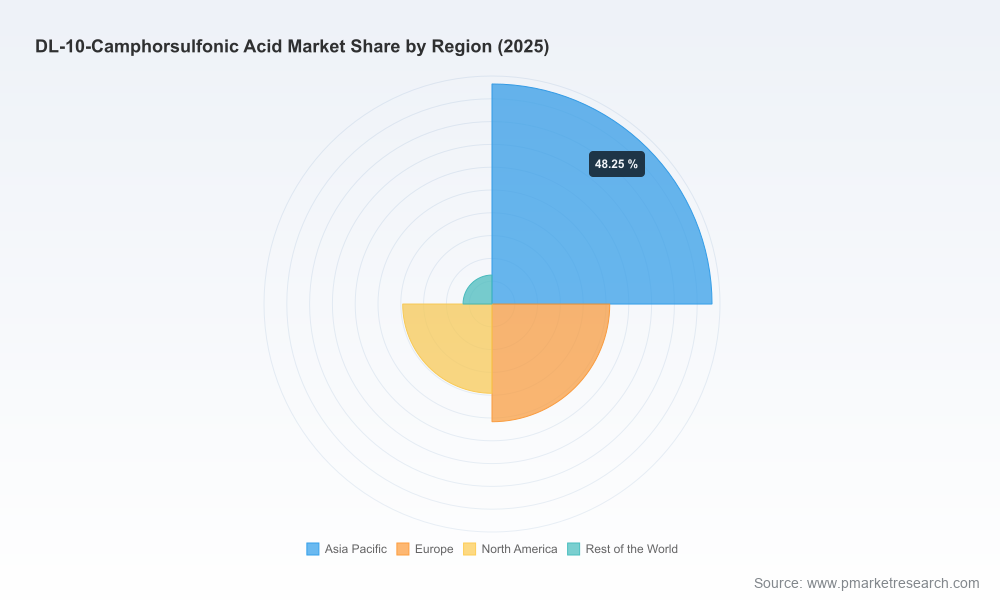

DL-10-Camphorsulfonic Acid Market: Strategic Imperatives for 2026 — PW Consulting Executive Brief

PW Consulting’s new DL-10-Camphorsulfonic Acid (DL-10-CSA) market study synthesizes five years of historical performance with a forward-looking, actionable playbook for corporate decision-makers preparing strategies in 2026 and beyond. Drawing on rigorous primary research, proprietary modeling, and supplier-level intelligence, the report situates DL-10-CSA within the broader specialty chemicals and chiral-chemistry ecosystems and translates market dynamics into concrete strategic options.

DL-10-Camphorsulfonic Acid Market

Market Overview: Resilience and a Clear Growth Trajectory

DL-10-CSA has exhibited steady expansion through the early 2020s, with total market revenues moving from approximately USD 67.25 million in 2020 to USD 85.5 million in the base year 2025. Despite episodic volatility in 2023, the product’s role in pharmaceutical intermediates, chiral resolution workflows and catalytic chemistry has underpinned durable demand growth. Our forecast through 2032 projects the market to reach roughly USD 121.29 million by 2032, driven by a compound annual growth rate (CAGR) of 5.12% over the 2026–2032 forecast window.

DL-10-Camphorsulfonic Acid Market

These headline figures mask important inflections: secular drivers tied to pharmaceutical R&D and manufacturing capacity expansion, coupled with incremental adoption in specialty catalysis and research applications, are creating a multi-path growth profile. PW Consulting’s scenario analysis quantifies upside and downside outcomes attributable to pharma cycle variability, regulatory changes, and supply chain shocks — enabling leaders to stress-test capital and procurement plans against realistic market trajectories.

DL-10-Camphorsulfonic Acid Market

Why This Market Matters for 2026 Decision-Making

- Strategic sourcing and supply continuity: DL-10-CSA is a specialty input with quality-sensitive applications. Firms that establish multi-sourced supply networks and implement tiered inventory strategies will materially reduce production risk for chiral syntheses and resolution processes.

- Product and process differentiation: Variations in purity, particle form, and packaging logistics create windows for suppliers and users to capture margin improvements. Companies that invest in specification tailoring and co-development agreements with end-users can command premium positioning.

- M&A and partnership opportunities: The market’s concentration dynamics create fertile ground for bolt-on acquisitions and strategic partnerships, particularly for mid-sized chemical manufacturers seeking entry into chiral reagent portfolios or for academic spin-outs commercializing novel resolution agents.

- Regulatory and sustainability alignment: Heightened scrutiny around raw material provenance and waste streams is reshaping supplier selection criteria. Early movers that integrate compliance and greener process chemistries into their offering will enjoy lower friction in regulated markets.

What the PW Consulting Report Delivers — Practical, Executable Intelligence

Our DL-10-CSA study is intentionally operational in orientation. Rather than high-level commentary, the report provides tools that procurement, R&D, and corporate strategy teams can act upon in 2026:

- Robust market-sizing methodology: Transparent, auditable top-down and bottom-up estimates covering 2020–2025 historicals and 2026–2032 forecasts, including scenario variants tied to pharma-capacity shifts and research funding cycles.

- Supply-chain and cost-driver maps: Line-item analysis of upstream inputs, synthesis routes, and logistics vectors that affect price and availability, with stress scenarios for feedstock shortages and logistics disruptions.

- Commercial playbooks for suppliers and buyers: Go-to-market strategies tailored to different customer segments (from large pharma to academic labs), recommended contract structures, and pricing frameworks to balance volume growth with margin protection.

- Formulation and purity guidance: Benchmarked specifications, stability considerations, and handling best practices that reduce rejection rates and improve downstream yields for resolution processes.

- Investor-ready competitive landscaping: Concise profiles and strategic positioning analysis of the market’s leading suppliers, plus an M&A heat map identifying likely consolidation targets.

- Regulatory, safety, and sustainability assessment: Jurisdictional overviews of compliance requirements, EHS concerns, and emergent sustainability expectations that affect procurement and product claims.

Importantly, while this executive brief maps the market’s contours and strategic imperatives, the full report contains the granular splits, regional demand matrices, and application-level elasticity estimates that underpin revenue forecasts and opportunity sizing.

Competitive Landscape — Who to Watch and Why

The DL-10-CSA market blends global laboratory suppliers with specialty chemical manufacturers. Our supplier intelligence highlights firms that combine scale, quality control, and channel reach — and those that present strategic advantages to customers.

- Merck KGaA (MilliporeSigma) — A global leader in high-purity specialty reagents, offering dedicated product SKUs tailored for high-end chiral resolutions and synthetic workflows. Their depth of analytical support and global distribution network make them a preferred partner for regulated pharmaceutical manufacturers.

- Tokyo Chemical Industry (TCI) — Strong in reagent-grade supply for research and industrial catalysis, TCI’s regional operating model and emphasis on catalog breadth enable rapid fulfillment and technical support for process development teams.

- Thermo Fisher Scientific (Alfa Aesar & Acros Organics) — With multiple brands under a single corporate umbrella, Thermo Fisher’s strength lies in product availability across scales, from research quantities to larger production packs, and in global logistics capabilities.

- Santa Cruz Biotechnology — While focusing on biochemical and life-science channels, firms like Santa Cruz provide targeted distribution to research communities and niche applications, an important channel for academic-driven innovation that later industrializes.

PW Consulting’s competitive chapter drills into each firm’s value proposition, catalog positioning, support services, and likely strategic moves through 2026. This section is designed to help buyers shortlist partners, support procurement negotiations, and help investors assess consolidation prospects.

Key Market Dynamics Shaping 2026 Strategy

- Pharmaceutical pipeline and manufacturing trends: The increasing complexity of active pharmaceutical ingredients and the emphasis on enantioselective synthesis are structural tailwinds for DL-10-CSA demand.

- Quality and specification premiumization: Demand bifurcation between high-purity grades for clinical and commercial manufacturing and more commoditized grades for research/in-house synthesis is accelerating supplier segmentation.

- Supply concentration risk: A limited number of established suppliers, combined with specialized manufacturing routes, raises the probability of supply tightness during demand spikes — necessitating capacity visibility and dual-sourcing policies.

- Cost and logistics inflation: Raw material price swings and logistics constraint scenarios are modeled in the report, showing their asymmetric impacts on smaller vs. larger buyers.

- Regulatory and sustainability pressure: Increasing buyer preference for suppliers with robust EHS documentation and sustainable sourcing practices is reshaping procurement criteria.

Actionable Recommendations for 2026

PW Consulting translates market intelligence into a prioritized set of actions tailored to common stakeholder objectives:

- For procurement leaders: Institute a three-tier supplier strategy (primary, secondary, and contingency), negotiate volume-flex clauses, and require supplier visibility into capacity and quality control metrics.

- For R&D and process teams: Collaborate early with suppliers to co-develop optimized grades that reduce downstream purification steps; invest in small-scale trials that quantify yield uplift from specification changes.

- For corporate strategy and M&A teams: Use the report’s M&A heat map to target bolt-on acquisitions that add specification capabilities or regional production nodes, accelerating time-to-market for value-added grades.

- For sustainability officers: Integrate supplier EHS audits into sourcing decisions and explore partnerships that reduce solvent and waste burdens in DL-10-CSA synthesis.

Why PW Consulting’s Report Is a ‘Must-Have’ for 2026 Planning

In markets where small specification differences translate to outsized operational and financial implications, executives need more than directional commentary: they need reproducible assumptions, supplier-level visibility, and implementation-ready recommendations. PW Consulting’s DL-10-CSA report bundles those elements with scenario-tested forecasts — including downside and upside cases — so that C-suite teams can align capital allocation, procurement strategies, and R&D priorities to realistic market pathways.

As an example of the report’s practical value, our models allow procurement to compare the total landed cost of different sourcing strategies under a set of realistic disruption scenarios, while our product-specification playbook quantifies the potential yield improvement and cost savings from migrating to a higher-specification input in a representative chiral resolution process.

Next Steps

This executive brief outlines the strategic landscape and high-level recommendations. For practitioners seeking the granular inputs needed to build 2026 budgets, supplier scorecards, or acquisition screens, the full PW Consulting DL-10-Camphorsulfonic Acid Market report provides:

- Detailed regional and application-level demand matrices

- Price and margin modeling templates

- Supplier scorecards and readiness assessments

- Step-by-step procurement and commercialization playbooks

Access to the full intelligence set will enable your team to convert the market’s projected growth (from USD 85.5 million in 2025 toward an estimated USD 121.29 million in 2032 at a 5.12% CAGR) into defensible, high-impact decisions for 2026 and beyond. PW Consulting stands ready to support integration of these insights into your planning cycle, whether through tailored client workshops, procurement audits, or M&A diligence support.

For detailed analysis of this topic, please visit the official page:DL-10-Camphorsulfonic Acid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com