk.

- Supplier & partner scorecards: Comparative evaluation criteria for ingredient suppliers, CMOs, and equipment vendors — including capability, geographic footprint, quality systems, and escalation playbooks.

- M&A and JV decision framework: Valuation heuristics calibrated to fermentation economics, dilution impact scenarios, and integration checklists tailored to food industry acquirers.

- Commercial go‑to‑market playbooks: Channel strategies for ingredient sales, co‑development with CPG customers, and branding considerations for novel fermented products.

- Operational risk register: Raw material, regulatory, and IP risks with mitigations and contingency cost estimates.

To respect the “trailer” principle, the report demonstrates the depth of our models and playbooks while withholding the granular segmentation tables and supplier‑level financials; these are included in the full deliverable for subscribers and advisory clients.

Competitive Landscape: Who Matters and Why

The competitive map is diverse and strategically partitioned into four clusters: established ingredient suppliers, bioprocess equipment providers, precision fermentation IP players, and vertically integrated product innovators.

- Ingredient pioneers: Firms such as Novonesis, dsm‑firmenich, Lallemand, Lesaffre, and Angel Yeast are extending classical microbial portfolios (cultures, enzymes, yeast) into plant‑based and novel fermented applications. Recent transactions and facility expansions demonstrate these players are prioritizing scale and customer proximity.

- Equipment and scale‑up specialists: Sartorius, Eppendorf, and Infors HT are the backbone of commercial fermentation. Their roadmaps — especially in single‑use systems and automated control platforms — materially reduce time‑to‑commercial scale for ingredient manufacturers.

- Precision fermentation innovators: Ginkgo Bioworks, Perfect Day, and The EVERY Company exemplify the new IP‑centric model: gene‑engineered microbes, fermentation at scale, and direct to CPG or ingredient licensing. Their trajectories differ — some aim for ingredient licensing, others for branded consumer products — and both routes reshape value capture.

- Strategic consolidation signals: The market concentration metrics indicate a moderate level of consolidation: the top three companies account for roughly 32.4% of market share and the top five about 48.15%. This concentration creates a dual reality — established incumbents have strong distribution and technical moats, while meaningful share remains available for fast followers and niche specialists.

Three recent corporate developments bear watching: Novonesis’ merger completion (May 2024) broadens culture portfolios; the DSM‑Firmenich integration (completed 2023) embeds fermentation assets within a larger flavor and nutrition platform; and Lallemand’s North American capacity expansion (2023) signals demand conversion in bakery and plant‑based segments. These moves accelerate vertical integration and heighten the importance of pre‑emptive partnership strategies in 2026.

Operational Dynamics and Risk Factors

- Raw material exposure: Fermentation inputs matter. For example, sugar — a common carbon source — experienced price pressure (averaging ~23.5 cents per pound in 2023) during supply tightness. Procurement strategies should include alternate carbon feeds and contractual hedging for multi‑year projects.

- Regulatory complexity: In the U.S., GRAS pathways remain the dominant clearance route for many strains; in the EU, novel fermentation products are typically assessed under Novel Food Regulation (EU) 2015/2283. Additionally, probiotic claims require EFSA‑grade clinical substantiation. Companies must budget regulatory spend early — not as a post‑pilot exercise.

- Geopolitical and capacity concentration: Production capacity is unevenly distributed; for example, one country represents over half of global yeast production capacity for food applications. Supply diversification and regional sourcing strategies are therefore business‑critical.

- IP and talent: Access to strain engineering expertise and bioprocess engineering talent remains constrained. Recruiting or partnering with specialist players (or acquiring them) accelerates capability building but raises integration complexity.

Actionable Strategic Imperatives for 2026

- Commit to a clear role: Decide whether to be an ingredient supplier, an IP owner, a co‑developer, or a branded user of fermentation technology. Each role demands distinct CAPEX profiles and go‑to‑market approaches.

- Lock strategic partnerships now: Secure capacity or off‑take agreements with established suppliers and CMOs ahead of facility commissioning cycles to avoid time‑to‑market slippage.

- Invest in regulatory readiness: Allocate headcount and budget to dossier preparation and pre‑clinical studies to shave months off approval timelines and reduce launch risk.

- Build optionality into feedstock strategy: Negotiate multi‑feedstock fermentation processes and multi‑region sourcing to mitigate commodity price and supply disruptions.

- Use M&A as a capability accelerator: Given the market’s partial consolidation (CR3 ~32.4%, CR5 ~48.15%), targeted acquisitions can buy scale or unique IP at attractive multiples versus greenfield build.

How Senior Executives Should Use This Report in 2026

Boards and executive teams should use the PW Consulting study as the central input into three processes in 2026: capital allocation (what to build vs. what to buy), partner selection (who can deliver scale and regulatory competence), and go‑to‑market sequencing (which applications to prioritize for margin and speed). The report’s scenario models allow sensitivity testing of pricing, capacity utilization, and regulatory timelines — enabling finance committees to create staging gates tied to measurable milestones.

Next Steps

PW Consulting’s full report contains the granular regional and application segmentation, company scorecards, and downloadable financial models that senior teams will require for transaction diligence and internal investment memos. For decision‑ready insights and advisory support in translating these findings into a 2026 investment plan, visit our Microbial Fermentation Technology for Food market page or contact PW Consulting’s advisory desk to arrange a briefing and model walkthrough.

In short: 2026 is the year to move from experimentation to industrialization. The firms that pair scientific rigor with commercial discipline — and who use the right risk mitigations and partner strategies — will capture disproportionate value as fermentation technologies redefine the food ingredient and alternative protein landscape.

For detailed analysis of this topic, please visit the official page:Microbial Fermentation Technology For Food Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com