Grant Management Software Market Next Growth Frontier

Other |

2026-06-24 09:10:07

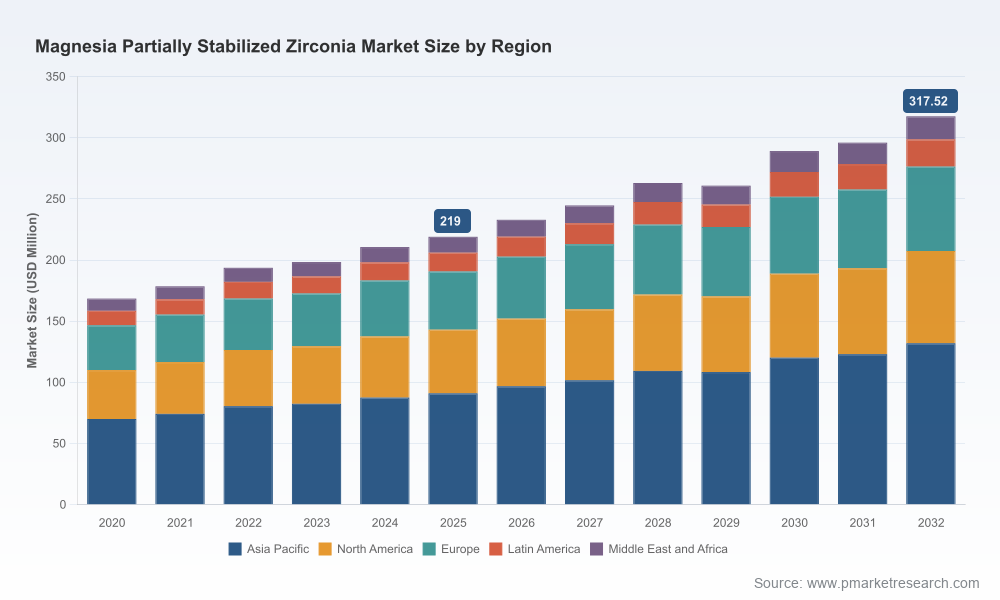

As companies set strategic priorities for 2026, understanding the magnesium partially stabilized zirconia (Mg-PSZ) market is no longer optional — it is a source of competitive advantage. PW Consulting’s latest market study synthesizes seven years of historical behavior (2020–2025) and delivers an actionable forecast through 2032. The market reached an estimated USD 219.0 Million in 2025 and our model points to a steady multi-year expansion at a compound annual growth rate (CAGR) of 5.45% across the 2026–2032 forecast window. This brief highlights the report’s strategic value for executive decision-making while preserving the detailed segment-level matrices available in the full report.

Magnesia Partially Stabilized Zirconia Market

Performance-driven substitution: Mg-PSZ is increasingly chosen over traditional metals and carbides where a combination of toughness, wear and corrosion resistance, and thermal stability delivers total-cost-of-ownership improvements in severe-service environments.

Magnesia Partially Stabilized Zirconia Market

Cross-industry reach: Applications span heavy industrial equipment, precision extrusion tooling, valves and pumps for oil & gas, and high-temperature crucibles and components — making Mg-PSZ a strategic material across multiple supply chains.

Magnesia Partially Stabilized Zirconia Market

Supply-side fragility: Upstream feedstock dynamics and geographical concentration create procurement and continuity risks that will shape sourcing and investment priorities in 2026.

Our base-year calibration to 2025 (USD 219.0 Million) and the 5.45% CAGR used for scenario generation produce a mid-single-digit growth trajectory through 2032. That profile reflects a market that is not explosive but resolute — maturing where performance differentiation, rising service life expectations, and new high-temperature applications sustain demand. The forecast incorporates observed near-term accelerators such as new product introductions and standards re-affirmations, as well as headwinds including feedstock concentration and potential supply deficits beyond 2026.

Lifecycle economics, not first-cost: Buyers increasingly evaluate ceramic components by lifecycle uptime, maintenance cycles, and replacement intervals. Mg-PSZ’s superior toughness in select grades shifts procurement evaluations toward higher-spec components when downtime costs are high.

Application migration: Proven Mg-PSZ grades are penetrating higher-spec applications (e.g., non-ferrous metal extrusion tooling and severe-service pumps), creating cross-application transfer opportunities for suppliers who can demonstrate in-field reliability.

Standards and medical legitimacy: The reapproval of relevant ASTM specifications for high-purity dense Mg-PSZ underpins trust in certain specialty markets (surgical implants among them), opening niches that reward suppliers with certified, traceable processes.

Feedstock pressure: Premium-grade zircon sand — the principal upstream feedstock for zirconia production — held prices just under USD 2,000/metric ton through 2025 and showed stable availability. However, industry sourcing studies point to a projected medium-term deficit beyond 2026 as several mature mines approach depletion. Buyers should allocate risk capital to feedstock strategies now.

Concentration risk: Global zircon exports remain geographically concentrated. The top producing mines control a disproportionate share of supply, making the value chain sensitive to regional disruptions and regulatory shifts.

Manufacturer concentration: Market concentration metrics indicate a market where scale and technical capability matter — our concentration indices speak to meaningful advantages for the leading groups, while also leaving room for specialized players to defend high-margin niches.

The market comprises a mix of global incumbents and specialized regional manufacturers. Competitive differentiation today hinges on three capabilities: materials science (grade and microstructure control), application engineering (proof in-service), and supply resilience (localized production and precision finishing).

CoorsTek — Known for its Dura-Z™ Mg-PSZ line, CoorsTek emphasizes toughness and fatigue performance for severe-service valves and machinery parts. Their value proposition is durability in extreme mechanical environments, an advantage in customers with high uptime costs.

Morgan Advanced Materials (Nilcra®) — Morgan’s Nilcra® grades highlight high Weibull modulus and long-term reliability. Their portfolio targets wear and corrosion replacement opportunities in materials handling and non-ferrous extrusion, positioning them as a go-to for OEMs seeking proven life extension.

Refractron Technologies — Refractron’s Izory®HD and focus on US-made precision-ground parts underscore a supply-resilience play, appealing to buyers prioritizing lead-time certainty and domestic sourcing for strategic equipment.

Superior Technical Ceramics (STC), C-Mac International, Zircoa Inc., Bangalore Ceramics — These firms represent the spectrum of specialty capability: transformation-toughened materials for high-temperature stability, engineered feedstocks and crucibles, and bespoke formed components for regional markets. Each demonstrates how focused technical differentiation can command premium positions.

Recent company-level developments further illustrate market dynamics: a 2026 application note highlighted a new MgO-PSZ crucible composition capable of reliable operation near 1850°C, while product catalog updates and ASTM standard re-approvals during 2025 signal both expanding application envelopes and regulatory continuity. Such signals matter for procurement engineers and R&D leaders planning 2026 specifications and qualification roadmaps.

The combination of steady market growth and concentrated supply should inform corporate strategy across four priority areas.

Procurement resilience: Firms should move from transactional to strategic sourcing for zirconia feedstocks. Actions include dual-sourcing agreements, indexed long-term contracts where feasible, and inventory strategy refinement to cover critical production windows beyond 2026.

Vertical and near-vertical plays: Economic value accrues to manufacturers that can combine specialty powder engineering, sintering know-how, and precision finishing. For industrial OEMs evaluating backward integration or JV partnerships, targeted investments could improve cost certainty and open proprietary materials differentiation.

R&D and product roadmaps: Prioritize grade-application pairing and accelerated field trials. Suppliers that can document demonstrable life-extension or reduced downtime in customers’ production environments will accelerate adoption. Invest in cross-disciplinary validation (materials science + application engineering + lifecycle cost models).

M&A and commercial strategy: Given moderate concentration, roll-up strategies in regional markets or bolt-ons that add finishing, machining, or application validation labs can create defensible platforms for growth. Conversely, established players should consider selective partnerships to shore up local supply in regions with feedstock vulnerabilities.

Our published study is structured to be immediately operational for commercial planning, procurement, and R&D investment committees. It includes:

A transparent market model calibrated to 2020–2025 observations and producing scenario-based forecasts through 2032, with sensitivity testing for feedstock disruption and accelerated adoption scenarios.

Supply-chain maps that identify single-point vulnerabilities, major export hubs, and logistics risk scenarios — authored to inform sourcing and inventory policies.

Commercial playbooks for suppliers and OEMs: go-to-market segmentation logic, margin archetypes by product positioning, and prioritized account strategies for penetration in severe-service applications.

Full vendor benchmarking and capability matrices: technical differentiators, production footprints, finish capability, and case studies demonstrating where Mg-PSZ replaces incumbent solutions.

Regulatory and standards annex: interpretation of relevant ASTM re-approvals and their implications for medical and specialty high-purity markets.

For CEOs and corporate development teams — use the market trajectory and concentration insights to prioritize inorganic activity and identify timing for value-accretive acquisitions.

For procurement and supply-chain leaders — convert the feedstock intelligence into a one-page sourcing risk register and immediate mitigation actions for 2026.

For R&D and product management — align 2026 budgets to validation programs that document total-cost-of-ownership gains where Mg-PSZ has demonstrated life-cycle superiority.

Mg-PSZ occupies an important role in the materials stack: not a mass-market commodity, but a performance material whose adoption is driven by evaluable economic outcomes. Our market sizing confirms disciplined growth, and the concentration dynamics deliver both opportunity and risk. The full PW Consulting report provides the quantitative granularity, vendor-level scorecards, and scenario models needed to convert these insights into 2026 decisions with measurable impact. For executives who must balance capital deployment, supply risk, and product differentiation, the report functions as both a decision-support model and a practical playbook.

To access the full dataset, segmentation tables, and our proprietary vendor scorecards, consult the complete Magnesia Partially Stabilized Zirconia Market report on PW Consulting’s publications page.

For detailed analysis of this topic, please visit the official page:Magnesia Partially Stabilized Zirconia Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com